Past performance does not predict future returns. You may get back less than you originally invested. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

The market is underestimating the run on inference compute, and not all hyperscalers will monetise it equally. The debate is no longer whether AI capex will generate a return; it is which hyperscalers have the compute, the custom silicon and the model access to monetise token demand fastest. Cloud revenue is inflecting higher than the market is modelling, and we expect aggregate hyperscaler capex to keep moving up – every operator is still saying demand exceeds supply, and we think that imbalance gets worse in 2026, not better.

Look at the evidence from the recent Q1 earnings season: Amazon’s Amazon Web Services (AWS) grew 28% in Q1, its fastest pace in 15 quarters; Alphabet’s Google Cloud grew 63%, accelerating from 48%; Microsoft’s Azure grew 39%. Three of the largest businesses in the world stepped up their growth rates simultaneously – generating tens of billions in extra revenues – and the demand drivers underneath are not what consensus is pricing.

Compute demand is now driven by four scaling laws, up from three in December: pre-training, post-training, reasoning, and now agentic workloads. Anthropic’s Mythos model result confirmed that bigger models trained on more compute still produce step-changes in capability – pre-training is not done.

The new variable is agentic AI, which is already c.10,000x more compute-intensive than a single-shot chatbot answer and this is only around four months into its evolution. Each agentic task is a step-function in tokens per query – the units of data processed by AI – not a linear increment: workloads run for hours, tool-call recursively, and consume both GPU and CPU at scale.

The 2024–25 industry buildout was about creating capacity. 2026–27 is when that capacity starts selling into high-volume inference, which is also why free cash flow compresses further through 2027 before re-inflecting hard on the other side.

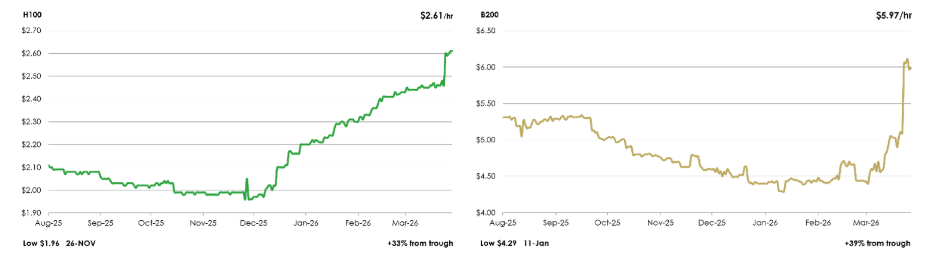

Surging GPU spot rental prices ($/hour)

Source: Bloomberg, August 2025 to March 2026. SDH100RT Index, SDB200RT Index.

The return on investment (ROI) debate in our view is over. Anthropic's revenue run-rate of $30bn at inference gross margins in the 45–75% range exemplifies the core economic point: at scale, the marginal cost of producing intelligence collapses. The bear case required either revenue not to materialise or unit economics to be permanently broken. Neither has held.

What separates the winners from here is full-stack ownership, and two capabilities matter most: custom silicon and access to a world-class first-party model. The cloud operators who own both will earn structurally better unit economics, capture demand origination from their own products, and optimise the entire silicon-to-model stack around the workloads that actually run on it. AWS and Google own both. Microsoft owns neither at the required scale.

Custom silicon is now the dividing line on inference economics. Nvidia remains the best architecture and Blackwell/Rubin are sold out; TPUs are the next-best scaled alternative. AWS’s AI accelerator, Trainium, does not need to match either – it needs to be good enough, available, cheaper at scale, and tightly optimised around Claude and Bedrock workloads. Trainium commitments now exceed $225bn, with Trainium2 largely sold out, Trainium3 nearly fully subscribed, and most of Trainium4 already reserved. AWS chips are running at $20bn of internal revenue and would be c.$50bn run rate if accounted for as a third-party chip business. The under-discussed second piece is Graviton, AWS’s CPU: agentic AI requires c.120 million CPU cores per gigawatt versus c.30 million for traditional AI, a 4x increase, and Graviton offers c.40% better price performance versus x86.

Every agentic task – tool calls, container orchestration, scheduling, memory management – is CPU work, and AWS owns both sides of the stack. Google's TPU programme is a decade old, deeply embedded in Gemini training and inference, and is the only credible scaled alternative to Nvidia outside AWS. Microsoft has Maia, but Maia is a vastly inferior chip. Without scaled in-house silicon, Microsoft pays Nvidia margins on most of its compute bill in perpetuity while AWS and Google (Alphabet) capture them internally.

Owning a world-class first-party model is the second competitive advantage, and it is not just a model story – it is a demand-origination and unit-economics advantage. The cloud with a frontier model is not waiting for workloads; it is creating them, embedding them into owned products, and routing them onto its own infrastructure. That improves utilisation, capacity visibility and unit economics, because silicon, networking and orchestration can all be optimised around the model architecture they are actually serving. Google leads clearly here: Gemini and DeepMind, TPUs underneath, distribution through Search, YouTube, Android and Workspace – the cleanest full stack in the industry.

AWS is credible through Bedrock, Anthropic and Nova: although Anthropic is distributed across all three clouds, the centre of gravity is AWS, with over 100,000 enterprise customers running Claude on Bedrock, Anthropic using over a million Trainium2 chips, and a $100bn ten-year commitment for up to 5GW of AWS capacity across Trainium2–4. Google's TPU ramp for Anthropic in 2026 is comparable in scale. Microsoft has no first-party frontier model and is therefore dependent on partners for the layer that drives token demand and inference economics – and with OpenAI exclusivity now gone, that dependency has become an exposure.

The end of OpenAI–Microsoft exclusivity is the biggest re-allocation of AI compute demand of this cycle. AWS picks up roughly $38bn of OpenAI compute, Oracle picks up c.$300bn over five years, and GCP is a credible third destination. The recent selloff in OpenAI-exposed names conflates weaker OpenAI consumer growth with weaker AI demand. They are not the same thing. Missed internal user targets tell us OpenAI's consumer trajectory is not perfectly linear; they do not tell us AI demand is weakening. The clearer interpretation is that OpenAI is shifting towards the higher-quality profit pools – enterprise, coding and agentic workflows – and the proof points are GPT 5.5 and Codex. GPT 5.5 is OpenAI's first new pre-train since GPT 4, more than two years ago, and a significant leap forward, competitive with Anthropic’s Opus 4.7 across multiple benchmarks and better at many tasks. Codex weekly developer count rose from 3mn to 4mn in two weeks, scaling rapidly into the highest-value enterprise workflow.

Microsoft is now in the innovator's dilemma, and the dilemma sharpens the faster Azure grows. The compute it rents to AI labs is being used to build the products that commoditise the per-seat software model underwriting Microsoft 365. If software consumption migrates from human seats to AI agents – which is exactly what GPT 5.5, Claude Cowork and Codex are designed to do – the economics of the most profitable software business in history invert. Microsoft can either invest harder into Azure and accelerate the disruption of its own legacy suite or invest more into Copilot to defend M365 and sacrifice Azure growth. Every other hyperscaler is attacking that profit pool from the outside. Microsoft has to attack it from the inside while simultaneously defending it. Compounding the issue, OpenAI's enterprise business at 3 million paying users (up 50% in a few months) is itself a Copilot competitor, and it sits on the same architecture Microsoft helped build.

Meta sits in a different category and is delivering the clearest AI ROI of the four today. Every other hyperscaler is rationing compute between external customers, internal workloads and strategic lab investments. At Meta, every GPU goes straight into products with an at-scale advertising engine already attached. Better recommendations drive more engagement, better targeting drives better ad ROI, better creative tools expand advertiser demand, and the existing ad auction monetises all of it immediately – a feedback loop that has now shown up in the numbers for four consecutive quarters. Capex of $125–145bn is, in this frame, a rational allocation, but we see greater upside today in those hyperscalers providing external compute to the AI labs.

Finally, the free cash flow (FCF) question: aggregate hyperscaler FCF will compress further through 2027 – longer than the market is modelling. We do not think this is what investors should focus on. Cloud revenues inflecting today will translate to cashflows once we are past peak build. Yes, AWS free cash flow alone collapsed from $26bn to $1.2bn year on year in Q1, but this is not the cycle ending; it is the cycle being prepaid. Land, power, buildings, chips and networking gear are funded six-to-twenty-four months ahead of customer billing. The original AWS buildout produced a similar pattern through the late 2000s and ultimately delivered the highest-returning enterprise asset of the past two decades. The playbook is the same today, just at much larger scale with economics arriving much sooner. This time the customer commitments are on the books before the assets come online. AWS backlog is $364bn excluding the $100bn Anthropic commitment. Google Cloud backlog almost doubled sequentially to $462bn. The monetisation curve is locked in, and FCF re-inflects once the build moderates and the installed base ramps.

Read, watch and listen to more insights from Liontrust fund managers here >

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

The Funds managed by the Global Innovation team:

-

May consider environmental, social and governance ("ESG") characteristics of issuers when selecting investments for the Funds.

-

May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund.

-

May have a concentrated portfolio, i.e. hold a limited number of investments or have significant sector or factor exposures. If one of these investments or sectors / factors fall in value this can have a greater impact on the Fund's value than if it held a larger number of investments across a more diversified portfolio.

-

May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings.

-

Do not guarantee a level of income.

The risks detailed above are reflective of the full range of Funds managed by the Global Innovation team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.com or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.