Knowing when to abandon an underperforming fund manager is one of the hardest judgments investors face, according to Juliet Schooling Latter, research director at FundCalibre.

“The hardest, and often most valuable, skill for investors is knowing the difference” between a strategy that is temporarily out of favour and one that has become genuinely obsolete, she said.

Her comments come as quality-growth strategies, which dominated the previous decade, have struggled in recent years, with well-known managers having had to apologise for and justify their underperformance.

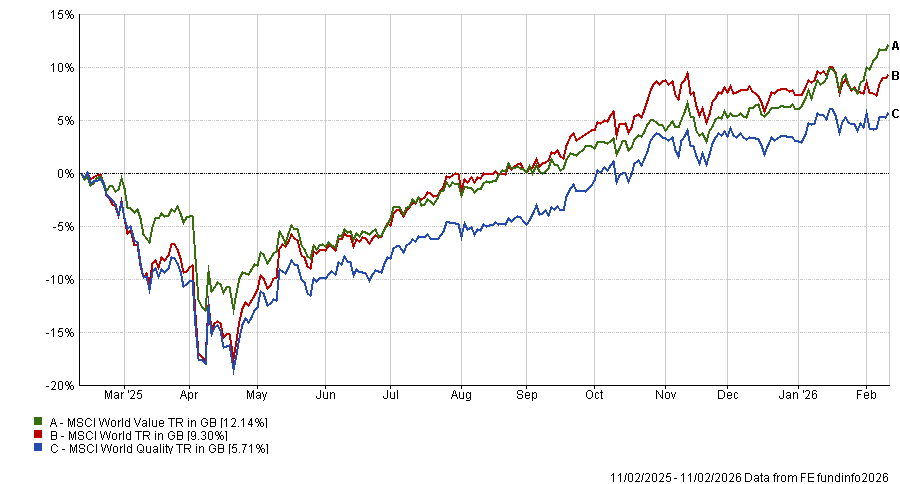

Performance of indices over 1yr

Source: FE Analytics

But Schooling Latter argued that short-term underperformance driven by style cycles should not be confused with strategic failure.

“Styles fall in and out of favour, sometimes for years at a time, and abandoning a clearly articulated process simply because it's underperforming can be far more damaging than sticking with it,” she said. “Investors should judge managers on whether they are doing what they said they would do, not on short-term relative returns driven by style cycles.”

That distinction matters because hasty decisions can lock in losses just before a strategy comes back into favour. Value investors who abandoned their managers during the 2010s, when growth dominated, would have missed the subsequent reversal. The same principle applies in reverse today.

Yet patience does not mean blind loyalty. Investment strategies must evolve with markets and good managers should be capable of thoughtful adaptation.

“Tweaks within a framework, made transparently and communicated clearly to investors, can make sense,” Schooling Latter said. “Successful managers adapt at the margins rather than tearing up their playbook.”

She pointed to FE fundinfo Alpha Manager James Thomson's addition of a ‘defensive growth’ bucket to the Rathbone Global Opportunities as an example. In 2008, Thomson introduced more resilient, lower-beta companies alongside his core growth holdings while remaining true to his philosophy. The key, Schooling Latter said, is that such changes must be clearly explained and openly communicated.

Performance of fund against index and sector over 1yr

Source: FE Analytics

Wholesale style shifts are a different matter. “Genuine style changes are rare and risky,” she said. Even Warren Buffett's gradual evolution from deep value towards quality was grounded in the same discipline rather than a reactive pivot. By contrast, wholesale shifts, especially those made quietly, risk eroding trust and can stray into mis-selling territory.

Marcus Brookes, chief investment officer at Quilter, said investors need a strong sense of the environments in which a manager or style should perform well or badly. Without this, it becomes impossible to assess whether strong performance has just been lucky or whether weak performance is explainable.

For quality-growth strategies, Brookes outlined four scenarios where the approach should excel: economic downturns, when investors value predictability and stability; falling markets, when risk appetite sours; periods of low interest rates and inflation, when the present value of future earnings is less heavily discounted; and when the past is a good guide to the future, allowing quality businesses with strong earnings histories to continue compounding.

“None of these scenarios have played out so far this decade, with strong economic growth and equity markets going on a tear and the MSCI ACWI almost doubling in value since the start of 2020,” Brookes said.

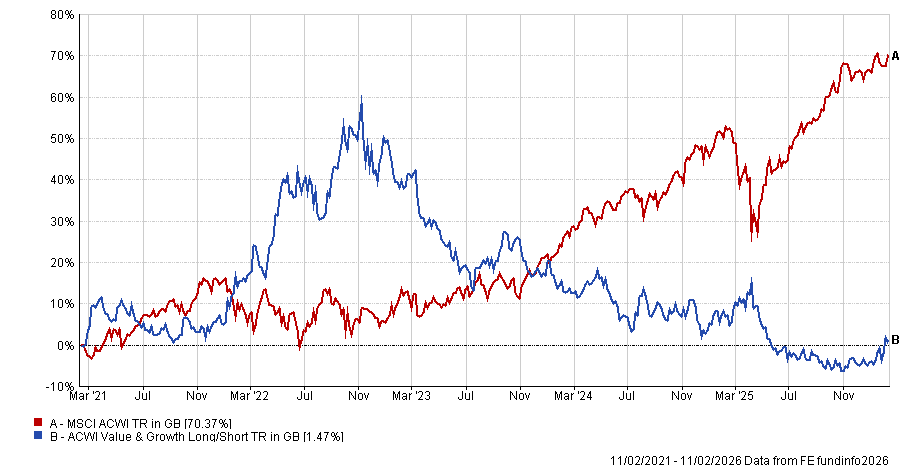

Performance of indices over 5yrs

Source: FE Analytics

There have been brief disruptions, such as the first half of 2022 and Liberation Day in April 2025, when quality managers outperformed during these episodes. However, rising interest rates and bond yields moving higher have plagued returns for most of the past few years.

“So, it is understandable that the investment style has been something of a dog in recent years," Brookes said. “If the environment changes, and it will at some point (although maybe we've seen the last of zero interest rates for a while) then the stage is set for quality-growth to come roaring back.”

However, AI is complicating the picture by disrupting business models across sectors – including quality-growth companies.

“Businesses that just a few years ago had almost unassailable competitive positions can now come under pressure overnight,” Brookes continued. “This increases the downside risks for these businesses and for their share prices, and means the way quality-growth managers deliver returns will be lumpier.”

The question, then, is whether this disruption means the style is broken.

"Not necessarily, but what you can expect from them is certainly different now," he said. "So, if you are looking for a steady compounder for your portfolio, then strategies like this don't fit the bill anymore."

Quality-growth may eventually roar back when conditions turn but the path will be rougher than in the past and, in the mean time, a strategy can still work without delivering what investors originally bought it for.

Schooling Latter concluded: “Strategies don't become obsolete overnight. They become obsolete when the underlying rationale no longer holds – not simply when performance is out of fashion."

The challenge for investors is recognising which they are dealing with.