Britons remain famous for their love of queuing, instinctively adhering to the unwritten rule that they form an orderly line when more than one person is waiting for the same thing.

This little ritual helps to preserve a sense of fairness, speeds up the provision of services and avoids the unpleasant scenario of a free-for-all. Yet there are times when sticking rigidly to this social convention can be counterproductive – and I’m not just talking about the post-pandemic phenomenon of queuing at the bar.

When your turn has come but your mind is elsewhere and you ignore the less-than-subtle hints from those standing behind you, can you really blame them if they push in?

Outflows

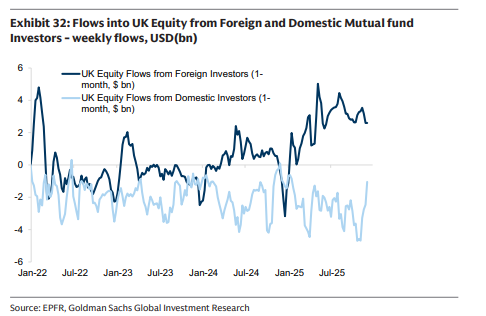

UK investors pulled a net £9.5bn from domestic equities last year. I suppose you could argue that this hardly constitutes ‘news’ – they pulled a similar amount of money from UK equities in 2024 and the asset class has now seen net outflows in every year since 2016.

What makes the statistic interesting is that it came in a year when the FTSE All-Share returned 24% – more than twice as much as the S&P 500. Us Britons may not be buying UK shares, but someone is.

Even after such a strong run, the price-to-earnings (P/E) ratio of the UK market sits well below the global average (this remains true even if you remove the US).

But there is a sector that sits on a further 20% discount to the large-caps that drove the FTSE All-Share’s performance last year – UK small-caps.

Talking down the UK

It’s sometimes difficult to put into words just how unpopular this sector is. The small-cap market derives about 60% of revenues from the domestic economy (compared with just 20% for large-caps), which over the past decade has been hit by Brexit, Covid and higher interest rates.

And don’t we know it: in any year without a World Cup, it is not queuing but bashing the UK that becomes our national pastime.

Despite all the negativity and market shocks of the past decade, our Artemis UK Smaller Companies fund managed to return 100%. There is no real secret here: we invest in undervalued companies that have strong balance sheets and are generating healthy levels of free cashflow.

When the market gets cheaper – and it has seen net outflows in nine of the past 10 years – takeovers and share buybacks become more prevalent. These will continue to drive returns if the sector sees similar headwinds over the next decade as the past.

Headwinds to tailwinds

But here’s the thing. Not only do we think we are unlikely to see similar headwinds over the next decade, we believe many of them are now turning into tailwinds.

The government is working towards greater integration with the EU. Interest rates are falling rather than rising. And it is becoming harder to see where the marginal seller will come from.

This last point is perhaps the most important one. The reason why the 20% discount to large-caps is so interesting is that small-caps have traditionally traded at a premium. And with good reason – they have delivered much higher returns over the long term.

The economy is stronger than you think

Based on the overwhelming narrative of negativity around the UK, it would be entirely rational to expect this discount to persist. However, this pessimism is at odds with what we are seeing at the company level.

Pub chain Fuller’s recently reported first-half earnings per share up 37%; package holiday operator On The Beach reported first-half earnings per share up 14%; and sofa retailer DFS reported full-year profit before tax up 188%.

These are not supposed to be representative, but they should serve as a reminder that, even for businesses exposed to discretionary consumer purchases, things are better than widely perceived.

And rather than getting worse, we think they could get better still. If, as expected, there is no spike in unemployment, confidence should improve and consumer spending (which makes up 60% of the economy) would recover.

The money is there – the savings ratio currently stands at 9.5%, close to twice its pre-Covid level. It is estimated that a single percentage point fall in this figure would provide a £17bn boost to the economy.

Creating a ‘growth loop’

What happens if this finally convinces investors to return to UK small-caps? Well, we could see a virtuous circle or ‘growth loop’. Increased investment. Faster growth. Rising confidence. Further fund inflows.

How does this work? Fund inflows reduce companies’ cost of capital as their share prices rise. A lower cost of capital reduces the required-rate-of-return hurdle that companies must exceed to justify investment. Higher investment boosts productivity and UK growth. Critically, investors who are early would also be handsomely rewarded through strong equity returns as share prices re-rate upwards.

Such a trend could finally help dispel the negativity around the UK. And remember, there’s a World Cup this year. But could it convince UK investors to start buying UK smaller companies once again?

We’re not sure it matters – there is no polite queuing system here. If they don’t, then someone else will.

Will Tamworth is co-manager of the Artemis UK Future Leaders investment trust and Artemis UK Smaller Companies fund. The views expressed above should not be taken as investment advice.