Liontrust Special Situations was once a multi-billion-pound flagship fund in the UK equity space but in recent years it has struggled to stem the tide of redemptions as investors have grown increasingly uneasy with its prolonged spell of underperformance.

The fund’s assets under management (AUM) has fallen sharply from highs of £6.5bn at the start of 2022, halving to £3.2bn in late 2024 and falling further to £988.7m as of 31 January 2026.

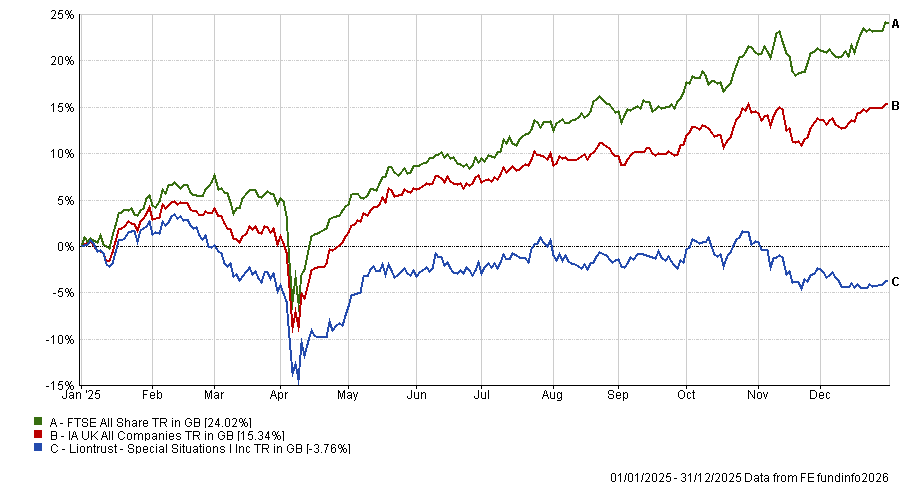

It has posted losses in four of the past 10 calendar years – most recently losing 3.8% in 2025.

This left the strategy well adrift of the IA UK All Companies average, which was up 15.4% by the end of the year – placing Liontrust Special Situations among the five worst performers in the sector for 2025. It also fell far short of the FTSE All Share, which rose by 24% in 2025, bolstered by FTSE 100 stocks.

Fund performance vs the benchmark and sector in 2025

Source: FE Analytics

According to fund selectors, much of this underperformance boils down to the strategy’s stylistic tilt, with Liontrust Special Situations hunting for quality businesses with long-term compounding potential.

Quality investing is typically popular during times of zero interest rates and low bond yields – which does not reflect today’s landscape.

John Monaghan, research director at Titan Square Mile, said: “In contrast, value has been the dominant investment style and is an area this fund is unlikely to be exposed to.”

For example, no major UK banks are held by the fund as they do not meet its quality threshold.

“Exposures to the standout performers in the defence-related space, such as Rolls-Royce and BAE, were also absent, which was a further key detractor,” Monaghan added.

“Based on recent returns, the adherence to the investment style could arguably be considered a negative as in some quarters it might be described as dogmatic and inflexible.”

Investment style is not the only headwind the Liontrust fund faces.

Through its established Economic Advantage investment process, which allows the fund to allocate across the FTSE 100, FTSE 250 and AIM indices, the fund has a heavy exposure to small- and mid-caps, currently in excess of 50%.

“To provide some context of market capitalisation returns, the FTSE 100 returned 25.8% in 2025, the FTSE 250 ex investment trusts (as a measure for mid-caps), rose by 12.5% and the FTSE Small Cap index was up by 10.9%,” said Monaghan.

Within the fund’s small- to mid-cap exposure, there is an around 25% exposure to AIM-listed companies, yet the FTSE AIM market lagged the aforementioned indices, gaining 8.5% in 2025.

In addition to the stylistic and market-cap headwinds, the fund also had issues with stock selection, according to Monaghan, who pointed to “key problematic investments, such as RWS (which is now sold), GlobalData and Gamma Communications.

On top of this, Jack Driscoll, fund analyst at FE Investments, noted that the continued fund outflows “can become a further headwind in their own right, [as] outflows can pressure liquidity management in an already difficult period”.

The fund was removed from Bestinvest’s Best Funds List in 2021, with analysts citing worries that its high exposure to small- and mid-caps, combined with the fund’s declining scale, risked creating liquidity challenges.

Mere months later, interactive investor also cut the strategy from its Super 60 best-buy list, indicating reduced confidence in the fund’s ability to navigate difficult market conditions.

So should you buy, hold or fold?

Given the fund’s shrinking size and variable returns, is now an opportunity to buy into a long-established strategy at a low ebb? Or is the writing on the wall?

Rob Morgan, chief analyst at Charles Stanley Direct, said: “The contrarian in me eyes an opportunity here, as the fund has good managers with a decent process and, following significant outflows, a relatively nimble vehicle with which to apply it.”

For existing investors who have “taken a considerable amount of pain, I think investors should hang on at this point – and the contrarian-minded should consider topping up or buying in anticipation of quality businesses returning to the fore”, he added.

Meanwhile, Sheridan Admans, director at Infundly, said he would hold the fund at this time, noting that many of the issues plaguing the Liontrust fund appear cyclical rather than structural.

“Many of the portfolio companies continue to deliver resilient earnings, strong cashflows and durable competitive advantages,” he said, pointing to core holdings such as RELX, Experian and Unilever – “durable companies with competitive moats and strong returns on capital which have demonstrated earnings resilience”.

“Selling now risks exiting as quality-growth valuations reset and macro conditions – peaking rates and moderating inflation – become more supportive,” Admans said.

However, he said folding may become necessary if “outflows accelerate materially, performance fails to recover across a full cycle or evidence of process drift emerges”.

To balance the Liontrust fund’s style exposure and sector tilts, Admans suggested holding TM Oberon UK Special Situations and/or Jupiter UK Dynamic Equity. He said the former adds cyclical and financial exposure and can benefit from re-rating catalysts, while the latter has a more defensive value tilt.

Monaghan said he would also hold, pointing to the stability of the management team and the ongoing adherence to a tried and tested process that has been successful over the long-term.

FE fundinfo Alpha Manager Anthony Cross – who has managed the fund since it was launched in 2005 – remains lead manager, following the retirement of his co-manager Julian Fosh last year. He is supported by Victoria Stevens and Matthew Tonge who were appointed in 2025.

In addition, Monaghan said the multi-cap, quality-oriented approach has very few direct peers and so provides exposure to an element of the market that cannot be easily found.

“We see the underlying portfolio as very attractively valued versus its history and should the current headwinds switch into tailwinds it is well positioned to perform well,” he said.

Despite the outflows Monaghan said “currently we do not have any concerns over its viability with assets still around the £1bn level”.

For investors choosing to hold, complementary funds “would be those with virtually the opposite characteristics – so more cyclically sensitive and managed with a value mindset”, Monaghan said, pointing to funds like Fidelity Special Situations and Man Income.

Meanwhile, Driscoll said he would fold.

“[Underperformance] has been persistent enough to raise questions about whether the strategy is structurally out of step with the current market regime,” he said.

“Even if you believe a style recovery is possible, there are alternative ways to access UK equities where the balance of recent execution, portfolio resilience and investor sentiment looks better.”

Driscoll noted that existing investors in the fund with long-term conviction “could justify a hold but they should be comfortable with ongoing volatility and the chance that the turnaround takes times”.

Similar funds which Driscoll prefers are Fidelity UK Special Situations and JPM UK Dynamic.