With more young people pursuing higher education while the price of a degree continues to climb, increasing numbers are graduating with sizeable debts.

The Department of Education estimates that full-time undergraduates starting in 2024/25 will borrow an average of £44,690 during their studies, with just over half expected to repay the full amount.

Under Plan 5 – which applies to students starting from 2023 – repayments begin once earnings exceed £25,000, with a 9% charge on anything above that.

Interest accrues from the first payment made to the individual or university and continues to build until the loan is repaid or the full term of the loan agreement elapses and the remainder is written off – for borrowers under Plan 5, this is 40 years. Last year, the rate of interest for Plan 5 loans was 4.3% – the year before, it was 8%.

This means the average student’s debt balance can rise quickly. Dan Coatsworth, head of markets at AJ Bell, noted that 2024/25 undergraduates will likely amass £53,000 in debt at the end of their period of study which, when applying a conservative estimate of 5% annual interest, means the amount owed will grow to over £86,000 in 10 years.

Given how quickly this debt can accumulate and how long it lingers, a Junior ISA (JISA) is one way in which families can build a pot to offset future university costs.

Up to £9,000 can be paid by parents into a JISA tax-free each tax year.

According to AJ Bell data, if parents paid £750 per month into a cash JISA from their child’s 11th birthday, they would have a pot worth £67,675 at the end of the seven-year period, assuming 2% interest paid monthly. Had that money been invested in the market, such as in the Vanguard FTSE All World ETF, the Junior ISA would be worth £100,143.

But what other funds would fund selectors consider in a JISA with this specific goal?

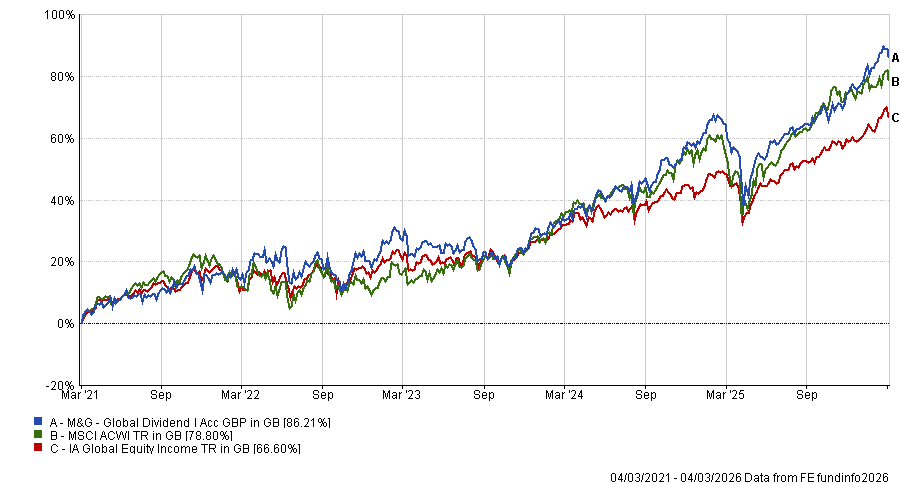

Rob Morgan, chief analyst at Charles Stanley, suggested M&G Global Dividend as “a great longer-term holding to help drive more consistent performance across market cycles”, adding that yielding stocks tend to be less volatile, while the flow of dividends can bolster returns during leaner periods.

When the child turns 18 and the JISA becomes a standard ISA, Morgan said the units could be switched from accumulation to income – “effectively turning the tap on an income stream that could help towards education costs”.

The fund, which is managed by Stuart Rhodes, invests in a broad range of income stocks spanning quality companies, those with asset backing and faster growing opportunities. As such, Morgan said “it is a well-balanced fund in its own right, or a good option for diversification when held with a growth fund or global tracker”.

M&G Global Dividend has beaten the IA Global Equity Income sector average return in five out of the past 10 years. Notably, it delivered a top-quartile return of 4.6% in 2022, a bad year for equities, while the sector average was a 1.2% loss and MSCI ACWI fell 8.1%.

Performance of the fund vs sector and benchmark over 5yrs

Source: FE Analytics

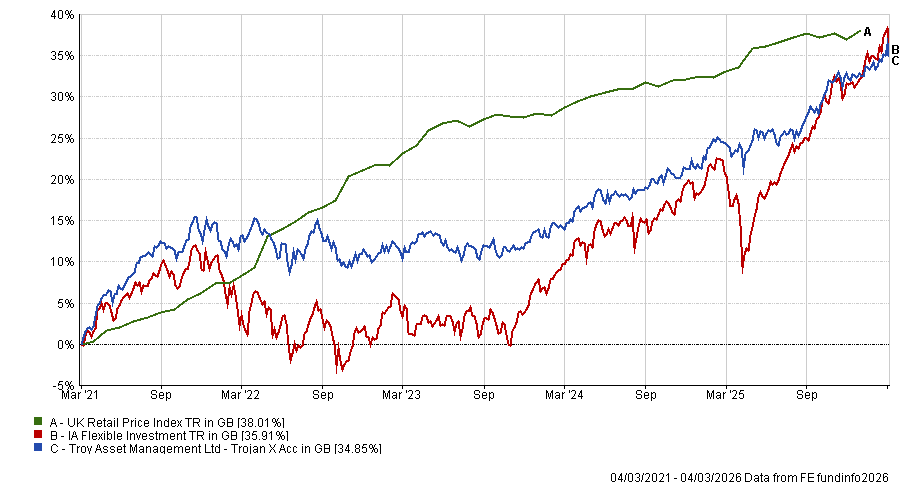

Meanwhile, Sheridan Admans, founder of Infundly, said a JISA needs both long-term growth and risk control, suggesting a blend of Nutshell Growth and Trojan, with the former serving as “the growth engine” of the JISA and the latter “providing balance”.

Managed by Mark Ellis since its 2020 inception, the Nutshell fund holds around 30 high-quality global stocks demonstrating strong profitability and cash generation – purchased at sensible valuations.

“This disciplined ‘quality at a reasonable price’ approach has historically delivered solid long-term growth with lower volatility than many global growth peers, making it well suited to compounding over a medium- to longer-term horizon,” said Admans.

With over half of its assets allocated to the telecom, media and technology sector, the vehicle is clearly tilted toward growth, with its top 10 holdings – which make up 57.7% of the fund – currently including Adobe and ASML.

The strategy has delivered an annualised return of 13.7% in sterling terms since inception.

Meanwhile, Admans said Troy’s £5.2bn Trojan fund will protect capital in downturns through its high exposure to gold and bonds, maintaining notably low volatility and limited sensitivity to broader equity market movements.

“This will help to ensure accumulated gains are still there when university costs arise,” Admans said.

Its current biggest position is in Invesco Gold ETC, which makes up 6% of the portfolio.

Performance of the fund vs sector and benchmark over 5yrs

Source: FE Analytics

“For parents starting saving later in their child’s life, for example at age 11, a higher allocation to Trojan may be prudent to protect accumulated gains,” he said.

“For those starting earlier, a heavier weighting to Nutshell allows time to absorb volatility while targeting stronger long-term growth.”

Simon Woodacre, fund research analyst at Quilter Cheviot, made two fund suggestions covering lower-risk and higher-risk appetites.

For those wanting a lower-risk option, he pointed to the £282.6m TM Redwheel Global Equity Income fund, which is led by Nick Clay and targets capital and income growth with a low turnover, a yield of around 3% and a long investment timeframe.

Its greater levels of downside market protection “make the fund suitable for clients with a variety of different timescales, however, it would still be best used at the earlier stages of the child’s life in order to benefit from the long-term effects of compounding and to provide more diversification to the rest of the portfolio”, Woodacre said.

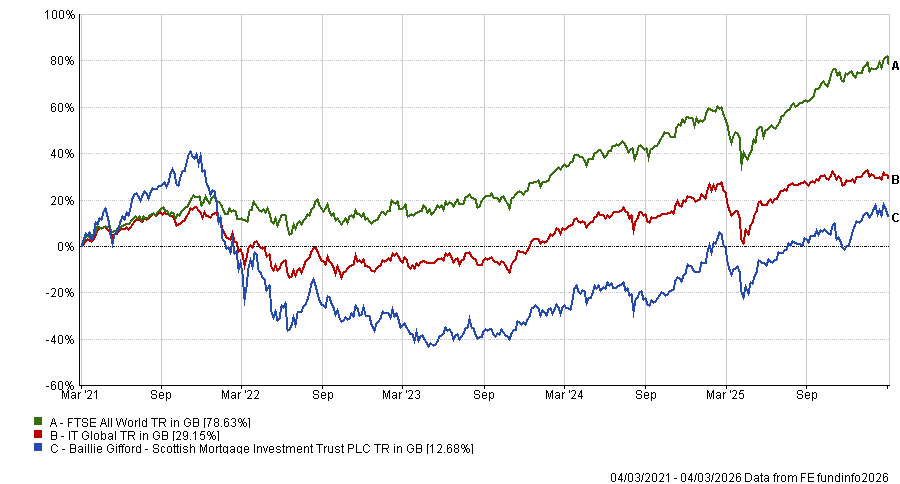

A higher risk option is Scottish Mortgage Investment Trust – a £13bn vehicle that invests in a combination of global private and public companies deemed innovators among their peers.

FE fundinfo Alpha Manager Tom Slater and deputy manager Lawrence Burns typically hold investments for long periods with limited turnover, meaning the trust is suitable for long-term objectives such as university fee planning, Woodacre said.

“The trust has also invested in pioneering businesses such as Anthropic and SpaceX, which could compound returns over time and help grow the portfolio to a meaningful size by the time the child needs to pay for university fees,” he said.

It has delivered strong returns over one, three and 10-year periods to the end of February 2026, gaining 19.3%, 76.1% and 425.9% respectively – although its five-year performance is slightly weaker due to a large drawdown during the interest rate hiking cycle of 2022.

“The trust should primarily act as a source of alpha generation within the portfolio,” Woodacre said.

Performance of the fund vs sector and benchmark over 5yrs

Source: FE Analytics

In contrast, Anthony Snowden, private client investment director at Tyndall Investment Management, said he likes the concept of pairing a trend following fund alongside a thematic option.

He selected the MontLake DUNN WMA Institutional UCITS Fund – a long-running commodity trading advisor (CTA) strategy – and WisdomTree Megatrends UCITS ETF.

CTAs are regulated managers that run systematic, futures-based trading programmes using trend-following models to capture moves across global markets.

“Unlike many other CTAs, MontLake DUNN WMA Institutional UCITS Fund currently has an around 40% exposure to commodity markets,” Snowden said, noting its strong longstanding record adapting to changing trends across equities, bonds, commodities and currencies.

In contrast, the WisdomTree exchange-traded fund (ETF) systematically allocates capital to a curated selection of themes, including quantum computing, Chinese technology, AI and blockchain.

“Spreading across multiple themes avoids the risks of being incorrect or swept up in fads, yet remaining exposed to growth sectors that will shape our world and investment markets over the coming decade,” Snowden said.