Investors dream of picking the next FTSE 100 stock when it is a fledgling business and owning it through its progression to the large-cap sphere.

Finding the next index heavyweight is far from an easy feat – particularly in the UK, where the international rivals and private equity tend to take out companies before they ever reach their full potential.

Below, Trustnet asked two smaller companies specialists for a stock they believe can make it to the upper echelons of the UK market while avoiding takeovers.

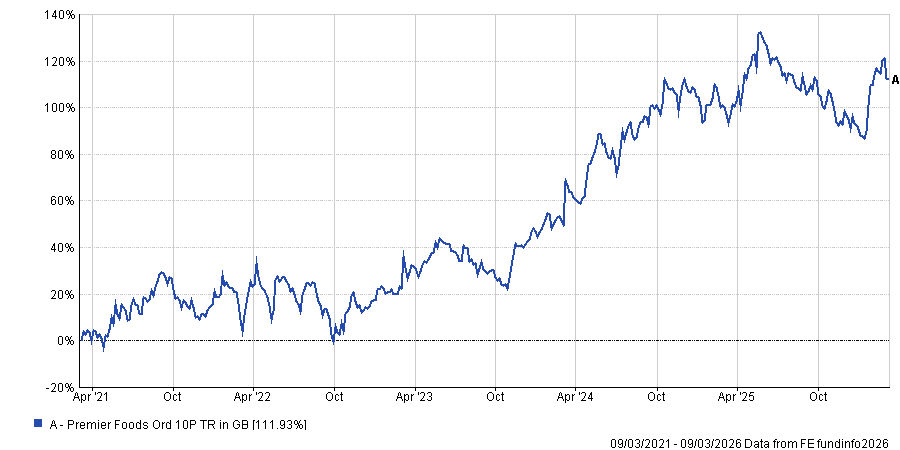

For FE fundinfo Alpha Manager Paul Marriage, the answer lies in a great UK consumer brands stock: Premier Foods. With a market capitalisation of £1.6bn, the stock currently sits in the middle of the FTSE 250.

The co-manager of the £57.4m Premier Miton Tellworth UK Smaller Companies fund said the company behind brands such as Bisto gravy, Mr Kipling cakes and Sharwood’s sauces (among others) is “one of the best opportunities in consumer staples”.

“It has done all the right things. It has done great M&A, sorted out its pension scheme, fixed the balance sheet and is now throwing off cash,” said Marriage.

“That is the stock I look at the most and say: Yeah, that’s a FTSE 100 stock in the making.”

Total return of stock over 5yrs

Source: FE Analytics

Premier Foods has been “historically undervalued by the market”, but is now run by an “entrepreneurial management team” who is “doing the right things”.

One issue is that the company is heavily tied to the UK consumer, with roughly 90% of its earnings coming from the UK and smaller sales to the US and Australia.

However, Marriage noted that the business should continue to perform as the UK consumer has remained notably resilient despite higher inflation in recent years. It also should do well if economic conditions worsen, as people tend to cook more at home and spend less on meals out.

“A lot of its products are remarkably simple and [Premier Foods] does them well. They’re popular sellers. The nation still likes its staples. People like good value, good quality and to know what they’re getting,” said Marriage.

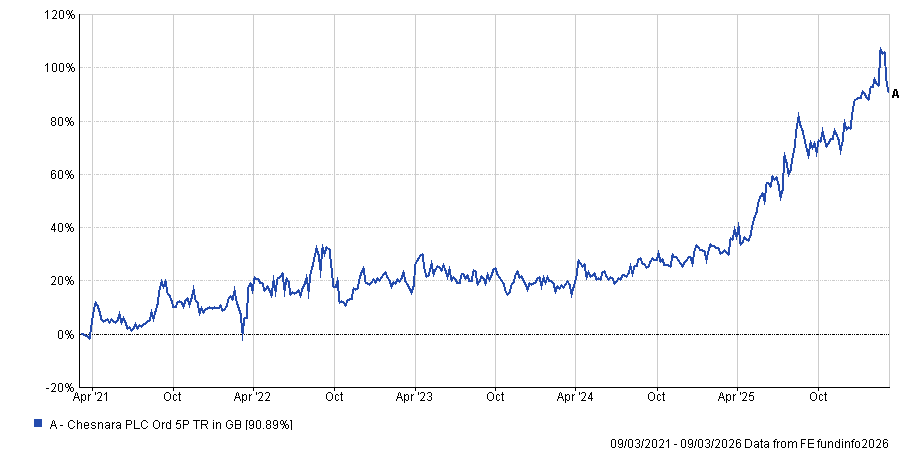

Eustace Santa Barbara, manager of the £455m IFSL Marlborough Special Situations fund, chose a company closer to the bottom of the FTSE 250: Chesnara.

The £725m life insurance firm is one the manager “would love to see” in the FTSE 100 in the future. He described the company as a “grinder” rather than a “flyer”, but said that it is currently in a bit of a “sweet spot”.

It is run by “a very good management team with good track record” and currently pays a dividend yield of above 7%.

Total return of stock over 5yrs

Source: FE Analytics

But it is not standing still. Chesnara is conducting acquisitions, buying up books of life insurance from “ambivalent sellers”, such as its acquisition of HSBC’s life book last summer.

The firm raised equity to conduct the purchase, which improved its market capitalisation significantly and provided additional liquidity.

This is at a time when regulators are nervous about private equity entering the sector. Santa Barbara pointed to an example in Italy, where Eurovita (owned by UK private equity firm Cinven) was placed under special administration.

As interest rates surged, mass redemptions caused a liquidity squeeze, with Cinven unwilling to inject cash to support the firm, leading to a rescue deal by other insurers.

Stocks that could get taken out before they reach their full potential

Mergers and acquisitions have been a large part of the UK market in recent years as international investors have pounced on domestically listed companies across the market capitalisation spectrum.

Both managers acknowledged there are stocks with large potential that could be bought out before they reach their full heights.

They expected M&A activity to continue, with Santa Barbara noting that there could be more to come as interest rates have fallen in the past 24 months, making it cheaper for companies to borrow money to afford takeovers.

Meanwhile, valuations remain cheap relative to other market equities, with Marriage adding that the valuation gap remains hard to fix.

“You come into every year thinking: Maybe this year the valuation gap closes. And then usually something happens in the first quarter that kills that for Q2 and Q3. Then in the fourth quarter there is optimism again. This is exactly what’s happened 2023, 2024, 2025,” he said.

Santa Barbara said real estate investment trusts (REITs) such as New River Reit could be the subject of future takeovers, with the investment trust space currently undergoing a period of transition and many private equity firms looking to buy assets for cheap.

Marriage agreed, noting that property is an area of M&A interest, but noted that Advanced Medical solutions (AMS) could be another to receive bid interest.

“It had a bid before. It strikes me as a high-quality business that is getting better, with resilient earnings and no AI threat. I can see that going out,” he said.

The manager said he has “loads” of companies that could be bought as non-market participants are valuing his stocks at around 50% more than the market.

However, he is not concerned by this. “I’ll take the performance,” he said.