Fund managers are positioning portfolios to cope with stagflation as the rising oil price threatens to choke economic growth while pushing inflation higher, a closely watched survey suggests.

On 28 February 2026, the United States and Israel began a series of strikes against Iran, targeting its nuclear and ballistic missile programme and aiming to induce regime change. The closure of the Strait of Hormuz, through which roughly 20% of global energy supplies pass, has pushed Brent crude above $100 a barrel and sent fund managers scrambling to reprice the global economic outlook.

Bank of America’s latest Global Fund Manager Survey shows a sharp rotation out of cyclical assets and into defensive positioning as professional investors respond to the fastest deterioration in sentiment in months.

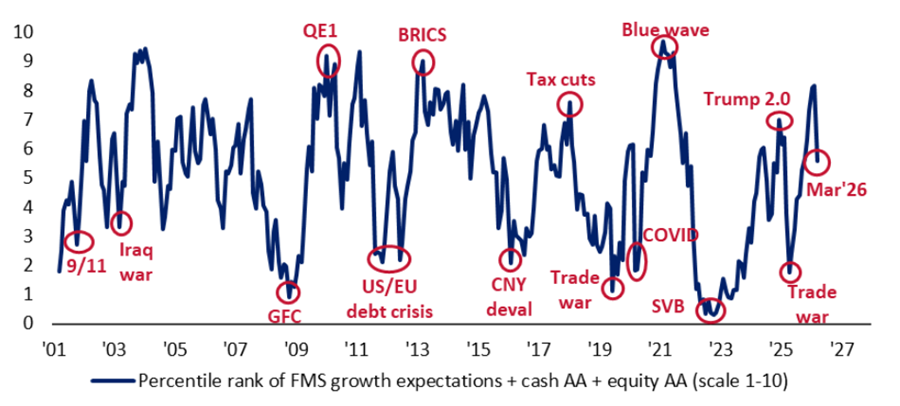

Fund managers’ current sentiment

Source: BofA Global Fund Manager Survey, Mar 2026

The survey’s composite sentiment index, which tracks fund managers’ cash levels, equity allocation and global growth expectations, has fallen from 8.2 in February to a six-month low of 5.6. Iran tensions and private credit concerns ended what Bank of America described as “frothy bull” sentiment that had defined the survey’s tone in recent months.

Despite the scale of the move, the reading sits well above the April 2025 low of 1.8, when the index approached panic territory in response to US president Donald Trump’s ‘Liberation Day’ tariffs.

The macro drivers behind the drop are, unsurprisingly, the US/Israeli attacks on Iran. Geopolitical conflict surged to the number one tail risk in March, cited by 37% of respondents, up sharply from 14% the prior month and displacing AI bubble fears, which fell to just 10%.

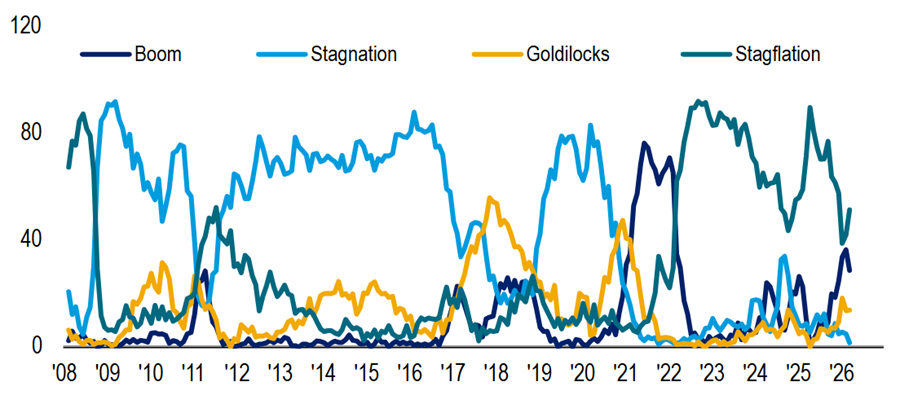

Fund managers’ economic expectations

Source: BofA Global Fund Manager Survey, Mar 2026

Stagflation, defined as below-trend growth with above-trend inflation, is now the dominant macro expectation among the survey’s respondents at 51%, up from 42% a month ago.

The ‘boom’ scenario, combining above-trend growth with above-trend inflation, fell from 36% to 29% since last month. Global growth optimism collapsed from a net 39% to a net 7% over the same period, while inflation expectations jumped from net 9% to a net 45%.

The ‘goldilocks’ scenario held steady at 14%, while ‘stagnation’ fell from 5% to 2%.

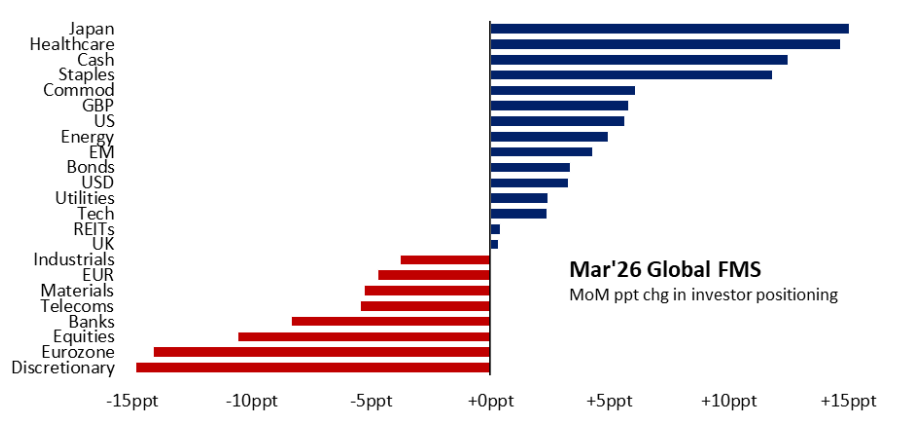

Change in fund managers’ positioning in Mar 2026

Source: BofA Global Fund Manager Survey, Mar 2026

The March allocation data shows some fund managers’ stagflation concerns reflected in portfolios, with consumer staples and commodities being added to this month. Japan recorded the largest month-on-month increase in allocation of any asset class, followed by healthcare and cash.

Consumer discretionary recorded the steepest monthly decline in allocation in the survey, with eurozone equities, overall equities and banks also sustaining significant cuts. Bank of America’s strategists pointed to a shift away from cyclical and growth-sensitive exposures toward defensive positioning.

In absolute terms, investors are most overweight emerging markets, healthcare, equities in general and commodities, while the largest underweights are to bonds, consumer discretionary and the US dollar.

Long gold and long global semiconductors were both cited as the most crowded trade among 35% of respondents. Notably, the share of respondents identifying long Magnificent Seven as the most crowded trade fell to just 9%, down from a peak of 54% in December 2025.

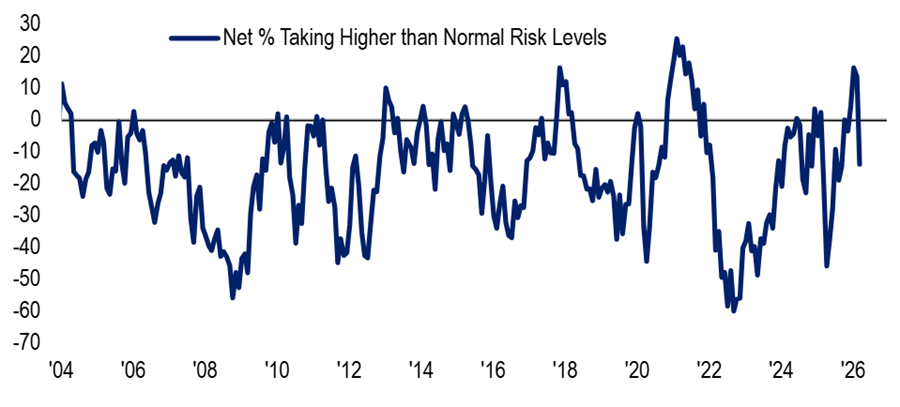

Fund managers’ risk relative to their benchmarks

Source: BofA Global Fund Manager Survey, Mar 2026

The de-risking extends beyond sector rotation into overall risk appetite, with the net percentage of investors taking above-benchmark risk swinging from net +14% to net -14% in a single month.

The absolute reading of net -14% is notable but not historically extreme, with lower risk positioning seen in recent events such as the start of the Covid pandemic, 2022’s inflation surge and 2025’s Liberation Day tariffs.

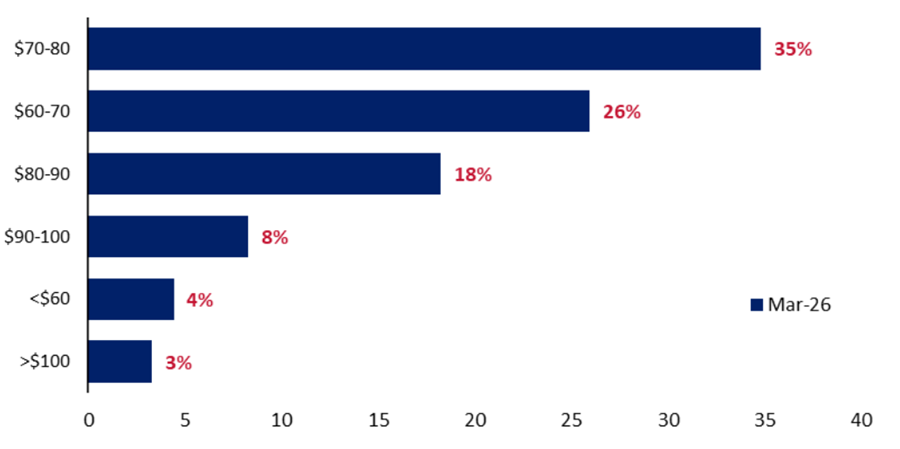

Where fund managers expect oil to end 2026

Source: BofA Global Fund Manager Survey, Mar 2026

With Brent crude oil currently trading above $100 a barrel, the weighted average year-end price expectation among survey respondents is $76/bbl, implying a decline of roughly 25% from current levels.

A combined 61% of respondents expect Brent to trade below $80/bbl by year-end, with 35% clustering in the $70-80 range and a further 26% expecting $60-70. Just 3% expect oil to remain above $100/bbl, reflecting an overwhelming consensus that current elevated prices will not hold.

Bank of America’s strategists use the survey to formulate contrarian trades, which this month include selling oil above $100/bbl, selling the US Dollar index above 100, buying 30-year Treasuries at 5% and buying the S&P 500 at 6,600.

The bank also identified lightly held Magnificent Seven, consumer and China stocks as the assets most likely to outperform in a US-Iran de-escalation rally, against the still-heavily owned emerging markets, Japan, semiconductors, banks and industrials.