No single asset class can be counted on to protect investors during periods of market stress so the only way to get genuine portfolio resilience comes from diversification across asset classes, styles and other investment factors, according to St. James's Place’s Stephen Brierley.

In recent weeks markets have been rocked after the US and Israel launched coordinated airstrikes on Iran, killing supreme leader Ali Khamenei and targeting military, leadership and nuclear infrastructure. Iran retaliated with missile and drone strikes across the region.

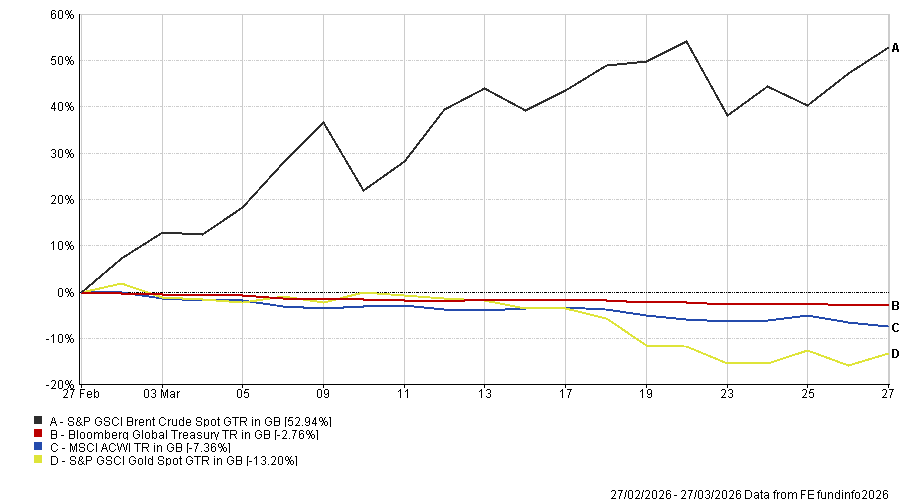

As a result, Brent crude surged from $72 per barrel on the eve of the conflict to over $115, as Iranian attacks reduced traffic through the Strait of Hormuz, through which around 20% of global oil and gas supplies transit. The IEA has described the disruption as the “greatest global energy and food security challenge in history”.

Assets across the board have fallen in the month since the conflict started – including perceived safe havens such as gold, which is down more than 15% in sterling terms.

Performance of assets since 28 Feb

Source: FE Analytics

This has led many investors to question the effectiveness of ‘safe havens’. However, Brierley, investment specialist at St. James’s Place, pointed out that this status is not defined by fixed characteristics but by investor behaviour.

When markets turn volatile, investors shift capital towards asset classes they perceive as less exposed to the prevailing shock. The dollar, gold and government bonds are the most widely cited examples, though which assets earn that status has shifted over time.

“However, the resilience typically associated with traditional safe haven assets within the broader geopolitical climate has been less reliable,” Brierley said.

The Iran conflict has demonstrated this, as investors who expected traditional safe havens to hold firm instead saw very different dynamics play out.

Gold reached an all-time high of $5,586 per ounce on 29 January 2026, but is currently trading at approximately $4,528 even though the Iran conflict represents the most acute geopolitical stress event the region has seen since 2003.

The dollar’s record has been similarly mixed. The greenback has been one of the clearest short-term safe haven winners in the Iran conflict. Although it has strengthened recently, it is some way off its 2025 highs, with Brierley noting it was "weak through the tariff volatility, not providing a safety net”.

The 2022 experience with bonds and equities added a further layer of complexity to the safe haven question. The two asset classes, which have historically shown low correlation, fell simultaneously that year.

“In 2022 we saw both bonds and equities fall because the world was in a very high inflation environment,” Brierley explained. “High inflation tends to cause equities and bonds to be more closely correlated.”

Black swan events compound the problem further. During the Covid lockdowns, for example, sell-offs were broad-based, leaving investors with few places to hide regardless of how their portfolios were positioned.

Given this, SJP’s investment philosophy rejects repositioning into perceived safe havens in times of market shocks.

“A core principle of portfolio construction is the inclusion of uncorrelated asset classes. This diversification helps build resilience, particularly in periods of market volatility,” the investment specialist said.

“While portfolios should be designed to withstand short-term shocks, which are inherently unpredictable, our investment philosophy does not support reactive moves into perceived safe-haven assets during or after such events."

He highlighted the complex picture facing any investors hoping to predict which assets could hold up best in the current market backdrop.

A modest shift in sentiment from emerging markets towards developed markets has provided some short-term support for the dollar, but Brierley cautioned that “whether recent strength can be sustained remains uncertain, with limited evidence to support a clear directional view”.

He also noted that currency movements remain difficult to predict, pointing to 2025 as a case in point: despite broad market weakness during the tariff volatility, the dollar weakened rather than strengthened, undermining its safe-haven credentials.

A further complication is that a wide range of both risk and defensive assets are denominated in US dollars, meaning currency moves feed through in ways that are not always intuitive for investors.

Longer term, Brierley said attractive valuations in emerging markets and developed markets outside the US continue to underpin a positive outlook for those regions, even as sentiment has shifted in the short term.

At a regional level, the US has outperformed its developed-market peers during the initial phase of the recent volatility. Japan and emerging markets have been the most affected, despite strong year-to-date performance coming into the conflict, and remain exposed to further developments.

Smaller companies have shown more resilience than large-caps outside the US and in emerging markets, which Brierley attributed to their more domestic orientation and lower exposure to global trade and energy, though he acknowledged liquidity dynamics may also be a factor.

At the sector level, energy has led performance, with consumer staples, industrials, materials and utilities also showing relative resilience. Financials and consumer discretionary have been the most negatively impacted.

Recent moves have also begun to reverse some of the earlier valuation trends that had favoured non-US markets, with US equities regaining relative strength. If that persists, Brierley suggested, the valuation gaps that closed earlier this year could re-emerge, with the US once again pulling ahead of other regions.

“The only way to truly manage market volatility is to be diversified across asset classes, currencies, styles, sectors and countries over the long term,” he finished.