Value investors hunting in ‘traditional’ value sectors such as oil, miners and financials have enjoyed somewhat of a boom period in recent years but must get more selective from here on out, fund managers have said.

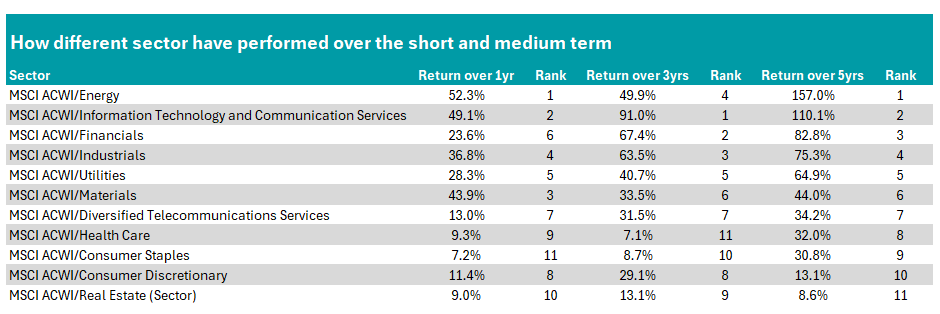

Banks and insurers – overlooked in the post-financial crisis era – roared back to life when central banks around the world ramped up interest rates to combat 2023's inflation that followed the pandemic. Over the past three years, it has been the second-best-performing MSCI AC World sector, as the table below shows.

Meanwhile, a half-decade headlined by uncertainty thanks to Covid, the outbreak of war and the return of president Donald Trump to the White House has caused gold to rocket to new heights, boosting miners producing the yellow metal.

A slowdown in global trade and fears over transportation has boosted metal prices in general as well – not just gold. As such, miners have been the third-best sector over the past 12 months.

Source: FE Analytics

Most recently, the war between the US/Israel and Iran has led to the closure of the Strait of Hormuz, a key waterway for oil transportation. The price of the black stuff has jumped to more than $100 per barrel as a result, boosting the energy titans.

The oil sector is up 33% in the past three months, 52.3% over one year and 157% over five years, making it the best-performing sector across all these timeframes.

Simon Adler, head of value equities at Schroders, said: “It is true that some of the strongest performing segments of the market recently have been banks, energy and materials. And it is also true that these were well represented in value portfolios.”

With such strong returns, investors may wonder if these traditional value areas still represent good value, or whether they are less attractive after their strong gains.

There are still opportunities in traditional value

Miguel Oleaga, portfolio manager at Thornburg Investment Management, said: “The strong performance of traditionally value-oriented sectors over the past year has shifted the opportunity set, but it has not exhausted it.

“The primary change is that markets are no longer rewarding entire sectors. Instead, returns are increasingly driven by individual businesses, where balance sheet strength, cashflow resilience and entry price are paramount.”

He suggested that value investors will need to be more discerning moving forward, highlighting BNP Paribas and Bank of Ireland as examples of stocks where “improved capital positions and resilient earnings” have yet to be rewarded by markets.

Among industrials (another traditional value sector that has performed well in recent years), Techtronic Industries is an example of a stock that has come under short-term pressure that has “obscured long-term competitive advantages”.

“While headline valuation metrics suggest that financials and non-US equities remain relatively attractive, avoiding ‘value traps’ requires a disciplined focus on business quality and a defined pathway to value creation,” Oleaga said.

“Opportunities are becoming increasingly idiosyncratic. Select consumer and service businesses, as well as technology segments where expectations have meaningfully reset, offer the potential to access high-quality companies with compelling long-term return profiles.”

Value moves over time

Adler noted that most sectors “will be a darling in one cycle and a value stock in another”. As such, investors must not assume that stocks are “stuck” in certain buckets forever.

“At its core, value investing is about avoiding overheated areas where stocks are priced for perfection and identifying opportunities where sentiment is depressed and share prices have fallen to irrationally low levels. These pockets of fear and greed are dynamic and they’re constantly evolving,” he said.

“Five years ago, with interest rates perceived to be anchored near zero and oil prices collapsing during Covid lockdowns, banks and energy companies sat firmly in that ‘fear zone’ and were trading at deeply discounted multiples of through-cycle earnings.”

He agreed that there are still pockets where the fund is finding select opportunities in these areas, but noted there are new options in other sectors, such as luxury goods companies.

“[These] have moved from being widely loved to increasingly out of favour as the growth outlook has slowed.”

He highlighted alcoholic beverage companies. Once viewed as dependable quality-compounders, they now face structural concerns around weight-loss drugs increasing the focus on wellbeing and fitness, and shifting consumer preferences as younger people are drinking less than previous generations.

Is tech now value?

Despite a roaring few years as the AI boom has inflated technology stocks, the wheels have come off some areas, such as software companies.

Investors have been quick to assume software will be obsolete in the era of AI, but Brendan Gulston, co-manager of the WS Gresham House UK Multi Cap Income fund, said the “disconnect between perceived and actual disruption risk has created a compelling opportunity”.

Focusing on the UK, he said the software sector, is home to companies with “structurally resilient business models”, adding that many “operate within frameworks that constrain AI-led disruption”.

“Businesses with deep domain expertise, proprietary data, system-of-record positions and trusted ecosystem relationships enjoy structural advantages that are difficult for new entrants or general-purpose AI to replicate,” he said.

“Against the backdrop of an already undervalued UK market, UK software stocks are now trading at even more attractive valuations.”

Not all agreed, however, with Adler noting that, despite the well-publicised sell off, “none of these [software] companies currently meets our screening criteria”.

“When it comes to Big Tech and software, there may well be a day when they are on our valuations screens. But today they are nowhere near.”