When investors think about financial stocks, they may often default to thinking only about banks – and although they have been performing well in recent months, several insurers, platforms, asset managers and exchanges have also had resilient earnings and idiosyncratic growth, despite the uncertain interest-rate backdrop.

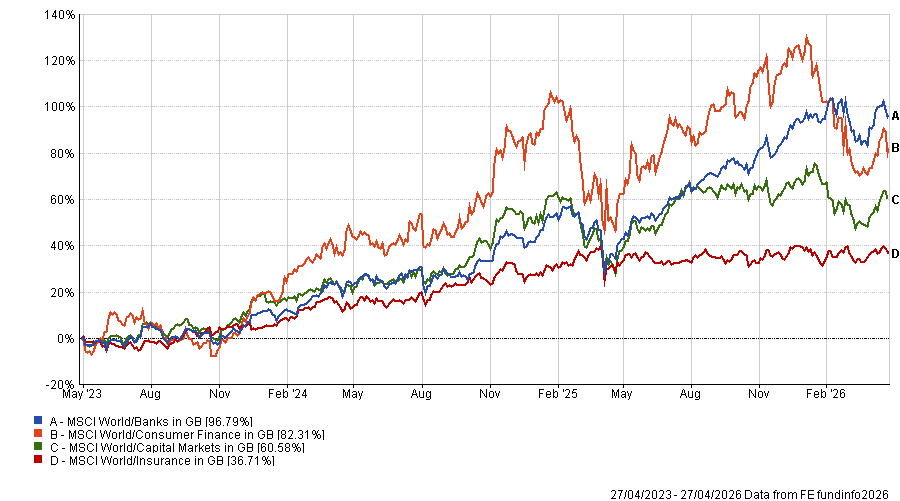

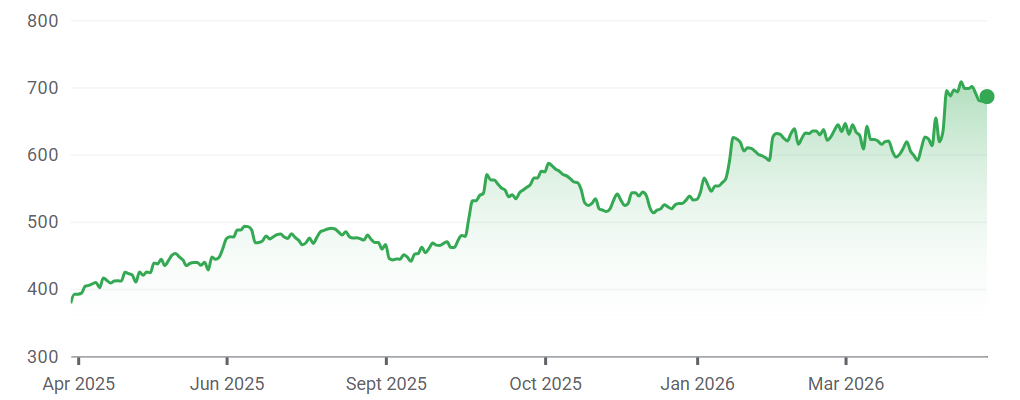

Performance of core financials subsectors over 3yrs

Source: FE Analytics

To avert the risk of leaving these behind, Trustnet asked fund managers which non-bank financials they believe offer the most compelling opportunities.

Brooks Macdonald

Ken Wotton, manager of Strategic Equity Capital, pointed to UK wealth manager Brooks Macdonald, a “strong value opportunity” in a “burgeoning market” underpinned by structural growth drivers, including rising household wealth, a persistent advice gap and supportive government policies.

“The firm’s recent transformation and investment initiatives have proven successful, with the company returning to net asset growth and delivering two successive quarters of positive net flows,” Wotton said.

Earlier this month, Brooks Macdonald reported second-quarter net inflows of £58m but total funds under management and advice dipped to £19.9bn after £301m of adverse market movements in the third quarter of the 2026 financial year.

“If sustained, this will demonstrate that management’s optimisation efforts are paying off and could act as a catalyst for a substantial re-rating,” Wotton noted.

Stock price performance over 1yr

Source: Google Finance

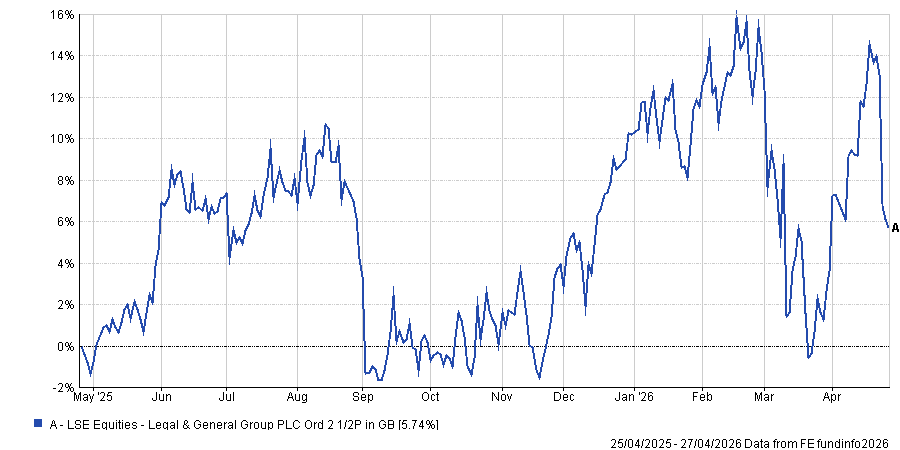

Legal & General

Alan Dobbie, co-manager of Rathbone Income, said Legal & General is a “well-constructed” business, offering services across retirement, insurance and asset management.

“While its complexity means it is not always fully appreciated by the market, it remains a key holding in Rathbone Income,” Dobbie said.

He noted that the long-term backdrop is supportive of the business, as an ageing population means pensions and retirement solutions matter more. In addition, “with interest rates no longer pinned to the floor, companies are increasingly looking for ways to de-risk their defined benefit pension schemes”.

“The final step in that journey often involves transferring the scheme to one of a small number of insurers,” he said.

Meanwhile, the asset management business is benefiting from “a mix shift away from its well-known index-tracking strategies towards higher-margin solutions”.

Dobbie argued that the market is underestimating how cash-generative L&G can be, noting it offers a dividend yield of over 8%, growing steadily at 2%, and has a “clear willingness” to return cash through share buybacks.

“That combination of attractive income and disciplined capital return is relatively rare outside the banking sector,” he said.

Stock price performance over 1yr

Source: FE Analytics

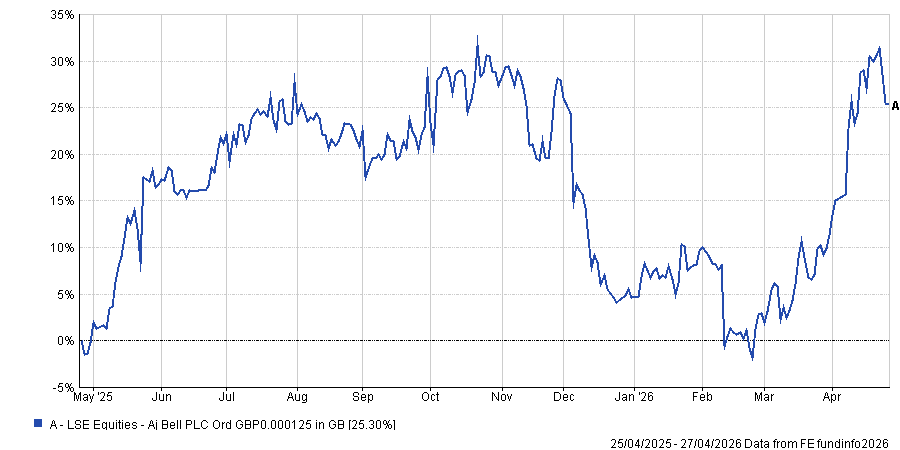

AJ Bell

Eric Burns, lead manager of TM SDL UK Buffettology General, picked UK platform AJ Bell.

As well as an “excellent reputation” and high customer satisfaction, the business has a financial model that “exhibits many of the characteristics we look for”, Burns said.

He said it has strong underlying revenue growth of around 20% per annum without reliance on acquisitions, a high return on equity of 50% and it converts most of its earnings into free cash.

“As a result, it has a cast iron balance sheet which is used from time to time to buy back its own shares, further enhancing shareholder returns,” Burns noted.

AJ Bell also recently published its second quarter trading update, where it reported growing its customer base by 7% in the three-month period and higher assets under management (AUM) in the face of heightened market volatility.

Since its initial public offering (IPO) in 2018, the platform’s earnings per share have grown at an annualised compound rate of 23%.

Stock price performance over 1yr

Source: FE Analytics

Polar Capital

Polar Capital is an AIM-listed active fund manager with £30.6bn in AUM across 13 specialist investment teams running thematic and sector-focused strategies across technology, healthcare, insurance, emerging markets and financials.

Simon Moon, fund manager at Unicorn Asset Management, said: “What draws us to it is the combination of a genuinely differentiated product offering, a strong balance sheet with £120m of net cash and a dividend yield of around 7% that reflects the high cash conversion of the fee revenue model.”

Its fund flows have also been strong, with inflows of £1.4bn in the first quarter of this year.

Moon added that Polar Capital’s specialist positioning gives it pricing protection in an asset-management market where generic active strategies are losing ground to passives.

“At around seven times enterprise value/earnings before interest and tax, the company’s current valuation ascribes very little to continued AUM growth or any pick-up in performance fee activity,” he said.

Stock price performance over 1yr

Source: Google Finance

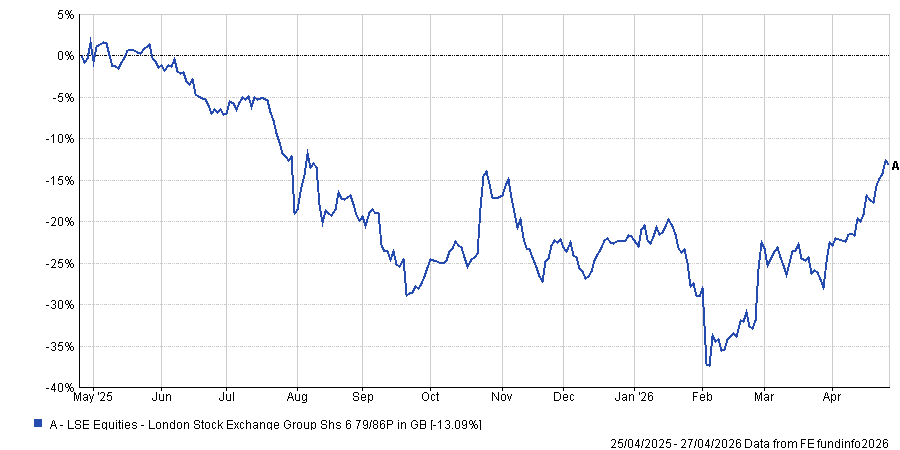

London Stock Exchange Group

London Stock Exchange Group (LSEG) is a holding of Finsbury Growth & Income Trust, highlighted by deputy manager Madeline Wright.

“Like so many other data companies, LSEG has recently been caught up in fears over AI disruption and both the share price and valuation are materially lower now than they were a year ago,” Wright said.

“If anything, the progress that the business has made over that period of time has made us more bullish on LSEG’s prospects and we therefore view recent weakness as a potential opportunity for long-term investors.”

Whilst the London Stock Exchange itself remains an important part of LSEG’s business, it now only represents around 4% of the group’s global revenues. A combination of organic growth and key acquisitions has allowed LSEG to evolve into a global provider of real-time financial data, Wright said.

“Its core strength lies in the recurring revenues it generates from financial data, analytics, and post-trade services, which embed it deeply into clients’ workflows.”

In the longer term, Wright argued that LSEG is likely to be an AI beneficiary rather than victim.

Stock price performance over 1yr

Source: FE Analytics

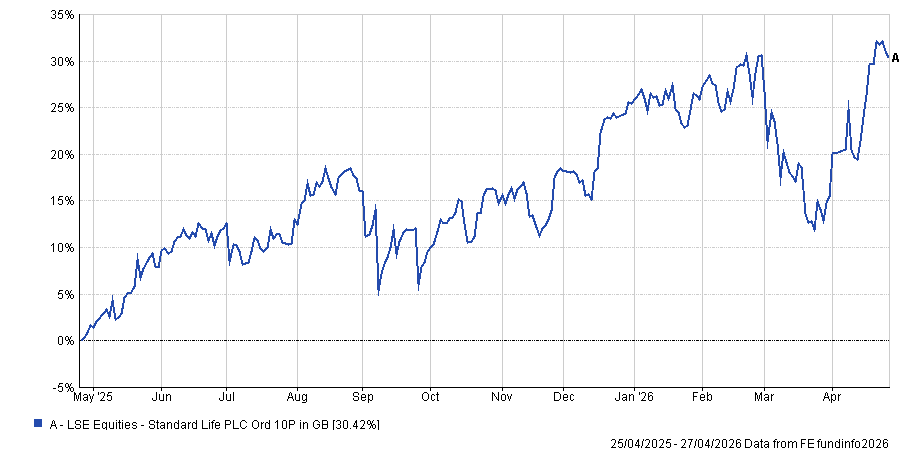

Standard Life

Life assurance, pensions and long-term savings company Standard Life is the pick of David Moss, senior portfolio manager at Columbia Threadneedle Investments.

Moss pointed to Standard Life’s recently announced acquisition of Aegon’s UK business. “They paid a sensible price and the deal comes with £800m of net synergies and transforms the business,” he said.

Prior to the deal, Standard Life made most of its profits from running off legacy books of closed businesses that had been purchased over the years, a business model that Moss said was very steady and cashflow-generative but was capital-intensive and would decline over time.

“Following the Aegon purchase, Standard Life will be made up of 57% capital light open businesses. It will also move from number six to number two in the workplace pensions market, while also becoming the UK’s largest long-term savings business,” Moss said.

The company has a dividend yield of over 7% that has been growing every year.

Stock price performance over 1yr

Source: FE Analytics

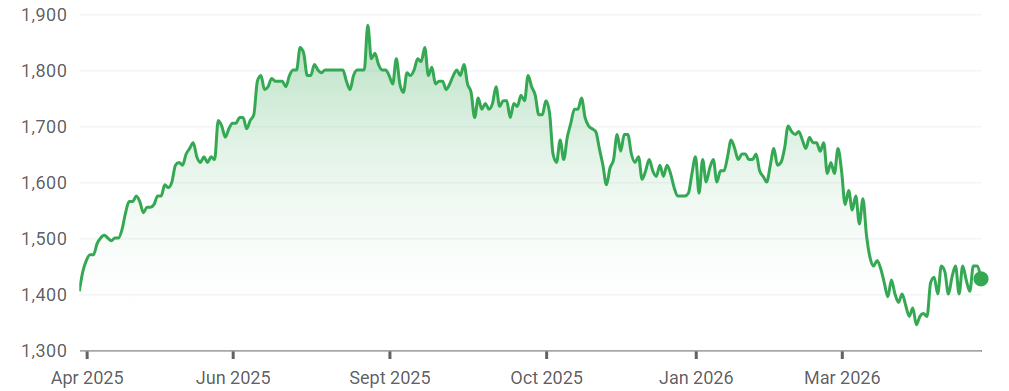

AIA Group

Looking further afield, Stuart Rhodes, manager of M&G Global Dividend, picked AIA Group – a Hong Kong-listed insurer.

With a broad Asia footprint, the company is “well-placed for the long-term growth and increasing wealth across the Asia region”.

Rhodes said: “Asia presents a compelling opportunity for life and health insurance and long-term savings, which was reflected in AIA’s record results for 2025.”

AIA reported that the value of new business increased by 15% to $5.5bn, operating profit after tax rose 7% to $7.1bn and embedded value increased by 8% to $79.7bn – driven by strong agency performance, a shift towards protection and capital-light products and robust demand across Asia.

“The company has a strong balance sheet to support growth across the economic cycle and remains disciplined in its approach to capital management,” Rhodes said.

Stock price performance over 1yr

Source: Google Finance

Deutsche Börse

Paul Middleton, senior global equities portfolio manager at Mirabaud Asset Management, pointed to German multi-tiered exchange and financial services company Deutsche Börse.

“When markets are unpredictable, businesses and investors have a much greater need to protect themselves against sudden moves in oil prices, interest rates and currencies – that translates directly into higher trading activity and rising revenues for the platforms at the centre of global markets,” Middleton said.

Alongside Deutsche Börse’s core trading business, its Clearstream division holds client cash and earns interest on it, meaning it benefits from interest rates staying higher for longer.

“In the first quarter of 2026, volumes are already running double-digits ahead of last year and the pending Allfunds acquisition offers a further leg of upside – doubling the size of its fund services business and delivering around EPS accretion from cost synergies,” Middleton added, noting that he does not think this has been fully priced in “given concerns on antitrust risk that we view as manageable”.

Stock price performance over 1yr

Source: Google Finance