Passive funds in the US, European and Japanese equity sectors have proved most consistent at staying out of the bottom quartile, Trustnet research has found, with few active funds being able to match them.

In this series, Trustnet ran the quartile rankings of every fund in the Investment Association universe for each quarter of the past decade then looked for those that avoided the fourth quartile in every one of them.

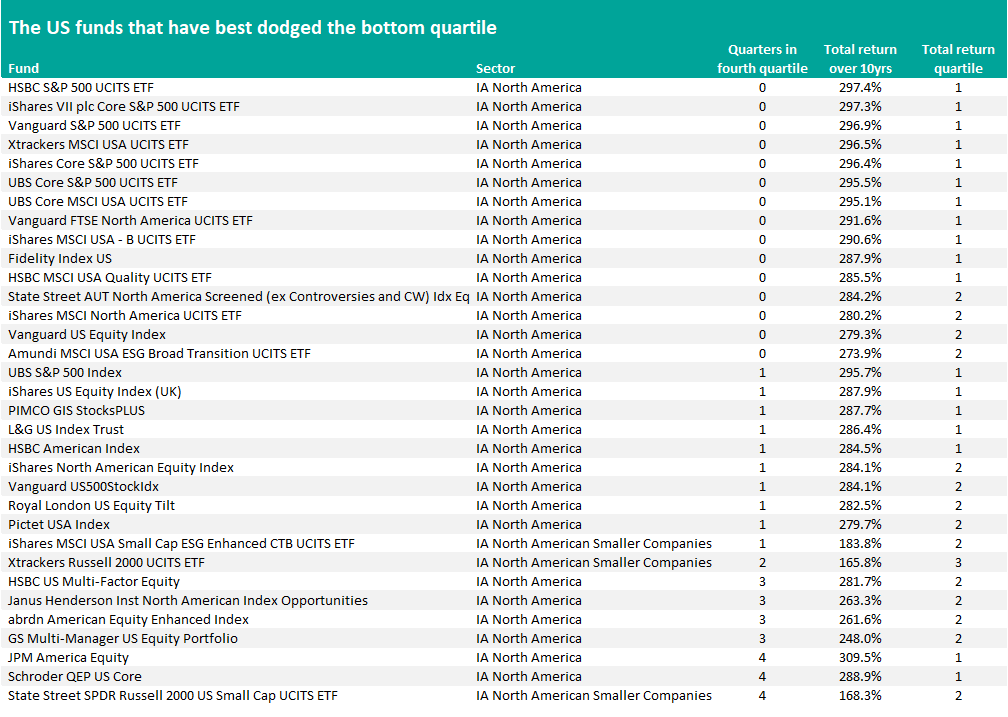

The table below shows the IA North America and IA North American Smaller Companies funds that spent four or fewer quarters at the bottom of their sector.

Source: Finxl. All funds have a minimum track record of 10 years. Total return in sterling between 1 Apr 2016 and 31 Mar 2026

Some 15 funds have a perfect track record of dodging the fourth quartile over the past 10 years. All of these reside in the IA North America sector and invest passively.

Those tracking the S&P 500 have made the highest returns over the past decade, reflecting the fact that US mega-cap stocks – especially in the tech space – have consistently led the global market.

Active funds, on the other hand, have historically found it difficult to outperform in the US, owing to it being the most heavily analysed market in the world and leaving little exploitable mispricing for active managers to capitalise on. In addition, the strong concentration of the past decade has held back active managers who failed to match the benchmark weightings to the winning stocks.

We have to go down 18 places to find a fund that is not a pure index tracker: PIMCO GIS StocksPLUS, which has only been in the bottom quartile in one quarter. This fund tracks the S&P 500 but uses an actively managed portfolio of short-duration bonds to generate alpha.

Royal London US Equity Tilt, HSBC US Multi-Factor Equity and abrdn American Equity Enhanced Index are examples of funds that largely mirror the market but make small active bets away from it in the pursuit of higher returns or, in the case of Royal London’s Tilt range, an improved ESG profile.

On HSBC US Multi-Factor Equity, analysts at Square Mile Investment Consulting and Research said: “Broadly speaking we would expect this fund to outperform the S&P 500 index during periods of market growth as well as when markets are being driven by fundamentals. While it may well underperform during market inflection points, a natural weakness for more quantitatively driven strategies, overall we believe that investors will be well served over a full market cycle.”

GS Multi-Manager US Equity Portfolio and JPM America Equity are the only active funds to appear in the above table, thanks to just three and four quarters in the bottom quartile respectively.

The Goldman Sachs portfolio is split between multiple investment managers who are unaffiliated with Goldman Sachs Asset Management, although the exact managers are not readily available on the fund’s factsheet or webpage.

JPM America Equity is built around a concentrated portfolio of the managers’ best ideas across the growth and value styles, which is intended “to provide investors with access to complementary investment styles and potentially smoother long-term returns”.

Source: Finxl. All funds have a minimum track record of 10 years. Total return in sterling between 1 Apr 2016 and 31 Mar 2026

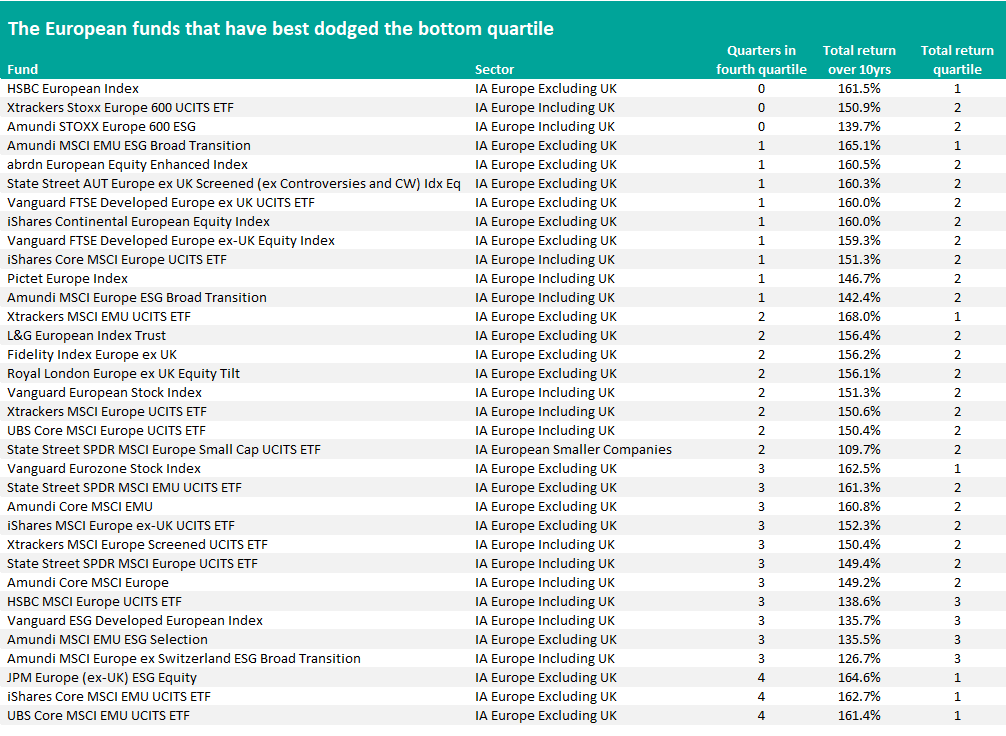

European equities are often seen as being a much richer hunting ground for active managers, as the market is less covered by analysts than the US and tends to have more attractive starting valuations.

However, FE fundinfo data shows that passive funds have the best track record in avoiding their peer group’s fourth quartile in this part of the market as well. As the table above shows, the vast majority of funds making the shortlist in this research track an index.

Of the 34 funds that have only been in the bottom quartile for four or fewer periods, just two – abrdn European Equity Enhanced Index and Royal London Europe ex UK Equity Tilt – do not take a pure passive approach.

But as we saw with the US sectors, even these funds are not fully active as they largely mirror the benchmark but will take underweight and overweight stock positions in order to maximise returns or their ESG profile.

Source: Finxl. All funds have a minimum track record of 10 years. Total return in sterling between 1 Apr 2016 and 31 Mar 2026

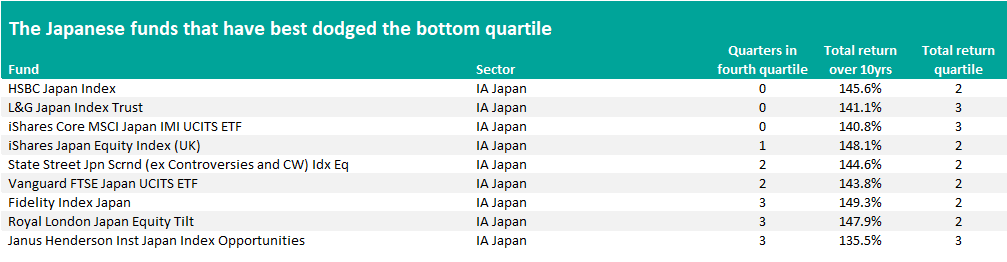

In the IA Japan sector, the same trend can be seen with only nine funds making the cut and all of these being pure index trackers. The exception is Royal London Japan Equity Tilt, which is in the same range as two funds already mentioned in this article.