Markets are pricing in both accelerating AI optimism and a potentially serious energy shock, according to investment strategists, creating a growing disconnect between buoyant stocks and an increasingly fragile economic backdrop.

Sahil Mahtani, a director at Ninety One’s investment institute, thinks financial markets are caught between two very different potential outcomes but investors may not be taking the worse one seriously enough.

The strategist said the investment case looked reasonably clear at the start of 2026, with a falling inflation and rising growth macro environment supported by the stability that followed the October summit between US and Chinese leaders Donald Trump and Xi Jinping, and durable capital expenditure themes including AI and rearmament.

However, the picture has since become considerably more complicated, following the attack on Iran by the US/Israel and the resultant closure of the Strait of Hormuz.

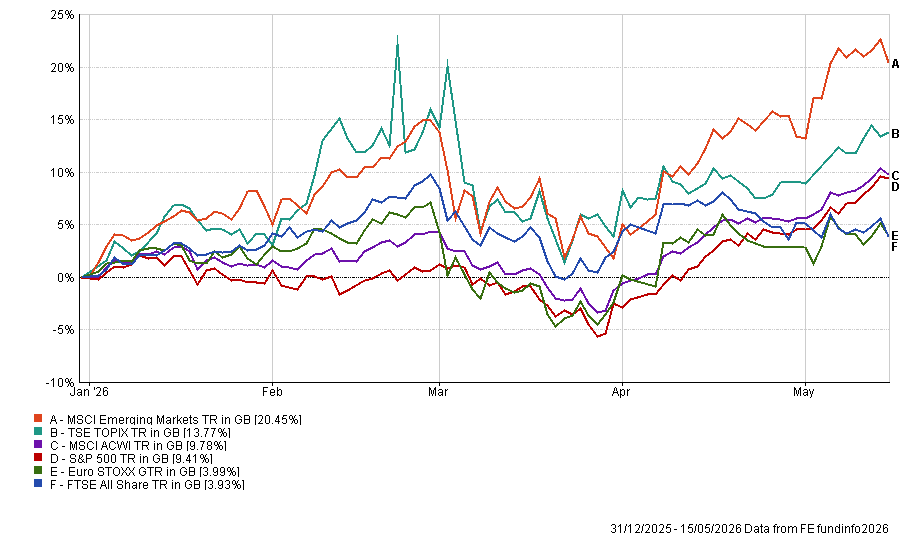

Performance of stock indices in 2026 to date

Source: FE Analytics. Total return in sterling between 1 Jan and 18 May 2026

“Markets are simultaneously pricing accelerating AI optimism and a potentially serious energy shock,” Mahtani said. “Putting all this together, we could be heading for a very good environment for risk assets or an utterly terrible one.”

Patrick Farrell, group chief investment officer at Charles Stanley, agreed that markets have shown a remarkable ability to look past bad news recently.

“Recent equity rallies suggest investors are willing to latch onto any positive signal, even as the reality on the ground remains stubbornly uncertain,” he said.

“That willingness to believe is understandable, but it risks glossing over a more uncomfortable truth. The world is entering a period where geopolitical volatility, higher inflation and tighter financial conditions are not temporary disruptions, but structural features.”

Mahtani identified two distinct technological leaps over the past 12 months that have reset expectations for AI’s economic impact and provided some grounding for the market’s optimism.

The first was the emergence of AI reasoning models including o3/o4-mini and Claude Opus 4.5 in 2025, which triggered a broader shift toward inference time compute scaling (where models are given extra computing resources at the moment of use to think through problems more carefully, improving performance with each query).

The second came in early 2026 with the arrival of agentic AI, a development markets quickly recognised as a demand multiplier across the entire AI supply chain, from graphics processing units to data centres. Nvidia H100 GPU spot prices rose roughly 70% in the on-demand market from April onwards and S&P 500 earnings expectations for 2026 have risen sharply since March, though the gains are concentrated in a small number of AI beneficiaries.

“The bullish case for AI is that demand for compute continues to arrive along with positive unit economics,” Mahtani said. “The inflection since March is why markets have become increasingly optimistic about the sustainability of AI spending.”

However, he argued it is too early to conclude that AI token prices will rise sustainably enough to improve unit economics, as some Goldman Sachs researchers have suggested. Previous technological revolutions have typically seen falling unit prices as they mature and AI is unlikely to be different, creating a headwind for the long-term investment case.

Farrell added the market is pricing an unusually strong earnings outlook, especially in the tech space, at a time when uncertainty spans geopolitics, supply chains, inflation and monetary policy, all of which have significant implications for sectors well beyond the AI cluster.

“The key question for investors is not whether uncertainty exists – it clearly does – but whether current valuations adequately reflect it,” he said.

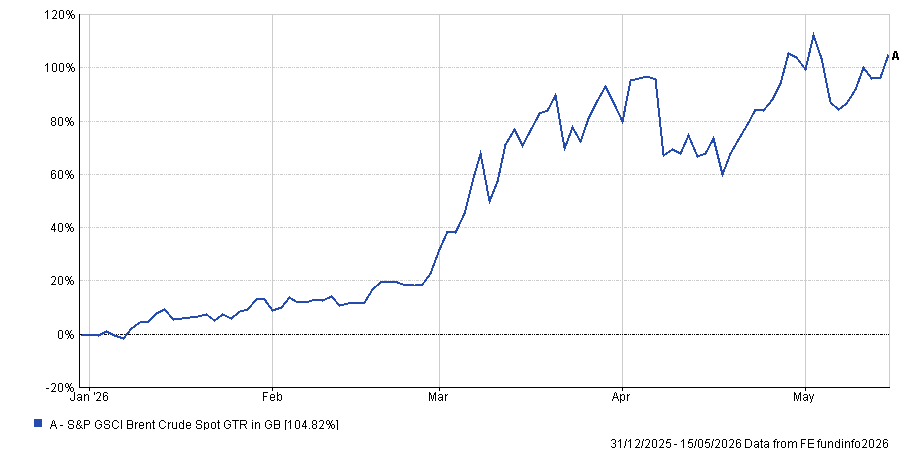

A lot of this uncertainty revolves around the rising oil price. Around one-fifth of the world’s oil passes through the Strait of Hormuz but it has been effectively closed for almost three months.

Performance of oil prices in 2026 to date

Source: FE Analytics. Total return in sterling between 1 Jan and 18 May 2026

Global oil inventories have fallen from under 8.4bn barrels to below 7.9bn barrels, according to Ninety One, approaching system maintenance levels of around 7.6bn barrels. Analysts say further depletion could begin to affect the global economy in ways that markets have not priced.

“Markets appear to be treating the Hormuz disruption as temporary rather than systemic,” Mahtani said. “But even if the Strait of Hormuz reopens, supply chains, inventories and refinery activity may take much longer to normalise.”

Raphael Olszyna-Marzys, international economist at J. Safra Sarasin Sustainable Asset Management, said roughly 10 to 13% of pre-war oil supply is still not reaching global markets and energy stockpiles cannot indefinitely cover that gap.

“Something will have to give,” he said. “In the near term, the danger is that oil prices surge as inventories are drawn down to critical levels.”

Olszyna-Marzys still expects oil to settle at $80-90 per barrel by the end of 2026, on the basis that pressure on both Iran and the US eventually forces a reopening of the strait, but now expects prices to stay higher for longer before easing, a shift that has pushed the firm’s inflation forecasts up by 0.1 to 0.2 percentage points.

But even a resolution to the Hormuz crisis does not clean up the problem neatly.

Mahtani noted that a meaningful normalisation of tanker positioning and refinery restarts may not come until late 2026. The lagged effects of product shortages, inventory depletion and demand destruction could produce a real squeeze on activity even after the strait reopens.

Farrell said energy prices “act as a tax on the economy”, feeding into consumer spending, corporate margins and growth expectations regardless of where the underlying conflict is located. “Optimism that ignores those mechanisms could be built on shaky ground,” he warned.

The US consumer is more exposed than headline equity indices suggest. Conference Board consumer confidence sits well below its long-run average since 1967 and the S&P 500 equal-weight index remains below its late-February peak, with companies with direct exposure to the bulk of US consumer spending, such as Whirlpool and Shake Shack, underperforming.

Mahtani noted that US households are currently being supported by $47bn in tax refunds and $63bn in tax relief, which together have so far offset a $25bn hit from higher petrol prices. That support could run until September.

The Federal Reserve faces an uncomfortable backdrop: Olszyna-Marzys raised his 2026 US inflation forecast to 3.7% and noted that three regional Fed presidents dissented at the 29 April FOMC meeting.

A prolonged Hormuz closure could tilt the policy bias toward tightening. His central forecast is for no rate cut this year and just one in 2027, with risks skewed toward a higher terminal rate.

For Farrell, the cost of money is the real pressure point as much of the bull-market case over the past decade rested on cheap, abundant capital. As rates settle at higher levels, highly leveraged businesses and long-duration growth themes face greater scrutiny.

“The risk is less about sudden collapse than a gradual reassessment of valuations that once looked unassailable,” he said.

Farrell suggested investors build portfolios for resilience rather than attempting to trade every twist. The case for diversified portfolios built around core asset classes still holds, he said, but those portfolios need reinforcement.

“The goal is balance, not bold bets,” he said.

Bonds and gold have behaved less predictably under inflation scenarios, diluting their traditional protective role. Direct commodity exposure, rather than equity proxies, offers a more practical hedge against short-term energy shocks. Absolute return strategies are also worth consideration.

Mahtani finished: “Our baseline remains that equities can do well in a reflationary environment, especially if AI spending continues to seem sustainable.

“But that view now carries more fragility than it did at the start of the year. The market’s leadership is narrow, the consumer economy is softer than the headline indices suggest and the energy shock has not yet fully passed through the system. It seems unlikely that the impact of this oil shock will be so limited for equity markets.”