For the past decade and a half, Japan has quietly run one of the best equity markets in the world and most investors missed it, according to Theo Wyld, manager of the CC Japan Income and Growth trust.

"It may surprise you to know that over the past 15 years the Japanese stock market has almost kept up with the US," he said. "Europe and the UK pale in comparison in terms of total returns."

Conceptions of the Japanese market as riddled with deflation and stagnation are outdated and, since the global financial crisis, returns have been steady and largely underappreciated. Detractors might also say the market has rerated, that it is expensive now and the easy money has been made. For Wyld, this is both wrong and too pessimistic.

In 2011, the Japanese market traded at below 14x earnings; at the launch of the CC Japan Income and Growth trust in December 2015, around 15x; today, just over 17x. A modest rerate over 15 years, and Japan still trades at a discount to global peers.

"Japanese companies have grown their earnings at a higher compound rate for the past 15 years than the US," Wyld said. "That is despite many reasons I hear for not investing in Japan, including low GDP growth, deflation, negative interest rates and a weak yen. All of this has been going on at a time when corporates have been able to deliver excellent compound growth."

The question, Wyld said, is what happens when those headwinds turn into tailwinds, as they now are.

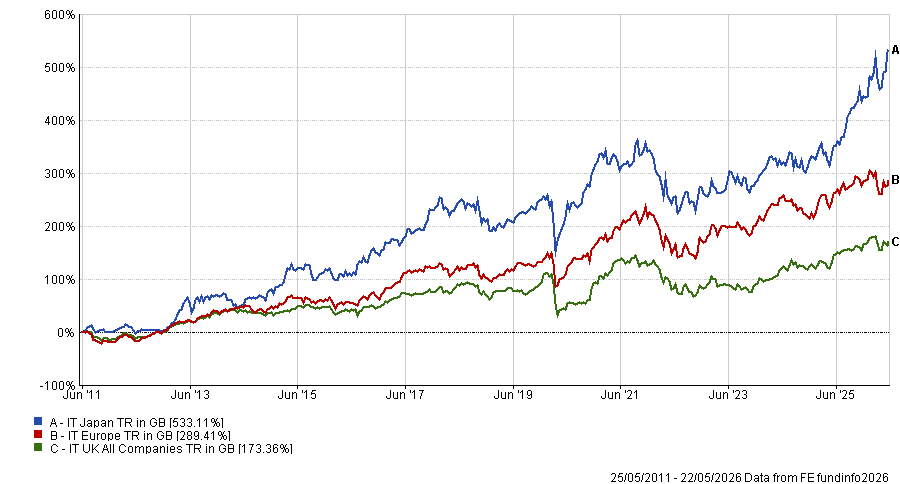

Performance of sectors over 15yrs

Source: FE Analytics

The tailwinds

The first is balance sheets. More listed Japanese companies hold net cash today than in 2012, despite a decade of rising dividends and buybacks. A revision to Japan's corporate governance code due this summer will specifically target companies holding excess cash.

"If you pretended corporate Japan was a company, it would be trading on net cash relative to the US, the UK, and Europe, which would be considerably indebted," Wyld said.

The second tailwind is improving return on equity. At the trust's launch, the market figure was around 3%. It is now around 9%, and Wyld argued corporate ambition will push it further. Return on equity has finally become a benchmark Japanese companies want to be measured against.

Margins are also increasing. Gross, operating and net profit margins across the Topix sit well below equivalent figures for US, UK and European companies. Operational inefficiencies have kept them down, Wyld said, and there is room to close the gap.

There is also a demand-side story that gets little attention. After two decades of deflation, the way Japanese households think about money is changing.

"For so long you could put your money under the mattress and it didn't matter," Wyld said. "Now it does matter."

An estimated 1,000trn yen sits in Japanese bank accounts. The domestic investor has been a net seller of Japanese equities for years. As they start buying, this would mark "a change in fortune for Japan".

The final tailwind is inflation itself, which is sorting companies in a way deflation never did. For two decades, businesses with no pricing power, no earnings growth and no competitive edge – what Wyld called "zombie companies" – could survive because wages never rose and capital was effectively free.

That is now over. Four consecutive years of 4%-plus annual wage growth, combined with one of the tightest labour markets in the developed world, is pushing up costs across the board. Companies that cannot pass those costs on will not hold onto staff.

The portfolio

The CC Japan Income and Growth trust targets the opposite of zombie companies: financially sound businesses that are growing and generating more cash than they need, with enough surplus to return to shareholders.

It holds a maximum of 40 stocks and turns over around 25% of the portfolio each year. Around 35% sits in small and mid-cap stocks, where sell-side coverage is thin and, Wyld argued, the work of finding good businesses is still rewarded.

One recent addition is Keyence, the optical sensors company with gross margins above 80% and operating margins at 55%. It had long been too expensive by the trust's standards, but Wyld bought it in January for the first time in a decade, after a reverse discounted cashflow calculation implied a terminal free cashflow growth rate of 3.5%, down from the 7-8% that had previously kept it out of the portfolio.

The portfolio, Wyld pointed out, has outperformed in growth-led markets and again in the value rally of the past three years without changing what it owns or how it owns it.

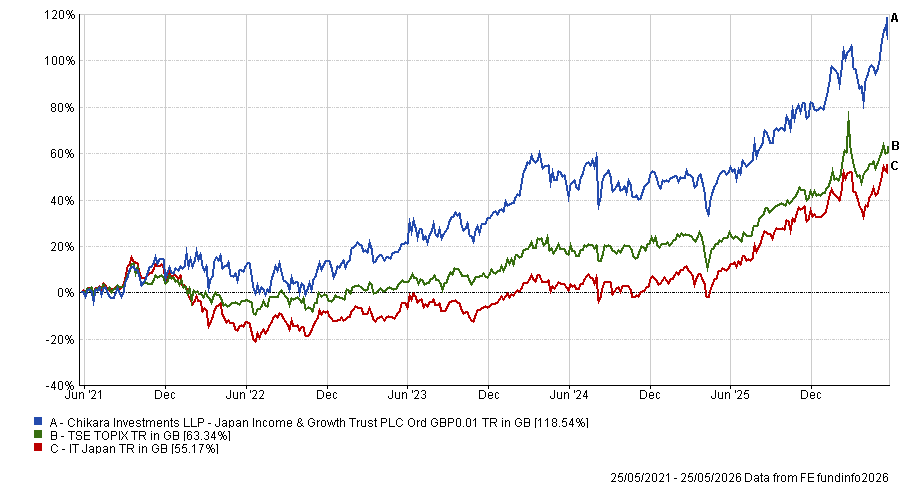

Performance of fund against index and sector over 1yr

Source: FE Analytics

"We don't want to be playing styles," he said, "so we haven't changed what we've been doing over this entire period."