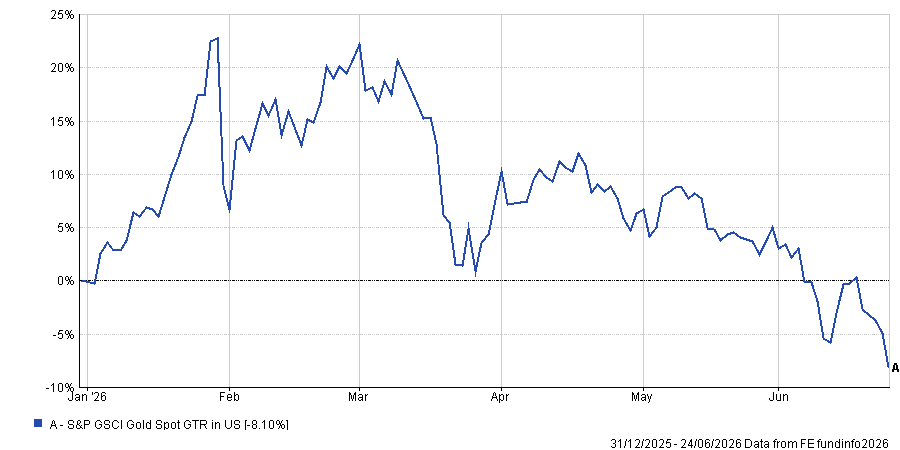

Gold is down 8.1% so far this year and more than a quarter from its peak in January but experts are split on if now is the time to buy.

The yellow metal has struggled in 2026, dropping to its current level of just over $4,000, some $1,600 below its peak in the first month of the year.

Benoît Harger, manager of the JSS Commodity Transition Enhanced fund, said this drop can be partly explained by the prospect of policy rate hikes due to inflationary risk, which boosts the appeal of alternative investments.

Performance of gold spot YTD

Source: FE Analytics

Francesco Sandrini, chief investment officer for Italy and global head of multi-asset at Amundi, said he would be a buyer at these levels.

“Gold has been an excellent diversifier and it will be a good diversifier in a stagflation scenario. So in my opinion, now is an opportunity to re-enter a little on gold,” he said.

What has been playing against gold in the past couple of months has been the readjustment of the US interest rate curve. The recent appointment of Kevin Warsh as Federal Reserve chair was one at odds with what many expected from US president Donald Trump.

Warsh is known to be more hawkish, yet Trump has been vocal in his desire for rates to come down. At his first FOMC meeting as chair, Warsh said he was committed to dealing with inflation, which markets took to mean he was more in favour of rate hikes than cuts.

Harger argued that the Fed is in a difficult spot. “US consumer dynamics remain fragile. Households and businesses cannot sustain a permanent increase in inflation, making higher financing costs highly recessionary. Furthermore, growth is under pressure while governments fail to reduce public deficits,” he said.

The expectation that Trump would not install a Fed chair likely to raise rates has kept US yields anchored. That is until recently, with the market pricing in one hike between now and the end of the year.

This is historically negative for gold, as it does not have an intrinsic yield. When people can get higher rates from holding cash, this option becomes more appealing.

However, Harger noted that, with the US deficit at 120% of GDP and projected to hit 140% by 2040, this puts a limit on any long-term interest rate hikes.

“Since gold is comparable to a long-duration bond, it will benefit from subsequent rate cuts,” he said.

Sandrini said he is still “trying to accumulate at this level”, with allocations of between 1% and 3%. After a rapid rise over the past few years, he said gold’s price is entrenched because elevated real rates and the high debt levels around the world make it “simply difficult to imagine” that the metal will fall too far.

“I think a debasement is something very difficult to unwind given the circumstances,” he said.

Not all agreed, however. Adam Rozencwajg, co-founder and portfolio manager at Goehring & Rozencwajg, said investors “stand at the beginning of what is likely to be a frustrating period for gold prices”.

“The central question is not whether a pullback in gold will occur, but how deep and prolonged it becomes, which will depend overwhelmingly on central bank behaviour.”

That is not to say the manager is anti-gold. Far from it. He argued that there is a “structural bull market” that could continue for many reasons.

For one, highly leveraged Western economies must confront mounting debt burdens, with “the risk of sovereign and quasi-sovereign defaults is likely to grow”, he said.

“In that environment, gold could increasingly be viewed as a ‘must-own’ asset class – one of the few financial assets that represents no one else’s liability.”

Central banks own around 27% of global gold reserves. A June 2026 World Gold Council survey showed that 45% of 76 central banks intend to increase their gold allocation this year, citing low real interest rates and geopolitical tensions.

In the short term, if central banks and other institutions keep buying the yellow metal – something that has helped to propel the price higher in recent years – then the declines seen so far should prove to be manageable.

However, he said that the asset “appears less compelling relative to other asset classes” and although there will likely be “extraordinary buying opportunities in gold and related equities” in the coming years, this has not yet arrived.

“Investors should consider reducing exposure to gold and related equities in favour of energy-related investments, especially those possessing strong earnings leverage to higher oil prices, which are likely to outperform,” he said.

For Harger, the price is less relevant than the use case for gold. “It is an insurance asset. A strategic allocation to it provides protection against sovereign risk and currency devaluation in the face of loose monetary policies and rising sovereign debt,” he said.