Attempting to time the rotation between value and growth investing is close to impossible, according to Charles Stanley Direct's Rob Morgan, so portfolios need exposure to both factors to be balanced.

Markets do not favour one investing style forever and leadership between the two styles can rotate unpredictably. Since the start of 2006, the MSCI AC Growth index has made an 815.6% total return (in sterling), compared with 399.2% from the MSCI AC Value.

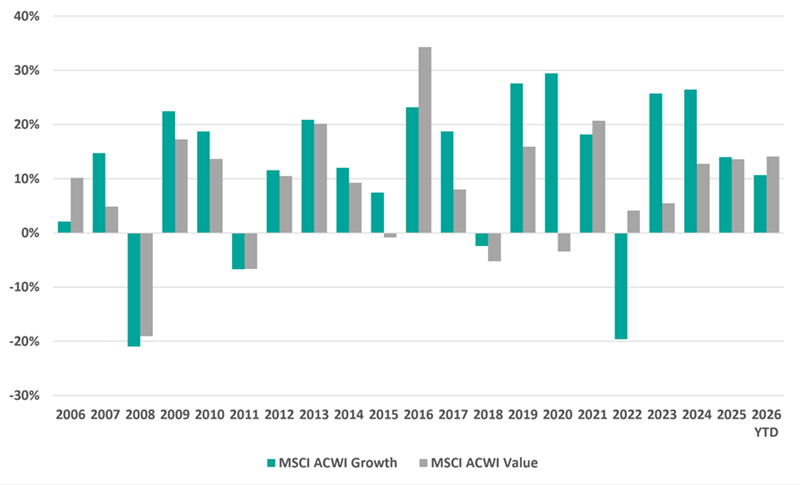

However, growth has not beaten value in every year. FE Analytics shows the growth index has outperformed its value counterpart in 14 full calendar years over this period, while value has won in six years and is ahead over 2026 to date.

Performance of value and growth indices by calendar year

Source: FE Analytics. Total return in sterling between 1 Jan 2006 and 3 Jul 2026.

Morgan, chief analyst at Charles Stanley Direct, said: "Sometimes growth will outperform value, sometimes it's the other way round. Often it depends on the economic situation or it is simply prevailing investor sentiment."

This creates a behavioural trap for investors if they are drawn to whatever has performed well recently. Crowding into a popular style or theme can leave them exposed when sentiment shifts and past performance fails to repeat itself.

Morgan described value investors as people who are "naturally contrarian, wish to avoid fashionable areas and instead target widely ignored parts of the market in search of unappreciated bargains".

Value investors look for a discount between a company's share price and what they judge its true worth to be. Some also seek a margin of safety, where the business's intrinsic value sits close to, or above, the value implied by its share price.

Growth investing works from a different starting point. Growth investors target companies they expect to deliver above-average earnings growth and they typically pay less attention to current valuation measures such as the price-to-earnings ratio.

This approach rests on a bet about the future. Growth investors accept paying more today because they expect a steep rise in earnings to justify that price over the long term.

Both styles carry risks that sit on opposite sides of the same coin. A value investor can fall into a 'value trap', buying a company that looks cheap but is actually declining, with no real prospect of recovery.

Because growth shares already carry high expectations, growth investors face a different danger: even a small earnings miss or short-term setback can hit their share prices hard.

Value investing has struggled in relative terms for most of the past decade, as shown above. Growth stocks, led by technology and e-commerce companies, have delivered outsized returns over that period on a global basis.

However, Morgan added: "Recent market moves perhaps suggest a broadening of market performance away from the domination of larger tech companies.

"It's a reminder to investors not to have a portfolio skewed too much in one direction and to consider rebalancing as different areas perform at different rates. Blending different approaches can lead to better balance and greater resilience to a variety of risks."

Japan offers a clearer example of value's recent strength. Improved corporate governance has lifted cheaper areas of the Japanese market, giving value-focused strategies there a tailwind that most global markets have lacked.

But the Charles Stanley Direct chief analyst warned investors against thinking they can constantly pivot portfolios between the two styles to capitalise on inflection points like this.

"To anticipate the market mood and switch back and forth between growth and value to improve performance is nigh on impossible," he said.

"Both growth and value investing strategies can perform well over the long term if the process is well implemented, so investors looking to maximise long-term returns through investing in shares should consider blending both styles."

Morgan pointed to several value funds that appear on Charles Stanley Direct's Preferred List as examples of how to add exposure to a portfolio.

Artemis Global Income, managed by Jacob De-Tusch-Lec, carries a value bias driven partly by its requirement to generate dividend income. The manager takes a disciplined, contrarian approach, often seeking turnaround situations where out-of-favour companies recover through an industry pick-up or management action.

Henry Dixon and Jack Barrat’s Man Undervalued Assets focuses on the current shape of a company's balance sheet rather than forecast earnings. The managers target UK-listed companies trading below their assessment of replacement cost, or whose profit streams they consider undervalued, while favouring businesses with little or no debt.

Fidelity American Special Situations targets US companies that have gone through a period of underperformance and are undervalued by the market. The manager assesses balance sheet strength, asset backing and business resilience and the fund trades at a sizeable discount to the index on traditional valuation metrics.

Nitin Bajaj's Fidelity Asian Values draws on a Buffett-influenced approach that targets resilient businesses run by trustworthy management teams at a good price. This tends to lead the fund toward smaller companies that are not widely followed by professional investors, across markets including China, India and south-east Asia.

Man Japan CoreAlpha runs a high-conviction value strategy that has benefited from improved corporate governance in Japan. The management team believes cyclicality strongly influences most sectors of the Japanese market and it currently holds sizeable weightings in banks, insurance and autos.