Three quality-growth managers have just placed different bets on which companies will win, each coming up with differing answers to the question of whether momentum can be fought or must be joined. But a brutal fortnight for the momentum factor shows why none of them can yet claim to be right.

This week, Bank of America's latest Global Fund Manager Survey found 82% of investors see 'long global semiconductors' as the market's most crowded trade, the highest reading the survey has ever recorded for any single position, as momentum money piled into the same handful of AI-linked names.

It also revealed that 45% of professional investors see AI as being in a bubble, the highest reading yet for that fear. But 61% don't expect AI hyperscalers to cut capex this year and cash levels have fallen to 3.6%, the lowest in years.

So it looks like fund managers are both worried about the AI trade and fully invested in it at the same time. That same contradiction has also played out across three well-known global equity funds.

Within the past fortnight, Fundsmith's Terry Smith, Rathbones' James Thomson and Lindsell Train's James Bullock have each given their answer to the question on what to do when momentum is setting share prices.

Smith eased Fundsmith Equity's longstanding 'do nothing' rule and said he would take more account of momentum when making investment decisions. He raised turnover to a high of 51.8% in the first half of 2026 and bought into the AI ecosystem, including a fresh stake in TSMC, the world's largest contract chipmaker.

As well as information technology, Smith bought industrials, financials, healthcare, consumer discretionary and communication services companies.

Thomson kept his Rathbone Global Opportunities fund's AI winners, Nvidia, Arm and CrowdStrike among them, but built a defensive flank: HALO (hard assets, low obsolescence) stocks like Caterpillar, Sandvik and Howmet, plus staples such as L'Oréal. His bet is that market leadership broadens out rather than reverses.

Bullock went the opposite way, adding to Lindsell Train Global Equity's stake in Intuit, a stock Smith and Thomson had both just sold, and other beaten-down software and data companies. His argument is that the 'AI loser' sell-off is a momentum story feeding on itself, not a verdict on the businesses involved.

It's only fair to point out that all three of these funds have strong long-term track records but have struggled more recently and are in the IA Global sector's bottom decile over the past year.

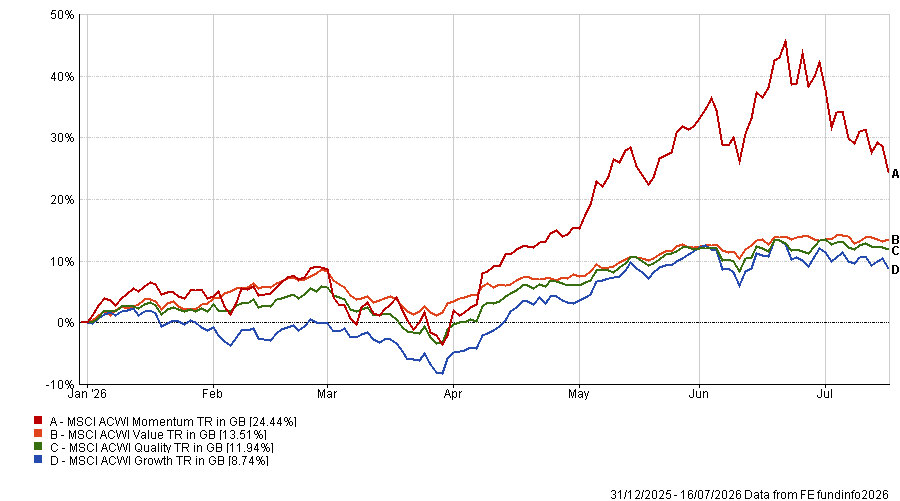

Momentum investing has dominated markets in 2026, with the MSCI AC World Momentum index gaining more than 40% in sterling over the first half. The quality, value and growth indices were all up around 12-13%.

But since 1 July, the momentum index is down 12.5%. The global value index is broadly flat, while quality has fallen 1.3% and growth has slipped 3%.

Performance of investment styles in 2026

Source: FE Analytics. Total return in sterling between 1 Jan and 16 Jul 2026

Of course, the momentum index is a quantitative factor built from stocks with the strongest recent price gains, not a direct stand-in for AI stocks. But there is some overlap – eight of the index's largest constituents are in the information technology sector, including Micron Technology, SK Hynix and TSMC.

Two weeks is a very short period in investment and won't settle who's right. All three managers are running portfolios built for years, not days. But for investors there are some questions worth asking.

Smith's move is the clearest to categorise. After years of 'do nothing', he's essentially decided that if you can't beat momentum, you join it, buying TSMC, a name sitting right at the centre of the world's most crowded trade.

Fairview Investing's Ben Yearsley asked, after 16 years running the fund one way, why the change now? If the answer is 'to catch the AI trade', has Smith arrived just as that trade starts to wobble?

Bullock sits at the other end. His addition to Intuit is a value argument: he's betting the stock's price and its underlying business will eventually reconnect, backed by unique datasets and switching costs he thinks the market is mispricing. It's a call that momentum has overshot and that overshoots correct, given enough patience.

Thomson isn't chasing the crowded AI/semiconductors trade; he's stepped out of it, into HALO names and defensives. But several of those names, particularly ones tied to data centre buildout and grid infrastructure, still sit close to the AI story he's supposedly diversifying away from.

So Thomson may be doing something genuinely different: stepping out of an overheated trade into a more attractive one. Or he may just be swapping one momentum bet for another. It's hard to tell which from where we stand now.

Momentum-driven markets rarely correct gently. The same flows that push prices up tend to reverse in the same way and the recent crack in the momentum trade should serve as a reminder that, ultimately, investments can never go up in a straight line forever.

Three managers have now shown their hand: Smith has bet that joining the crowd pays off from here, Bullock has bet that the crowd has already overreacted and Thomson has bet that leadership broadens without needing to call the top or bottom of anything.

The next few months, particularly how the momentum factor behaves from here, might start to show which wager is closest to right.

Gary Jackson is head of editorial at FE fundinfo. The views expressed above should not be taken as investment advice.