Past performance does not predict future returns. You may get back less than you originally invested. Reference to specific securities is not intended as a recommendation to purchase or sell any investment.

The general industry cycle is inflecting, and the evidence is now coming from every link in the chain.

For two years the bear case on general industry has been simple: a multi-year destock, soft China, and expensive project finance. That argument is now significantly harder to make. Three of the most informative bellwethers in the global industrial economy reported in the same window – Texas Instruments, Keyence, and United Rentals – and each delivered the same message. When the silicon, automation, and build-out all inflect together, it is no longer a vertical-specific story or a restock. It is the start of a cycle.

These three companies are not interchangeable data points – they sit at deliberately different positions in the chain. Texas ships the analog and embedded silicon that goes into virtually every piece of industrial equipment. Keyence ships the sensors and machine vision that customers buy when they are committing capex to new lines, not just maintaining old ones. United Rentals rents the gear that builds the sites where that equipment ends up. When all three accelerate in the same window, the inflection signal is much stronger than any single name in isolation.

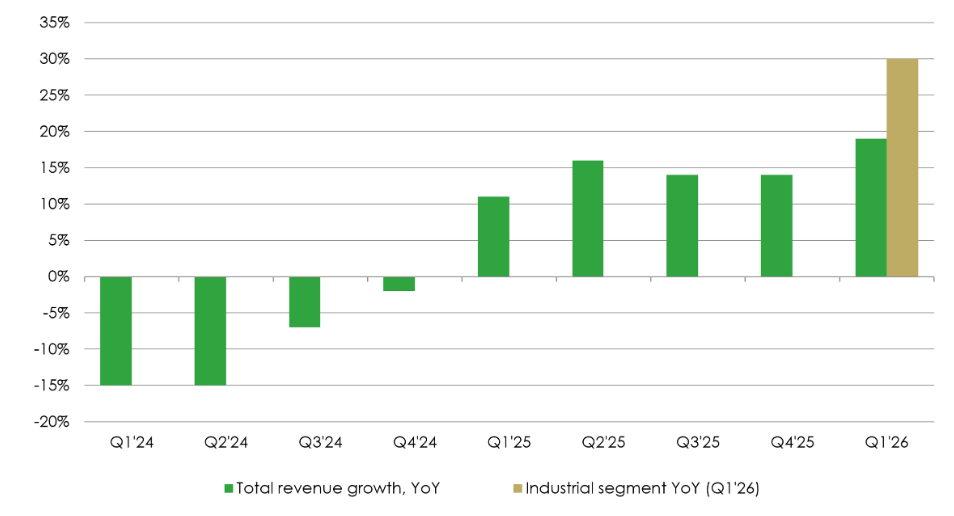

The clearest single picture is the trajectory of Texas, the most cyclical and earliest of the three to report results:

Texas Instruments: revenue growth (YoY, %)

Source: Liontrust, Texas Instruments, April 2026

Two things stand out in its first-quarter results released in April. First, the destock was deep – Texas was running -16% YoY (year-on-year) at the trough – so the 35-point swing to +19% in seven quarters is meaningful, not a base-effect optical illusion.

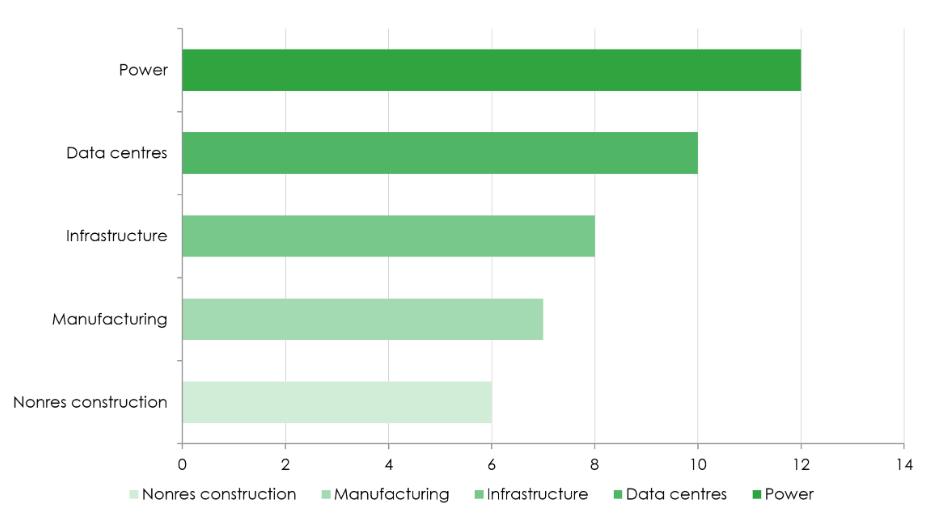

Second, the industrial segment is now leading rather than lagging, the textbook signature of a real cycle turn rather than a tech-driven pull from data centres alone. The corroboration from United in its own first-quarter results is in where the demand is coming from:

United Rentals: Q126 revenue growth by end market (YoY, %)

Source: Liontrust, United Rentals, April 2026

The breadth here is the key. If only data centres were lifting, the cycle thesis would be weaker – that would just be the AI infrastructure trade in another wrapper. Power running double-digit, with infrastructure, manufacturing, and non-residential construction all positive, is the broad-based picture you need to see for an industrial cycle to be real.

Keyence quarterly results rounds out the picture by confirming pricing power has returned alongside the volume. Sales +10.4%, net income +11.7%, all delivered at a 51% operating margin, and a dividend hike from ¥350 to ¥550 – a 57% step-change that management committed to maintain. Keyence is famously conservative on capital return; a move of this magnitude is a deliberate signal that demand durability has changed, not a one-good-year reflex.

What does this mean for portfolios? The industrial complex has been treated as a late-cycle, rate-sensitive sector to be underweight while AI infrastructure buildout was the only game in town. That framing is now stale. The companies supplying chips, automation, and equipment to the physical economy are themselves operating into accelerating demand, with pricing power returning and order books extending. The classic industrial cycle is not a substitute for the AI infrastructure cycle; it is a parallel one, increasingly intertwined with it through power and data centre build-out, and now broadening into the rest of the real economy. The market is still pricing these names as if 2024's destock is the steady state. The evidence from this earnings season says otherwise.

Read, watch and listen to more insights from Liontrust fund managers here >

KEY RISKS

Past performance does not predict future returns. You may get back less than you originally invested.

We recommend this fund is held long term (minimum period of 5 years). We recommend that you hold this fund as part of a diversified portfolio of investments.

The Funds managed by the Global Innovation team:

-

May consider environmental, social and governance ("ESG") characteristics of issuers when selecting investments for the Funds.

-

May hold overseas investments that may carry a higher currency risk. They are valued by reference to their local currency which may move up or down when compared to the currency of a Fund.

-

May have a concentrated portfolio, i.e. hold a limited number of investments or have significant sector or factor exposures. If one of these investments or sectors / factors fall in value this can have a greater impact on the Fund's value than if it held a larger number of investments across a more diversified portfolio.

-

May encounter liquidity constraints from time to time. The spread between the price you buy and sell shares will reflect the less liquid nature of the underlying holdings.

-

Do not guarantee a level of income.

The risks detailed above are reflective of the full range of Funds managed by the Global Innovation team and not all of the risks listed are applicable to each individual Fund. For the risks associated with an individual Fund, please refer to its Key Investor Information Document (KIID)/PRIIP KID.

The issue of units/shares in Liontrust Funds may be subject to an initial charge, which will have an impact on the realisable value of the investment, particularly in the short term. Investments should always be considered as long term.

DISCLAIMER

This material is issued by Liontrust Investment Partners LLP (2 Savoy Court, London WC2R 0EZ), authorised and regulated in the UK by the Financial Conduct Authority (FRN 518552) to undertake regulated investment business.

It should not be construed as advice for investment in any product or security mentioned, an offer to buy or sell units/shares of Funds mentioned, or a solicitation to purchase securities in any company or investment product. Examples of stocks are provided for general information only to demonstrate our investment philosophy. The investment being promoted is for units in a fund, not directly in the underlying assets.

This information and analysis is believed to be accurate at the time of publication, but is subject to change without notice. Whilst care has been taken in compiling the content, no representation or warranty is given, whether express or implied, by Liontrust as to its accuracy or completeness, including for external sources (which may have been used) which have not been verified.

This is a marketing communication. Before making an investment, you should read the relevant Prospectus and the Key Investor Information Document (KIID) and/or PRIIP/KID, which provide full product details including investment charges and risks. These documents can be obtained, free of charge, from www.liontrust.com or direct from Liontrust. If you are not a professional investor please consult a regulated financial adviser regarding the suitability of such an investment for you and your personal circumstances.