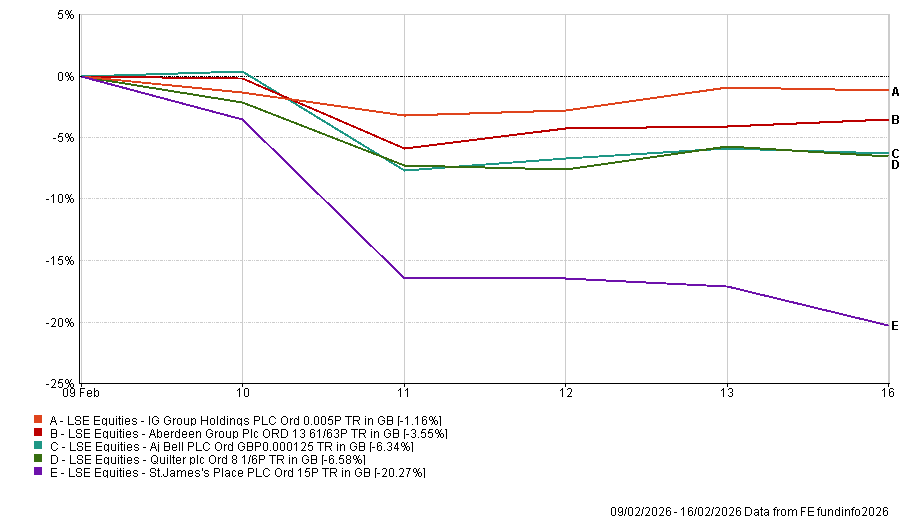

UK wealth managers took a sharp knock last week after a US fintech startup spooked markets into treating the entire sector as the next AI casualty. Shares in Aberdeen Group, Quilter, IG Group and AJ Bell fell between 1% and 7%, while St James's Place tumbled about 20%, as shown in the chart below.

The sell-off was triggered by wealth management startup Altruist's decision to introduce artificial intelligence (AI) in its tax-planning offering, fuelling fears that human advice could soon be automated at scale.

Schroders was the exception, its shares soaring 28.6% after US asset manager Nuveen announced a recommended cash offer valuing the firm at £9.9bn.

Performance of stocks last week

Source: FE Analytics

Bloomberg Intelligence analyst Neil Sipes described the sell-off as “tied to broader concerns about AI disrupting the financial advice and wealth management model,” with investors focusing on “concerns around efficiencies being competed away, fee compression long-term and potential market-share shifts”.

Launched on 10 February 2026, Altruist's new platform, Hazel, can generate personalised tax strategies for clients by pulling together their tax returns, payslips and account data. Altruist chief executive Jason Wenk said the tool “makes average advice a lot harder to justify.”

Nick Clay, manager of the Redwheel Global Equity Income fund, sees the panic as symptomatic of a market prone to wild swings between extremes. “Confidence has flipped quickly,” he said.

“We went from complete confidence that spending trillions building AI was a great thing to do, to complete confidence that every software company is going to be replaced by AI. The truth is somewhere in the middle.”

The volatility, Clay argued, reflects a market that has forgotten what normal looks like after consecutive years of gains in the MSCI World index. “A couple of AI bots get announced and everybody starts to panic, and certain parts of the market get taken out,” he said. “That's the place the market has got itself to.”

For Tim Levene, chief executive of Augmentum Fintech, AI-driven personalisation of wealth management is not to be seen as a threat to incumbents but as a structural shift that will ultimately benefit millions of ordinary investors.

“It's an inevitability that we will see a dramatic shift in the personalisation of long-term wealth management that appropriately risk-weights while understanding personal circumstance,” he said.

His starting point is how poorly served most people currently are. Traditional wealth managers can only serve so many clients, leaving the masses without the kind of continuous, tailored oversight that more seasoned investors take for granted.

“I think it's fair to say a vast majority of the population is not investing effectively to date, including those that are aren't in a scenario where there's ongoing optimisation,” he said.

AI changes that, with tools that have sight of a client's salary, net wealth, family circumstances and market exposure simultaneously, updating their view as life changes.

“Am I overweight equities, underweight commodities, underweight crypto? The tool is looking at your circumstances in the totality at any one point, constantly rebalancing and optimising,” Levene said.

The result would be actively managed portfolios accessible to people who today receive no meaningful service at all. “We're not there today, and I'm not saying we'll be there in a year or two, but I do think we're going to be a long way on that journey in three to five years.”

His broader thesis is that fintech still has the majority of its disruption ahead of it, a “fintech 2.0” wave. Disruptors account for less than 5% of a $15trn global financial services market, he noted.

“I think we're going to see a total transformation over the next five years in many sectors, particularly in insurance, wealth management and asset management. There's a lot to be excited about.”

Holly Mackay, chief executive of consumer research firm Boring Money, agrees that AI will reshape the economics of advice but struck a more moderate tone.

“AI has huge potential to change and improve both the delivery and costs of advice,” she said. “But the recent panic and sell-off ignore the very human need for trust and validation from a trusted person.”

According to Boring Money's Advised Investor Tracker, 94% of all advised clients report having absolute trust in their adviser.

“AI might spit out some calculations but we still don't trust it,” Mackay said. “That mistrust and need for trusted human validation will not be replaced by AI for at least a few years yet, and this will be true for both DIY and advised customers.”

Where Mackay does see near-term change is in back-office and support roles rather than front-line advice. She believes the paraplanner role will come under pressure as AI improves efficiency, and that costs and minimum service thresholds should fall as a result. At the same time however, client volumes will rise to compensate.

“The model's not dead, it just needs to evolve,” she said.

In asset management, Clay sees AI as likely to compress returns rather than expand them. “If everybody uses the same tools, they end up in the same stocks and create bubbles,” he said.

“AI doesn't change the fundamental dynamic of markets, which is overvaluation and undervaluation driven by human emotions. It may make data processing more efficient, but it doesn't improve your ability to choose the right stock,” he concluded.