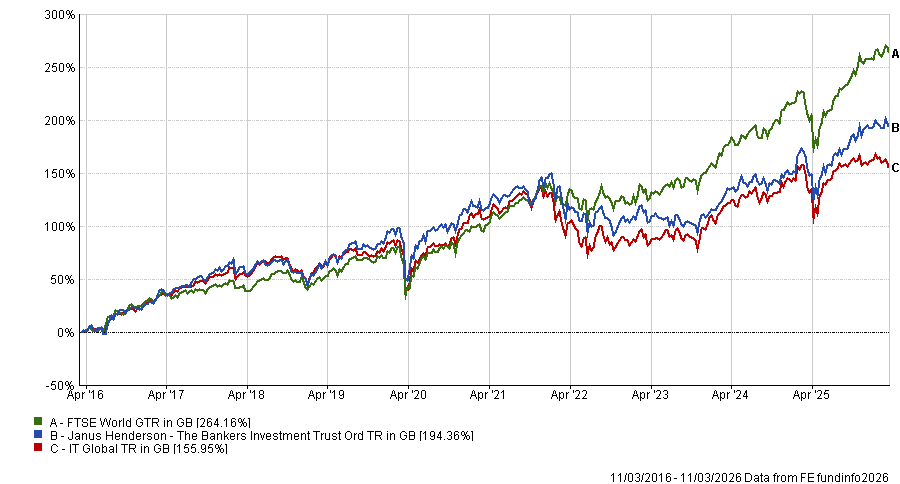

The £1.3bn Bankers investment trust has had a difficult decade, languishing in the bottom half of the IT Global peer group and failing to beat the FTSE World benchmark during this time.

Recently, this has led to sweeping changes. Last year, the trust reduced the number of holdings to around 100 and cut the number of regional ‘sleeves’ it invests in from six to four: Europe (including the UK), North America, Japan and Asia.

In particular, the trust has adapted its approach to the US. The portfolio had been significantly underweight the region due to its value approach, causing it to significantly underperform in the early 2020s, culminating in a bottom-quartile year in 2023.

Performance of trust vs sector and benchmark over 10yrs

Source: FE Analytics

To address this, co-manager Richard Clode was brought onto the trust in September 2025, taking over the US portion of the portfolio. He is using his experience in running the £1.7bn Janus Henderson Global Technology Leaders fund, pivoting the trust’s US exposure to a more growth-oriented approach.

Previously, the managers of each region invested for both growth and income. Now, however, they are playing to the strengths of individual markets.

“I see my job in the US as finding growth opportunities, but that’s okay because if we get a growth‑to‑value rotation like we’ve had in the past few months, I will underperform in the US but we’ve got plenty of value and income‑yielding stocks in Europe, Japan and Asia, and that helps offset and provide balance,” he said.

Clode works alongside veteran stockpicker Alex Crooke, who has been in charge of Bankers since 2003. But while his co-manager remains the same, the trust is moving in a new direction.

“Things are changing, Bankers is evolving. The trust has been around since 1888 and you’re not around for that long if you don’t evolve and change,” said Clode.

“With me coming on board I think that only accelerates that journey and should give us a better chance to be able to outperform in the future.”

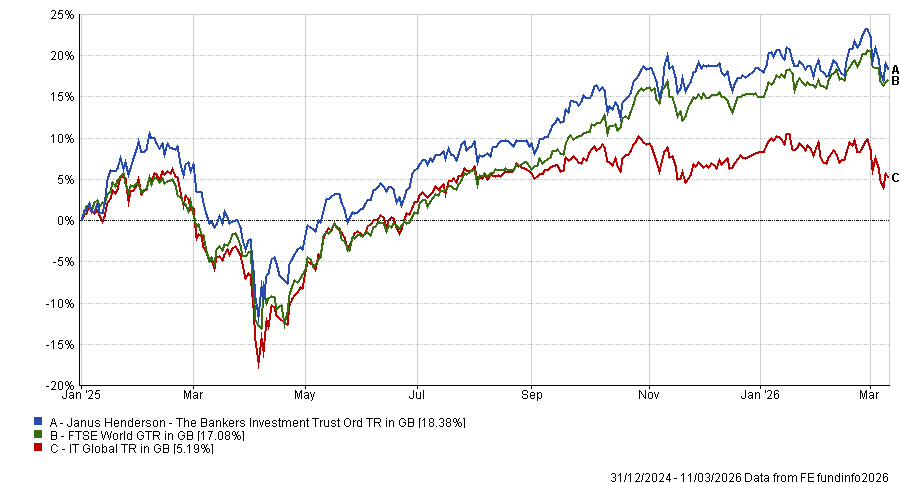

There are already signs of progress. In 2025 the trust made 18.5%, the third-best performance in the IT Global sector. So far this year, it is broadly flat (a 0.1% loss) at a time when most peers have dropped much further.

Performance of trust vs sector and benchmark since the start of 2025

Source: FE Analytics

“Last year was better and we did a much better job against the benchmark. I can't take credit for this; it was well before I turned up. But that’s what you want in active funds – that’s why you pay the fees you do,” he said.

“We acknowledge the underperformance from years gone by and we’ve started to do a better job. We still need to do a better job than that, but we think we've got the pieces in place to be able to do that from here. I think if we keep delivering double‑digit returns to our shareholders, they’d generally be happy.”

Below, Clode explains how the entire trust approaches picking stocks, confirms Bankers will up its dividend for the 60th consecutive year in 2026 and discusses why Nvidia is now the trust’s largest holding after years of not owning US tech giant.

What is your process for picking stocks?

We follow profits and cashflow. Ultimately, if we're going to deliver double‑digit returns over the long term, the only way to sustainably deliver that is to have a portfolio that has double‑digit earnings and cashflow growth. That's what gives capital appreciation and helps support our growing dividend over time.

We mainly use price‑to‑earnings and free cash‑flow yield. There are certain areas where price‑to‑book might be more relevant, but we’re certainly not doing price‑to‑sales or EV/EBITDA [enterprise value/earnings before interest, taxation, depreciation and amortisation] or longer‑term DCFs [discounted cashflows] and things like that.

The trust is a ‘dividend hero’ but is it necessarily an income fund?

Bankers has always had a balance. We believe that, to deliver the financial outcomes our shareholders want, there is a balance of capital appreciation and income.

The decision was made a few years ago not to go too far down the income route because it really does constrain your ability to capture some of the growth in innovative areas of the market, particularly in the US.

We view Bankers as sitting between your more income‑ and value‑oriented trusts out there and then your Scottish Mortgages at the other end.

Is the dividend still a priority?

We like having that dividend and we're committed to keeping growing it. We’ll grow it again next year for the 60th consecutive year.

It provides discipline. We ask our companies to pay dividends because it disciplines their capital allocation and we want to keep paying dividends to our shareholders because it disciplines our investment process and stockpicking.

It’s something that’s nice to have: we'll pay you some income and we’ll grow that dividend above CPI [the consumer price index] over the long term. But we think [if] we’re going to deliver double-digit returns [a lot of it has to come] through capital appreciation over the long term.

What have been your best and worst performers in the past year?

Obviously some of the technology names, particularly – something like a Broadcom, which is playing into that AI compute side. But it’s not just tech. Some of the banks, such as NatWest and some of the other European holdings that we had, performed very well.

[Shares in Broadcom are up 39.6% since the start of 2025. NatWest’s shares have risen 43.1% over that period.]

On the flip side, our big detractor was UnitedHealth. There are some well‑known issues there in terms of top‑down and macro, but also some bottom‑up and company‑specific things that maybe we should have identified a bit earlier.

[Shares are down 45.2% since the start of 2025].

What changes have you personally made since joining?

When I looked at the portfolio, we had lower earnings growth versus the benchmark in the US. I would argue it’s hard to keep pace with a benchmark over the long term if you're consistently lower growth, as you're always then relying on re‑rating and trying to identify undervalued opportunities — which is hard to do consistently in my mind.

We leaned a bit more into that growth side and are now slightly above the growth rate of the index – but crucially we’re not massively overpaying for that additional bit of growth.

Why did you buy Nvidia for the first time in towards the end of last year and why is it now your biggest holding?

I think [previously there was a] slight constraint in terms of thinking about owning companies that had a more meaningful dividend yield. Our previous US manager preferred Broadcom, which provided a yield.

He thought that there was a better opportunity based on valuations and that played out pretty nicely. He was already shifting a little bit into Nvidia before I took over, so I didn’t take over with a 0% position.

Nvidia did well last year, up 40%, with most of that coming in the first half. Performance plateaued despite very good results through the back half [of 2025] so it got very cheap. It was trading at a market discount – a significant discount to Broadcom – so we thought it was a good time to take that on.

I cover Nvidia in our technology fund and have followed it for many years. Versus the rest of AI we think it's actually pretty attractively valued in relative terms.

What do you do outside of fund management?

I've got three sons who are pretty sporty. Two of them are very good tennis players. One can pretty easily beat me now and one I can just about beat. So that's what we spend most of our time doing – having very friendly, competitive tennis sessions between the family.

It’s a great way to keep them away from screens, do something healthy, keep me away from the stress of markets and do something together.