Overvaluation, portfolio concentration and a volatile macroeconomic backdrop has led the managers of the Allianz Technology Trust to go into 2026 “cautiously optimistic”.

In the £1.9bn trust’s full-year results, lead portfolio manager Mike Seidenberg argued for AI-driven secular growth and pent-up post-pandemic technology demand as the foundations for continued returns in the space. “These technology shifts come once every 12-15 years and when they occur, they tend to be very powerful,” he said.

However, he acknowledged that bubble fears are a persistent feature of such cycles. “People will always worry about a bubble, but when a secular change emerges, it tends to create significant value over the cycle,” he said. “It is our job to uncover this value and to look beyond the obvious opportunities to other parts of the market.”

Seidenberg said the tech spending environment, while not straightforward, contained a structural tailwind. In the aftermath of the pandemic, companies underspent on technology, leaving a reservoir of pent-up demand that has yet to be fully released.

He expected companies to need to demonstrate clear value before purchase orders increased materially. That requirement, he said, typically allows market leaders to take share while weaker competitors fade.

The manager also pointed to the IPO pipeline as a specific source of opportunity for this year. “2026 has the potential to be a robust year for IPOs with a number of high-profile companies waiting in the wings,” he said.

But he noted that “a number of factors need to line up” for those listings to proceed.

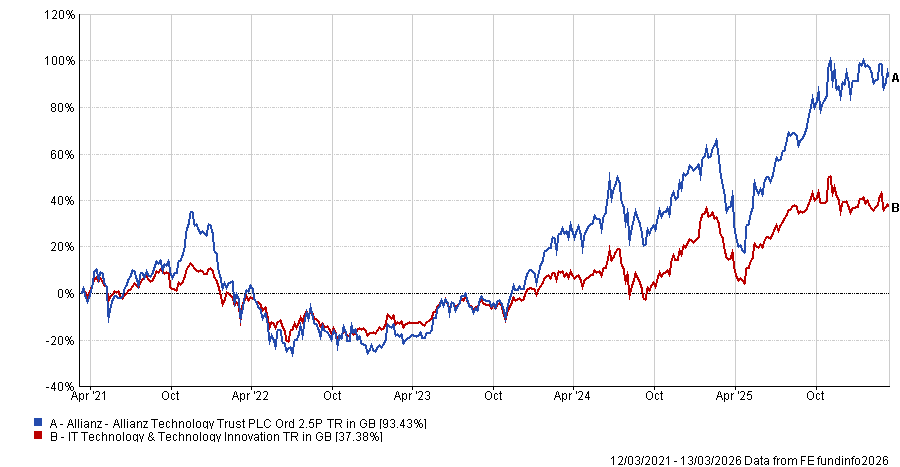

Performance of Allianz Technology Trust vs sector over 5yrs

Source: FE Analytics. Total return in sterling between 13 Mar 2021 and 13 Mar 2026

On the macro backdrop, Seidenberg said: “It is important not to let macroeconomic or geopolitical factors become a distraction. Our stock selection has to be governed by our deep dive on the stocks, rather than by the latest missive from the White House.”

He acknowledged that macroeconomic factors occasionally change a business model in a fundamental way but argued this happens far less frequently than markets assume. Technology’s role in driving differentiation across industries remained the anchor for his long-term enthusiasm.

Tim Scholefield, Allianz Technology Trust’s chairman, also pointed to geopolitical risk as a separate and growing source of market volatility.

A new world order appears to be emerging, he said, with disagreements and posturing becoming increasingly uncomfortable and carrying the potential to spill into wider conflict with significant market implications.

“Any volatility can be both good and bad for investors,” he said. “Certainly, it never feels comfortable while experiencing it live – but for the seasoned, dedicated and attuned investor, therein lies opportunity.”

One tech area that has commanded investor attention – both for its potential opportunities and its potential risks – is AI.

Scholefield characterised the current debate over AI as producing two distinct camps: those who believe valuations are beginning to overheat, and those who see sufficient evidence of AI-driven revenue or margin improvement to justify higher prices today.

He added that the market had called an AI bubble multiple times during the past year, with share prices reacting accordingly on each occasion.

Seidenberg drew a clear distinction between the current AI cycle and the dot-com era.

The dot-com boom, he said, was characterised by weak businesses failing to solve meaningful problems, whereas many AI companies are tackling large, real-world challenges. Hyperscalers have also built far greater dominance over the AI ecosystem than the internet’s first movers ever achieved.

“Public market valuations remain high, but – for the most part – are not excessive and not nearly as high as at the peak of the dot-com euphoria,” the manager said.

“We do see signs of exuberance in some of the private equity valuations and are watching capital spending carefully. Companies recognise that it could be an existential threat if they get AI wrong – they risk becoming obsolete. This could prompt some potential capital misallocation, but a rigorous bottom-up approach ensures that we can avoid any excesses.”

Allianz Technology Trust’s outperformance in 2025, when the trust returned 24.7% against its benchmark’s 20%, was partly driven by the team’s decision to own meaningfully fewer mega-caps than the index.

“In a diversified, actively managed portfolio, it would not be prudent to hold Nvidia at index weight or above,” he added. “And so, even though it is our largest holding, Nvidia did not deliver outperformance versus our benchmark.”

Seidenberg said the dominance of the Magnificent Seven had been a headwind for active technology strategies in prior years. That dynamic reversed in 2025 as investors recognised that AI growth could be captured across a wider range of companies.

The portfolio held 47.5% in companies valued at more than $1trn, roughly 12 percentage points below the benchmark weighting, and that underweight became a tailwind in 2025 as investors turned their attention to the broader AI ecosystem.

Semiconductor stocks were the portfolio’s standout performer in 2025. The sector accounted for 32.5% of the portfolio and delivered an average return of 45.6%, with Micron the single largest contributor to overall performance. The investment rationale centred on exposure to the infrastructure underpinning AI growth rather than the most visible platform names.

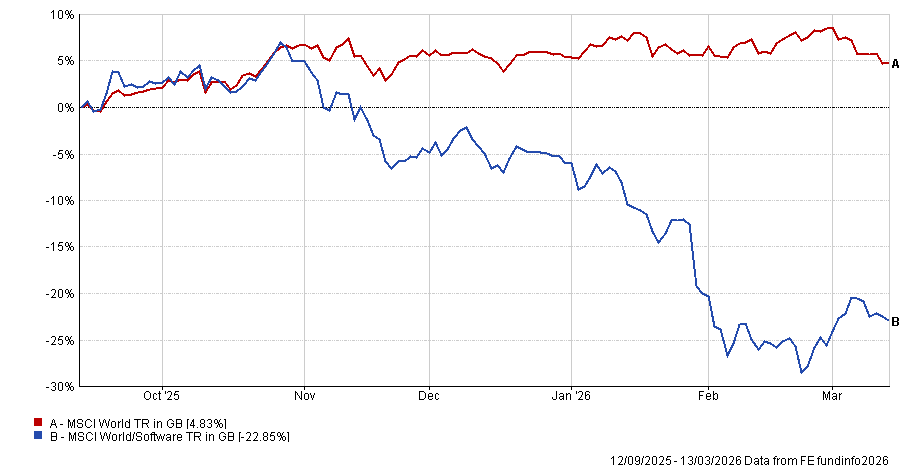

Performance of software stocks vs global equities over 6m

Source: FE Analytics. Total return in sterling between 13 Sep 2025 and 13 Mar 2026

Software told the opposite story with software stocks selling off heavily recently on fears that AI agents would displace traditional products.

Seidenberg said the growth differential was stark: semiconductors were growing at more than 30%, against 10-12% for software. He added, however, that valuations had fallen to levels where selective opportunities were beginning to emerge.

“There is a question over whether they have gotten too cheap – the decrease in value has been extraordinary. We are finding some interesting opportunities. MongoDB, for example, has been hit hard over the year. It is a good example of a company that hasn’t been able to prove to investors that it is part of the deployment of AI workloads, but we see value there,” he finished.

“Elsewhere, we continue to look at software companies in detail, visit their premises and pore over the data. We need to be sure that not owning them at these valuations is the right position.”