Capitalism has its positives and its flaws, but when working well it should be a mechanism to drive money to the more efficient areas that best use people’s money.

In the era of low interest rates, this theory flew out of the window, as cash was prevalent and companies with no business remaining alive continued to borrow money cheaply to prop themselves up.

Over the past few years, this has reversed. Interest rates have risen, lifting the amount owed on repayments for the debt taken out during the ultra-low rate environment of the 2010s.

For the companies that only survived due to the abundance of cheap loans, this has been a death knell.

Rob Burdett, head of multi-manager at Nedgroup Investments, says investors should get used to this moving forward, noting that the world is unlikely to go back to the zero or negative rates of the recent past.

“I think that sorts the wheat from the chaff in the real economic world of commerce and that will reflect in the creative destruction of capitalism,” he said, adding that this will require a heavier emphasis on stock selection than investors have needed since the financial crisis of 2008.

It will affect all areas of the market. For example, tech start-ups will need to be the best in their particular niche to attract funding. Meanwhile, the companies with leverage will need to demonstrate their worth in order to increase margins and stave off their new higher rates.

For established brands (often plonked in the ‘quality’ bucket), now more than ever they will have to prove that their customers have brand loyalty as they increase higher costs.

But this rejuvenation of capitalism is not just at the stock level – the investment trust landscape is changing too.

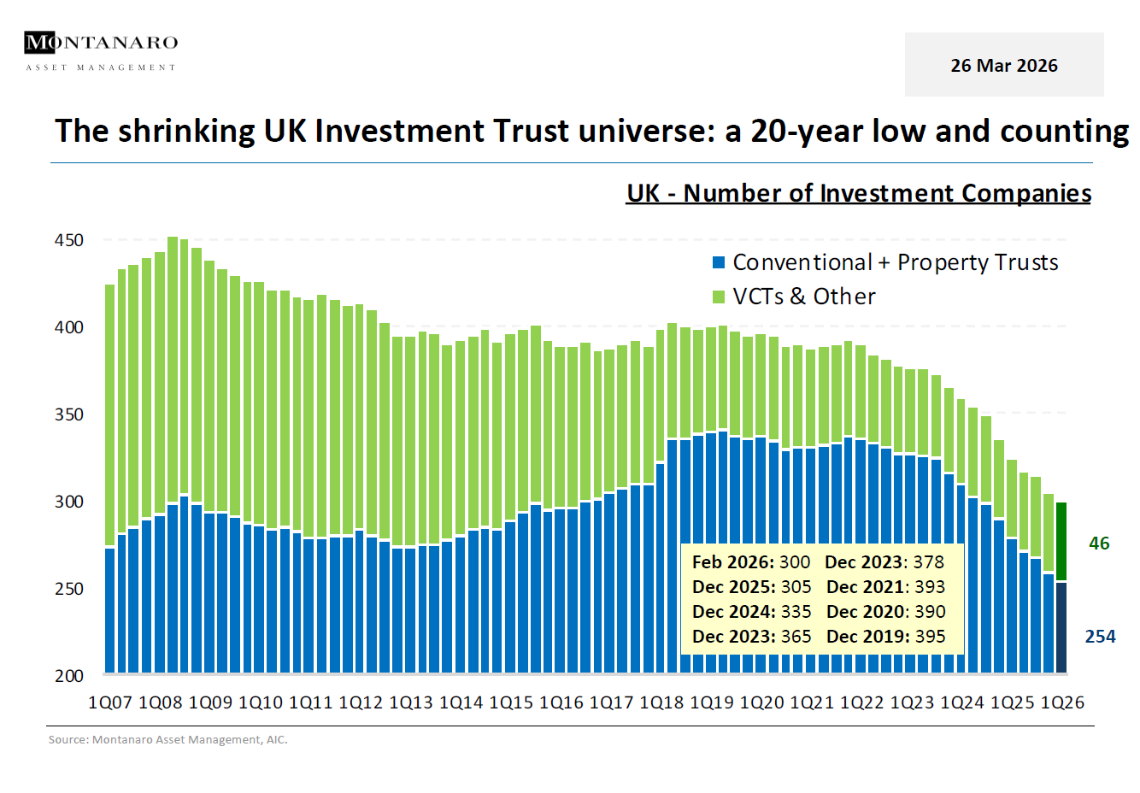

A chart this week from Montanaro highlighted the stark reality that faces investment companies. It shows that the number of such closed-ended funds have plummeted in recent years from a peak of 395 in December 2019 to 300 today – an almost 25% reduction.

Some will point to the ‘Saba Capital effect’. The US hedge fund has launched an active campaign against numerous trusts, aiming to put its nominees on boards and replace incumbent managers with its own.

While it has been persistently beaten by shareholders, its effects are wearing on its targets, with several opting to close or merge.

For example, Edinburgh Worldwide is currently urging shareholders to approve a 100% cash exit to stop the controversial US hedge fund from gaining control of the trust. It is essentially proposing to wind itself up rather than allow Saba to take control.

But Saba is not the only reason why this is happening. For too long the space has been home to stale, out-of-date investment trusts offering nothing particularly different to their open-ended peers.

For defensive investors, they can now get access to reasonable yields from cash and bonds – making the case for certain income-paying trusts difficult. Meanwhile, more aggressive investors can get strong returns from stock markets, either actively, passively or through increasingly popular ‘passive plus’ options.

This has led to persistently wide discounts in recent years as investors have moved away from investing in trusts to other areas.

While there are a number of brilliant investment trusts, it is no bad thing that capitalism is back working as intended: culling the weak and leaving only the strong to survive.

Jonathan Jones is editor of Trustnet. The views expressed above should not be taken as investment advice.