As the end of financial year approaches, many investors may be taking the opportunity to review their portfolios and make final top-ups to their ISAs before the deadline.

While many investors use their Stocks & Shares ISAs to access funds and investment trusts, others may prefer to also make use of the ‘stocks’ element of the wrapper by backing individual UK companies directly.

To offer insight into the parts of the UK market attracting professional attention, Trustnet asked UK fund managers which stocks they currently favour within their own portfolios.

These are not recommendations but potential ideas for investors exploring the UK stock market this ISA season.

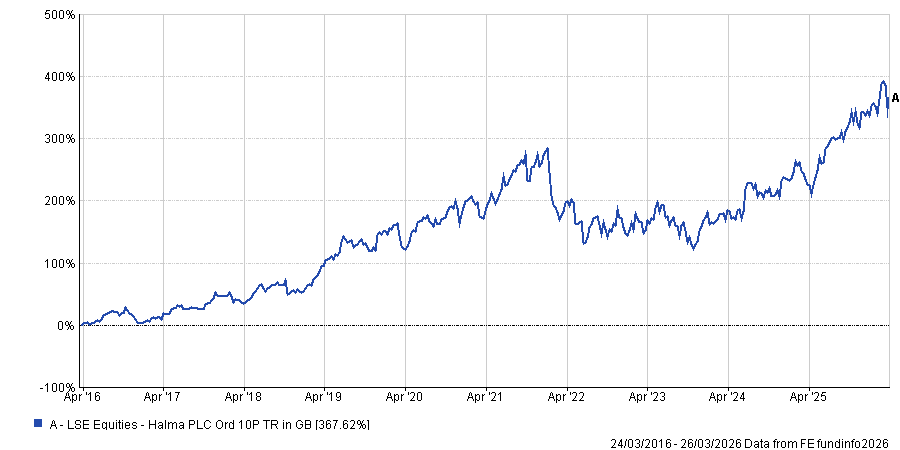

Halma

Alexandra Jackson, manager of Rathbone UK Opportunities, highlighted Halma, a decentralised group of safety equipment companies, as a reliable compounder in the fund’s portfolio.

She said this “niche focus” drives Halma’s consistently strong performance, with an organic revenue growth of 6-7% over a decade and an earnings before interest and tax (EBIT) margin of around 20%.

She said Halma can be seen as a bond-proxy because of this steady, compounding profile, adding that it can be susceptible to share price falls when bond yields rise.

Halma’s total return over 10yrs

Source: FE Analytics

“Every year, Halma quietly does what we like our companies to do: execute well, reinvest sensibly in itself and deliver steady growth,” Jackson said.

More recently, she noted that Halma has gained AI beneficiary status through its photonics division, which is supplying products to a large hyperscaler – “possibly Meta”.

“Being exposed to this theme has not only driven earnings upgrades but also very strong share price momentum in recent months,” she said.

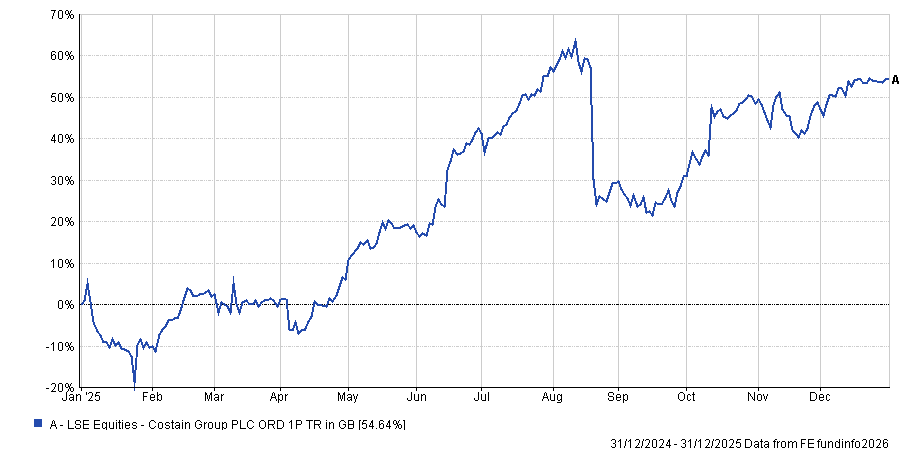

Costain

Ken Wotton, portfolio manager of Strategic Equity Capital, said British construction and engineering company Costain “is well-positioned to capitalise on several key tailwinds”.

He pointed to the UK government’s 10-year Infrastructure Strategy, which offers “significant growth potential” across Costain’s core markets – transport, water and energy.

In the company’s full year results for 2025, it reported a 9% adjusted operating profit growth and a 4.5% adjusted operating margin. Strong cash generation has also resulted in a strengthened balance sheet which will support increased shareholder returns, with the company confirming it will proceed with a £20m share buyback programme in 2026 and implement its target dividend cover of 3x adjusted earnings.

“Costain is also set to rejoin the FTSE 250 for the first time in 20 years,” Wotton said, adding that its “robust financial position and strong balance sheet provide the flexibility to invest in growth initiatives and navigate potential industry challenges”.

Costain’s total return in 2025

Source: FE Analytics

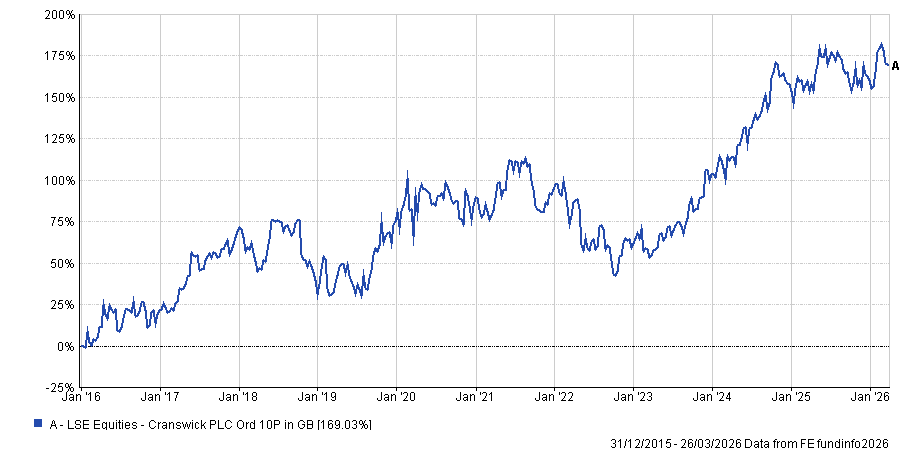

Cranswick

A potential growth stock option may be food producer Cranswick. Jean Roche, manager of Schroder UK Mid Cap, said the fund bought Cranswick in 2016 and, since then, the company has grown into a major player in the pork, poultry and convenience food sector, supplying UK supermarket chains such as Lidl, Sainsbury’s and M&S.

“Margins have expanded and significant cashflow generation has been both reinvested and paid back to shareholders,” Roche said.

Its share price growth has reflected this, with a total return of more than 190% – or 11.6% per year – since the Schroder fund first invested in the company, she noted, adding that the company “may have the hallmarks of a future FTSE 100 company”.

Cranswick’s share price performance since 2016

Source: FE Analytics

Cranswick is also a core position for Anthony Lynch, manager of JPMorgan Claverhouse Investment Trust.

Lynch said the company has invested heavily in capacity and automation, which has added to its ability to scale efficiently while improving margins – “a key advantage as rising labour costs pressure more highly leveraged peers”.

He added that the company offers the trust an “attractive blend” of stability, income and growth.

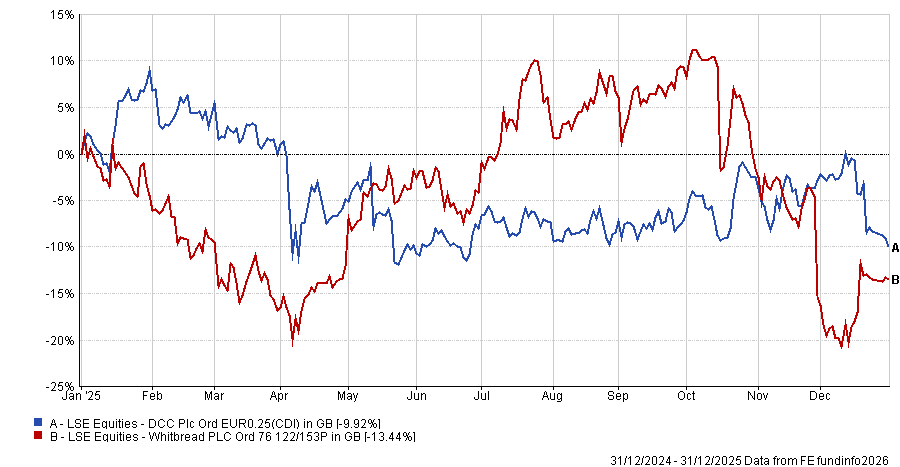

DCC

FTSE 100 company DCC offers international sales, marketing and support services across the energy, healthcare and technology sectors.

FE fundinfo Alpha Manager Alex Wright, portfolio manager of Fidelity Special Situations and Fidelity Special Values, pointed to the restructuring of its energy-focused business – “an area where it holds a strong track record of generating attractive returns on capital and growing through acquisitions”.

“The company fulfils our downside criteria given its shares trade close to trough valuation levels, while management are delivering substantial share buybacks from its disposals, which are highly accretive to its earnings power,” he added.

Wright noted that market sentiment around the company has been weak, largely driven by concerns around the structural decline of its fossil fuel distribution business.

“We believe these fears are overdone and the substitution effect is likely to be slower than expected,” he said.

DCC is also continuing to scale its renewable energy activities, including solar installation and other energy efficiency-focused solutions.

“The company’s defensive ‘utility’ characteristics and attractive valuation make it stand out as a compelling turnaround opportunity,” Wright said.

DCC reported a 4.5% decrease in revenues of £18bn, a 2.9% increase in adjusted profits to £617.5m and free cashflow conversion of 84% for the year ending 31 March 2025. It proposed a 5% increase in the annual dividend to 206.40p, marking 31 years of dividend growth.

Whitbread

A potential UK value stock for investors’ ISA portfolios could be hotel and restaurant company Whitbread.

Simon Gergel, manager of Merchants Trust, said the medium-sized business has an established presence in the UK – particularly through its ownership of hotel chain Premier Inn – and a growing presence in Germany.

“The business has a strong competitive advantage over peers due to its scale, its brand and a large freehold asset base,” Gergel said.

“The long‑term investment case centres on its five‑year growth plan, to repurpose underperforming restaurant space into additional rooms, grow the estate in the UK and Germany and drive efficiencies, as well as recycling capital for investment and share buybacks.”

He said that these factors have not yet been reflected in the share price.

Indeed, the company disclosed a 1% decline in revenue – from just shy of £3bn in 2024 to £2.9bn in 2025. Similarly, net income fell from £312.1m to £253.7m and earnings per share (EPS) decreased from £1.61 to £1.42.

Year to date, the company’s share price is down 9.4%.

DCC and Whitbread’s share price performance in 2025

Source: FE Analytics

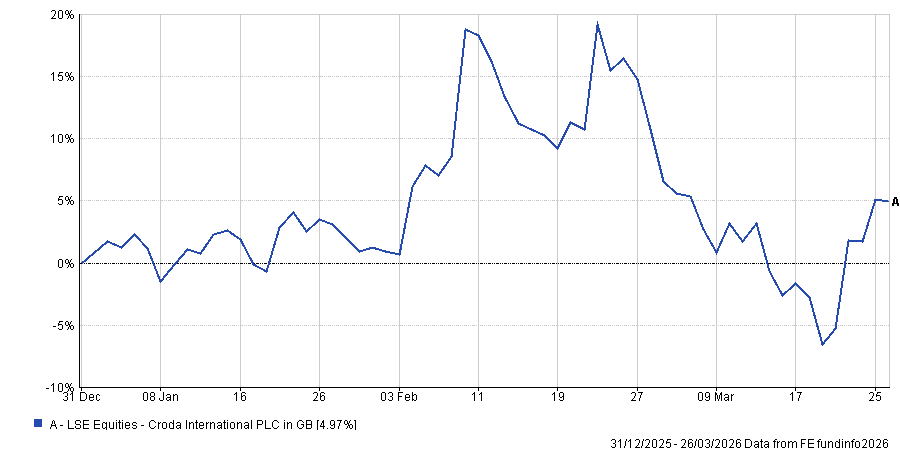

Croda International

Specialty chemicals company Croda International has a long track record of high margins, strong growth and attractive returns, according to Dominic Younger, lead manager of CT UK Capital and Income Investment Trust.

“More recently, performance has been impacted by softer end markets and a period of elevated investment,” he noted.

“But we believe the market is underappreciating the strength of the underlying business and our conviction has been reinforced through engagement across the organisation, and we see clear scope for a meaningful improvement in profitability, supported by an ambitious cost programme, a well-invested asset base and a recovery in demand,” Younger said.

In Croda’s 2025 full year results, it reported encouraging early progress against its plan to grow earnings and improve returns, with a 4.4% increase in sales, 7.1% increase in adjusted earnings before interest, taxes, depreciation and amortisation (EBITDA) and 2.5% increase in EPS.

The dividend was also increased from 110p in 2024 to 111p in 2025, while free cashflow dipped slightly from £169.6m to £161.6m. The share price is up almost 5% year-to-date.

Croda International’s share price performance YTD

Source: FE Analytics