Quality investing has delivered strong long-term returns, yet the style has been out of favour as inflation, higher interest rates and political uncertainty pushed investors toward cheaper, more cyclical areas.

The more recent surge in investment in the AI value chain has further pulled capital away from quality.

These combined pressures help explain why quality struggled in 2025 – a year that proved to be the investment style’s fourth most challenging between 1990 and today, according to JP Morgan Asset Management research.

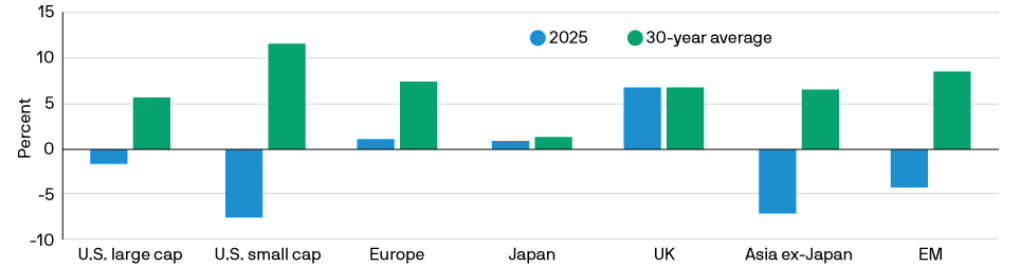

Performance of quality across regions in 2025 compared to the 30-year average

Source: JPMorgan Asset Management. Data as at 31 December 2025.

Separate data from FE Analytics indicated that the MSCI ACWI Quality index gained 10% last year, trailing Growth, Value and Momentum, with the latter topping the table with a 15.1% gain.

However, Chris Rossbach, chief investment officer and lead manager of J Stern & Co World Stars Global Equity, said pressure on quality has opened up attractive entry points.

“Right now, quality is on sale, as the headwinds of the past year or so brought on a sell-off that made these companies extremely cheap,” he said.

Specifically, he pointed to the negative impact of technological disruption as AI investment soared, a “severe consumer squeeze”, political uncertainty and the resulting rotation into value, resource-intensive and capital-intensive stocks.

“Yet, between the consumer turnaround we expect and the valuations these [quality] companies currently trade on, we think we are poised for a resurgence in quality stocks that will be as strong as the resurgence in banks, mining, energy and other capital-intensive areas.”

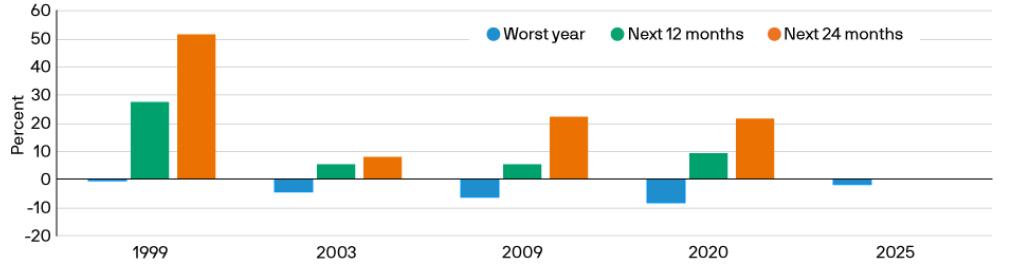

Indeed, when looking at quality’s periods of underperformance, JP Morgan Asset Management noted that these tend to be short-lived and often followed by renewed outperformance as fundamentals regain prominence.

Performance of quality during/after its worst periods in history

Source: JPMorgan Asset Management. Data as at 31 December 2025.

Rossbach noted that such shifts in sentiment “do not happen slowly” and that he thinks “it will happen soon” – by the end of this year or early 2026.

His confidence is rooted in quality’s strong track record.

MSCI’s analysis of its Sector Neutral Quality indexes said that the MSCI USA Sector Neutral Quality and World ex USA Sector Neutral Quality indexes have outperformed their respective parent indexes by 50 and 165 basis points (bps) annually since 1998, with risk also lower by 50bps and 14bps respectively.

“Profitability (as measured by return-on-equity) has been the strongest and most persistent driver of returns, while low leverage and stable earnings have moderated losses during periods of market stress,” MSCI analysts said.

During periods of heightened market volatility, MSCI USA Sector Neutral Quality and the World ex USA Sector Neutral Quality indexes also outperformed their respective benchmarks by an average of 23bps and 31bps per month, they said.

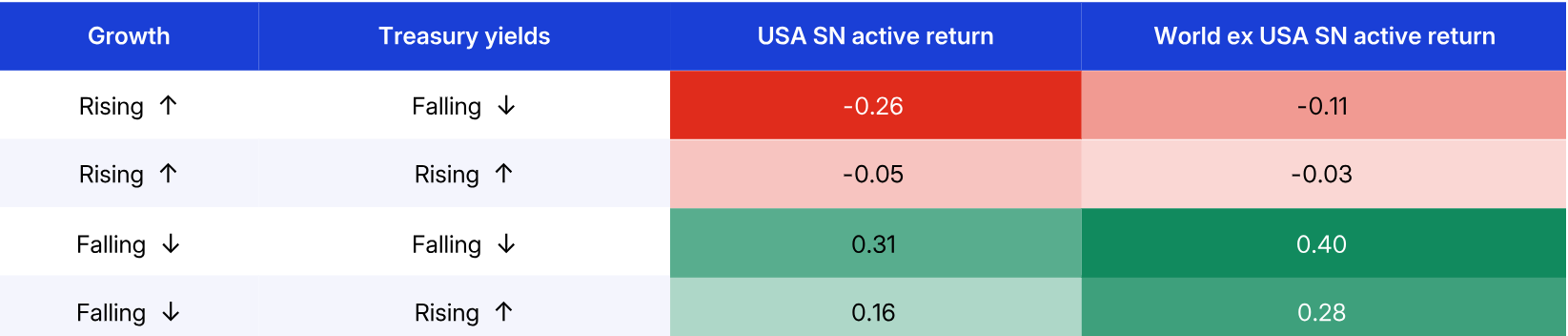

MSCI research also noted that the indexes’ relative performance is strongest when both growth and yields are in decline.

MSCI shows how quality outperforms in periods of slower growth and falling yields (USD)

Source: MSCI. January 1999 to October 2025. The table shows the active returns of the MSCI Sector Neutral Quality indexes over their respective parent indexes against 10-year US treasury yields and growth proxied by the OECD’s composite leading indicator.

Identifying quality stocks

As style leadership shifts, Rossbach said having a disciplined framework through which to assess the quality characteristics of stocks is even more important.

He said traditional markers of quality – such as stable revenues, consistent margins, solid balance sheets and strong returns on equity – remain important foundations but “only tell part of the story”.

“In a challenging environment, it is much more important to have a clear view on forward-looking quality,” Rossbach said.

“We want to invest in companies that are solving problems, not creating them; companies that are doing the disrupting, not getting disrupted.”

J Stern & Co World Stars Global Equity is tilted toward digital businesses, healthcare, consumer franchises and select industrial names, and away from “balance-sheet-driven financials like banks and regulated or resource- and capital-intensive businesses like utilities, mining and heavy manufacturing”.

He also sees “tremendous opportunity” in the technological innovation surrounding AI and the infrastructure needed to support it, highlighting German multinational software company SAP, which was added to the portfolio in November 2025.

“We bought it because we think it will be key for the application and use of data as AI applications are developed and implemented at scale in large businesses,” he said.

He pointed to the company’s deeply entrenched role in corporate data and potential for growth, with only around 50% of SAP clients currently on the cloud.

“Far fewer have data ready for AI use – so it has a long runway migrating customers to the cloud, increasing recurring revenue and enhancing the ability to use data,” he added, noting this is “only partially understood in the share price”.

Remaining patient

Although headwinds for quality – geopolitical tensions, political uncertainty and inflation – are not yet showing signs of abating, Rossbach said higher-quality companies are resilient and that “there is significant self-help within these quality companies”.

“Many are innovating, investing in advertising again, aligning their businesses, cutting costs and positioning themselves to get through constrained demand,” he said.

“When demand returns, companies will be well-positioned, leaner and more efficient. Their operating leverage will be significant, driving profitability and share price recovery.”