Almost every asset class has lost money since the start of the war in Iran, according to FE fundinfo data, with only six peer groups across both the open-ended fund and closed-ended investment trust universes making a positive return in March.

The US and Israel launched coordinated strikes on Iran on 28 February, killing supreme leader Ayatollah Ali Khamenei. Since, Iran has responded by closing the Strait of Hormuz, a shipping lane through which roughly a fifth of global oil supply passes.

Energy prices have leapt higher, causing fears that a protracted war could lead to a stagflationary scenario (where inflation remains high while economic growth weakens) for the rest of the world.

US president Donald Trump has declared victory several times over the past month, yet the war continues.

Ben Yearsley, director at Fairview Investing, said: “What felt like being a short sharp war in Iran has morphed into an attritional war. Markets have been in turmoil; benign at the end of February and since then in heightened volatility mode.

“The key question for markets is what is the end game? The answer to that is a complete unknown as Trump appears to change his mind daily. The latest post on his social media account suggests he’s not bothered whether the Strait of Hormuz re-opens or not.”

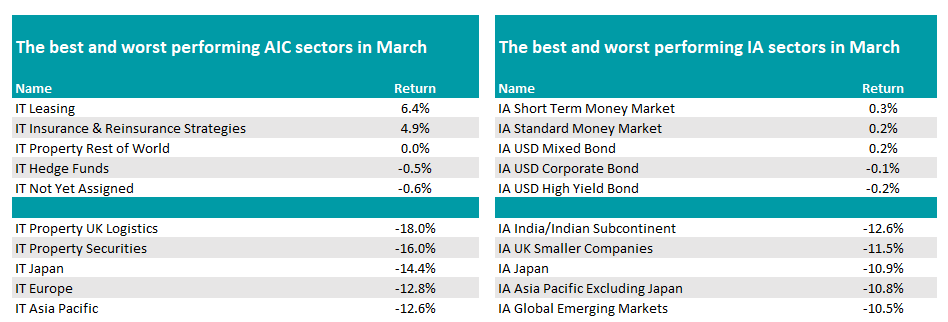

Fund investors that took shelter in money market funds were spared the worst of the falls, with the IA Short Term Money Market and IA Standard Money Market sectors two of only three peer groups to make a gain in March.

The other was the IA USD Mixed Bond sector, which was “aided by the 1.76% rise in the dollar against the pound”, said Yearsley. The remainder of the top five was also made up of US bond funds, although the IA USD Corporate Bond and IA USD High Yield Bond peer groups made shallow losses.

Investment trust fans could have found shelter in the IT Leasing or IT Insurance & Reinsurance Strategies sectors, which were up 6.4% and 4.9% respectively.

Source: FE Analytics

On the downside, India and Japan were hit hard as both markets are large oil importers, while Asia and the emerging markets also suffered for similar reasons. According to data from the International Energy Agency, 80% of all oil passing through the Strait of Hormuz is destined for Asian countries.

UK smaller companies funds were also sold off strongly last month as investors took risk off the table over the course of March. “After a bright start to 2026 [the sector] fallen away quickly,” said Yearsley.

Despite their big falls last month, Japanese, Asian and emerging market equity sectors remain towards the top of the pile over the course of 2026, having had strong starts to the year.

Yearsley said: “It’s easy to forget that we are only three months into 2026 and how strongly markets rose in the first two months of the year.”

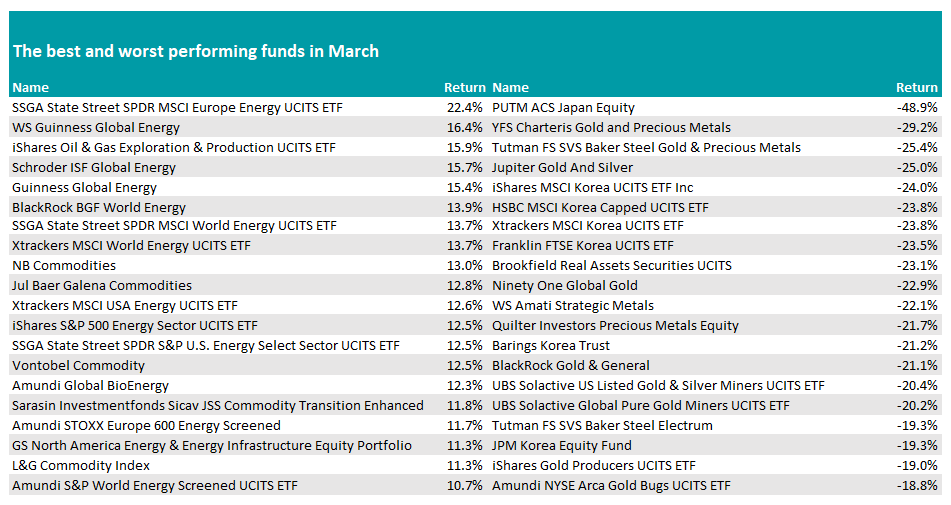

Turning to individual winners and losers, energy was the clear success story, with a barrel of Brent crude jumping to more than $100 around the middle of March and staying there for the final two weeks.

State Street SPDR MSCI Europe Energy UCITS ETF topped the performance tables, up 22.4%. All top 20 funds were energy or commodity portfolios.

“From an individual fund perspective, the energy funds well and truly delivered the goods with oil company share prices following the price of oil up,” said Yearsley. “Where there’s muck, there’s brass, or should it oil instead of muck?”

Just outside the top 20, L&G Cyber Security UCITS ETF and Polar Capital Biotechnology were the first funds to appear with no reliance on the oil price. The two funds made 7.8% and 5.4%, the 24th and 25th best returns in the Investment Association fund universe.

The cybersecurity sector rose as investors looked to the future criminal activity that could become more prevalent in the era of AI, while biotechnology funds were boosted by the asset class’ more defensive characteristics.

Source: FE Analytics

Turning to the foot of the table, gold and precious metal specialists – which have reaped the gains of a rapidly rising gold price in recent years – found themselves at the bottom of the rankings.

Despite the yellow metal’s safe-haven status, investors used the past month to take profits in assets that had been performing strongly and gold was not spared.

Investors also sold out of Korean equities, with five funds investing in the country appearing in the bottom 20 performers last month. Another large oil importer, investors moved out of the market that had made a strong start to 2026.

However, PUTM ACS Japan Equity was the worst individual performer over the month, down 48.9%.

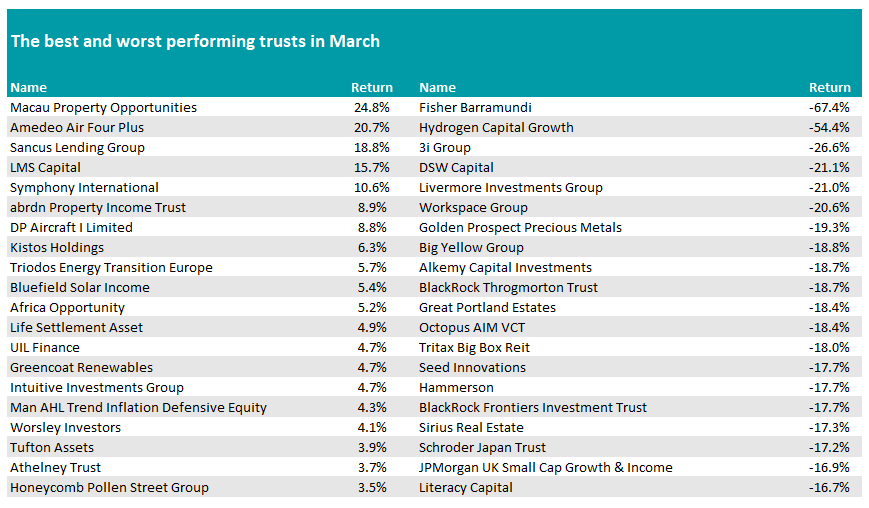

In the world of investment trusts, “it was the usual eclectic mix,” said Yearsley.

Macau Property Opportunities topped the tables with a gain of 24.8% in March, with Amedeo Air Four Plus, Sancus Lending Group, LMS Capital and Symphony International rounding out the top five. All made double-digit returns last month.

Source: FE Analytics

Conversely, Hydrogen Capital Growth, 3i Group, DSW Capital, Livermore Investments Group and Workspace Group were the worst performers, all making more than 20% losses.

Of particular note is 3i Group, the UK’s largest investment trust. Investors have grown concerned about its largest holding: Netherlands-based discount retailer Action.

The company accounts for almost three-quarters of the trust’s assets and has been a superb performer over the long term, but fears that it may have saturated its market (a November update warned of weaker sales growth in France, its largest market) had concerned investors.