Global equity-income funds do not do a good enough job at making money when times are good, according to Aviva’s Richard Saldanha, who said the peer group “hasn't done a great job of keeping pace” with rising markets in recent history.

The manager of the Aviva Global Equity Income fund would give the sector an “A star” for downside protection if he were “marking a report card”. However, there has been a lack of participation on the upside, something he said many in his peer group “struggle” with.

His goal is to do both sustainably, aiming to capture around 80% of market falls (so if the index falls 10% the fund would be down 8%) and 90% of the upside.

“When we look at the past decade, or since inception, that's been what we've done. Markets go down 10%, the fund goes down 8%. If markets go up 10%, the fund goes up 9%,” he said.

“And it’s that asymmetry that we think is attractive, where we can have a high degree of confidence we’ll protect capital, but that doesn't need to come at a huge sacrifice of upside if you construct the portfolio right.”

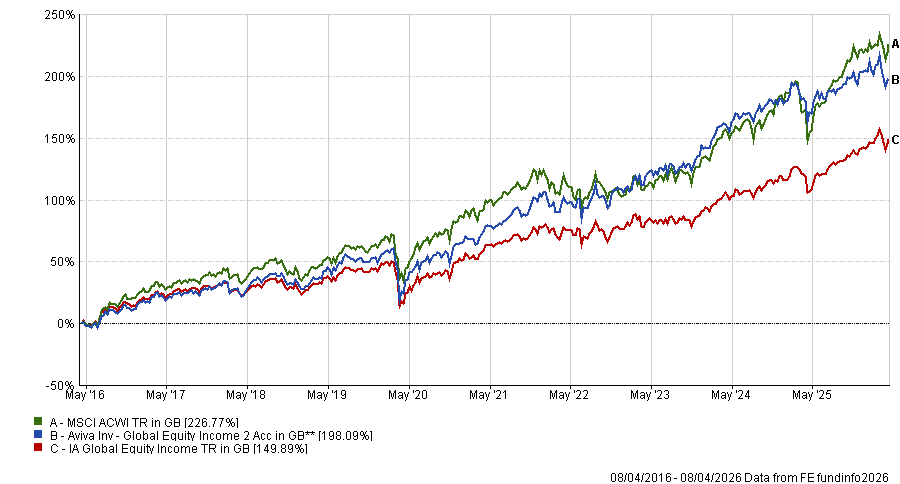

This way of thinking has netted investors strong returns, with the fund up 198% over the past 10 years, a top-quartile performance in the IA Global Equity Income sector.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

Below, Saldanha explains why his fund is overweight mature, defensive businesses and why it lags in years when commodities and banks take the lead.

What is your process?

The objective of the fund is to find companies that are paying dividends and grow them over time. We think in terms of three income buckets – or types of dividend-paying companies.

The first is mature-yielding companies. These are very mature businesses that have been around for decades, sometimes centuries, and you tend to find these in sectors like telecoms, utilities, consumer staples and pharmaceuticals. So, Colgate or Unilever, Deutsche Telekom in telecoms and Merck or Novartis in pharma, for example.

They pay quite high yields, which is attractive, but they also give us downside protection because they tend to have resilient cashflows and incomes.

Next is the ‘core yield’ or ‘cash compounders’. These are steady‑Eddie types of businesses. They grow cashflows and income at a nice, steady rate over time. Typical dividend yields are around 2-3% but they compound that income nicely over time.

Third is income growth – businesses with strong structural growth prospects. Examples include TSMC, Broadcom, Microsoft and Schneider Electric.

These often have low yields, maybe 1.5% or lower, but the income growth is very high (15-20%, sometimes 30% per annum, because they’re growing cashflows so fast).

What is your current split between the three?

Typically, we maintain something close to one‑third, one‑third, one‑third through the cycle. But we’re opportunistic – depending on value – and right now, the mature yield bucket has the highest weight at around 40% of the portfolio.

We’re seeing more value in traditionally defensive areas such as consumer staples and healthcare, which look more attractive on valuation grounds right now, relative to the income‑growth companies that have done extremely well.

When markets are very buoyant, we'll recycle a bit out of income growth and a bit more into the mature‑yielding companies that are probably less loved. In down markets, we'll go in the other direction.

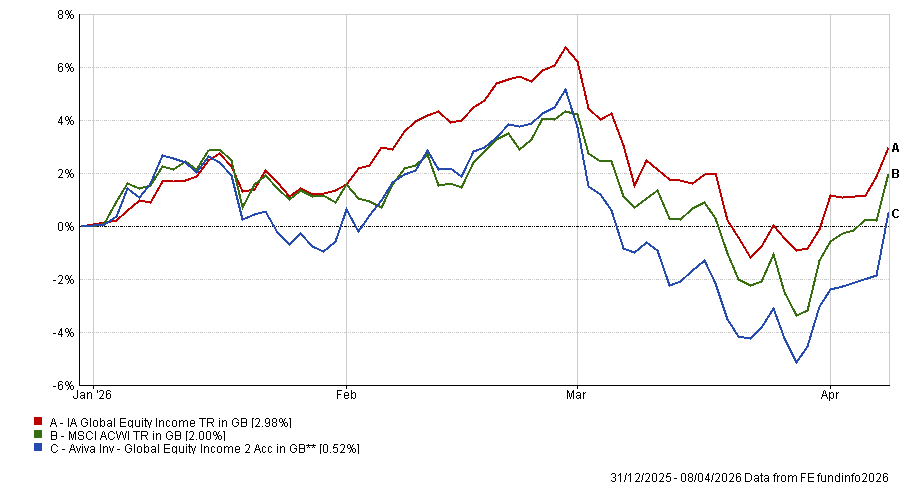

Why has the fund struggled in 2026? Has it been an underweight to energy stocks?

We do own energy majors – for example, Total – which we’ve held for a long time. The performance this year hasn’t been because of an energy underweight.

What’s been interesting is some of the more defensive sectors (e.g. some consumer staples and even some of those healthcare companies) have not actually been particularly defensive. So it's an interesting period where it’s not been what you’d typically expect in a drawdown in markets.

A lot of the consumer staples, what people would broadly define as quality growth, have not held up as well as they should have.

Performance of fund vs sector and benchmark YTD

Source: FE Analytics

Why does your fund struggle relative to the peer group in ‘value’ dominated years such as 2016 and so far in 2026?

We try to avoid companies or sectors where we think there's potential for dividend cuts so historically, the fund has never had huge exposures to commodity‑type companies, banks and real estate.

So if those parts of the value complex perform well, that’s where you’d expect this fund to lag somewhat.

What has been your best performer over the past year?

Tech. So Broadcom would be the best. The share price has almost doubled from where it was 12 months ago. We've owned it in the portfolio for a long time and it’s been a very consistent dividend payer.

That’s been tied into semiconductor companies supplying custom silicon chips to big customers like Google and Meta.

If you look at the portfolio, instead of saying ‘we think Microsoft's going to win the AI race’, we've gone for the picks and shovels.

And the worst?

The worst performer has been software, which has gone through quite a torrid time in the past 12 months. The absolute biggest underperformer for the fund is Automatic Data Processing (ADP).

The stock is down around 40% in dollar terms yet earnings estimates have actually gone up for this company. So it’s all been in the multiple.

ADP does payroll management, processing around 40 million individual worker payrolls. One in six people in the US are paid by ADP. We think the barriers to entry are high, so think ADP is relatively resilient, even though the market is obviously taking a very different view.

What do you do outside of fund management?

I’ve got a five‑year‑old son, so parenting takes up a lot of my time. But also I’m really big into watching and playing sports. I've taken up padel recently, that’s my new one. My wife has really got into it too.