The two-week US-Iran ceasefire creates conditions for gradual, selective portfolio building but the distinction between market relief and genuine resolution carries significant weight for how investors should position now, according to Stephen Dover, head of the Franklin Templeton Institute.

The ceasefire has introduced a degree of calm to markets that were in the midst of one of the sharpest geopolitical shocks in recent memory. A month after the US and Israel launched coordinated strikes on Iran on 28 February, global stocks were down more than 7% (in sterling terms).

Oil prices surged to 2022 highs after Iran closed the Strait of Hormuz and stagflation risk jumped as investors questioned if a re-run of the 1970s energy crisis could be on the cards, with central banks unable to cut rates as previously anticipated.

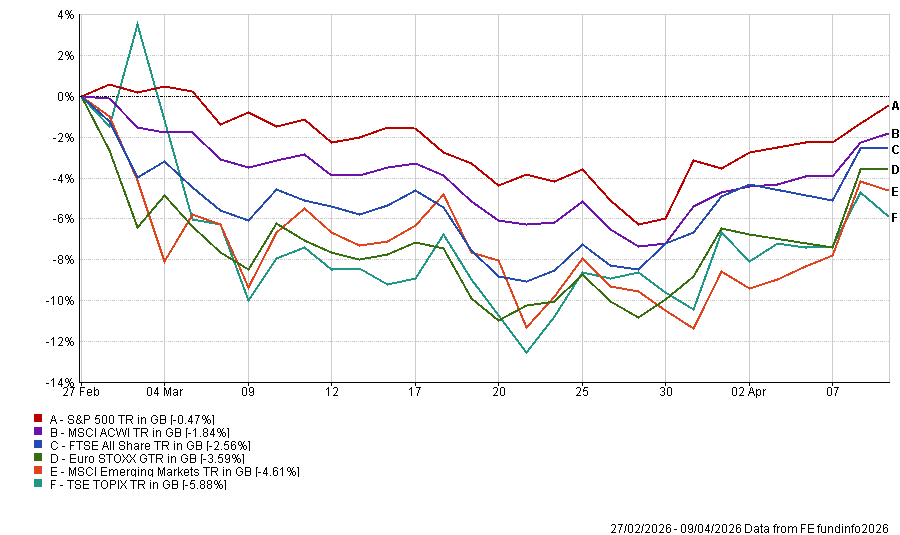

Performance of stock indices since 28 Feb 2026

Source: FE Analytics. Total return in sterling between 28 Feb and 9 Mar 2026

The ceasefire – tentative as it may be – has eased some of that pressure and markets have rallied but Dover cautioned investors against embracing it and returning to a full risk-on mindset.

“Retail investors should resist the temptation to confuse relief with resolution. In a market like this, I think the right approach is to stay constructive but disciplined,” he said.

“The optimistic case is that the market is broadening beyond a narrow set of leaders, which is healthy. But the fragility comes from the fact that a lot of the recent relief is tied to geopolitics and lower oil, and that can reverse quickly.”

The central theme in Dover’s analysis is market broadening. A rally driven by a wider set of companies, rather than a concentrated group of mega-cap technology names (the Magnificent Seven), would represent a more durable foundation for portfolios.

He identified industrials, financials and healthcare as the primary targets for selective addition on valuation and defensive grounds.

“I would add selectively to areas that benefit from broadening rather than the Mag 7, although they are clearly getting cheaper,” he said. “That means industrials and financials in particular, and selectively health care, where valuations and defensiveness can still be attractive.”

Technology retains a place in Dover’s framework. The AI and productivity investment case remains intact, he argued, but concentration in the most crowded parts of mega-cap growth warrants caution.

“Our internal work has emphasised that broadening beyond the largest names remains an important theme and that value and equal-weighted exposure can make sense when leadership starts to widen,” he added.

Dover also has a list of what to avoid, with companies holding weak balance sheets, a lack of pricing power and speculative valuations being candidates to steer clear of.

He also highlighted energy as a sector requiring careful handling despite its strategic relevance and recent gains. “Energy may still matter strategically, but after a war-driven spike in oil and then a sharp reversal, I would be careful about treating that as the core opportunity right here," he said.

The strategist also noted that lower-quality small caps often benefit in a broadening market, but he stressed the importance of “selective exposure, not a blanket rush into risk”.

Some of the sectors that performed strongly during the initial shock were responding to geopolitical conditions rather than underlying business fundamentals. Dollar-cost averaging, or adding to positions gradually and systematically rather than attempting to call precise turning points, is better suited to this environment than tactical market timing, in his view.

“Diversify, favour fundamentals and use volatility to upgrade portfolio quality rather than to make heroic calls,” he said. “That is very consistent with our broader view that disciplined dollar-cost averaging is usually better than trying to call the exact bottom or top.”

The ceasefire is far from solid, as peace talks have proved difficult and the two-week window leaves limited room for diplomatic progress. The Strait of Hormuz has not been fully reopened and Israel has continued its strikes against Lebanon, frustrating Iran’s leaders.

Any breakdown in negotiations would expose markets to a renewed shock. Dover argued that if risk escalates and the VIX – the stock market’s fear gauge – climbs above 50, this would represent “a very strong buying opportunity” rather than a signal to reduce exposure.

“Investors should stay constructive, but not complacent. I would focus less on chasing the latest relief rally and more on adding gradually to quality companies, especially in areas where market leadership is broadening beyond the mega-caps,” he summarised.

“The key is diversification, pricing power and discipline because in this environment, dollar-cost averaging usually works better than trying to time the market.”