Investors looking to buy bonds in the current climate should focus on the ‘income’ part of the term ‘fixed income’ and not concentrate too heavily on the diversification benefits often associated with the asset class.

Bonds have traditionally been viewed as the antithesis of equities – rising when stocks fall and vice versa. Yet this relationship has been put to the test in recent years.

Over three years, the MSCI World index and the Bloomberg Global Aggregate fixed income benchmark have a correlation of 0.53.

This falls to 0.39 and 0.25 over five and 10 years, respectively – not the negative numbers that would be expected from two asset classes that are supposed to move in opposite directions to one another.

Martin Coucke, co-manager of the Schroder Strategic Bond fund, said: “The diversification characteristics of bonds tend to come back when inflation goes back to close to target.

“So when inflation is about 2.5%, that’s when the inverse correlation between equities and bonds tends to come back as well.”

The issue is that since the Covid pandemic, inflation has been rampant. Supply chain constraints caused by global lockdowns had a knock-on effect that took years to address, with inflation touching 10% in many countries around the world in the early part of the 2020s.

While interest rates rose rapidly in 2022 to rectify this, inflation remains elevated today, with the latest bout of higher prices caused by a spike in oil prices following the outbreak of the war in Iran.

“We don't say the role of bonds as a diversifier is gone. It’s very much a matter of the macro environment. In an inflationary environment, you don’t see [the benefits],” he said.

At present, markets are under the assumption that the current bout of inflation will be transitory, he noted, with prices remaining higher over the next few months until the Strait of Hormuz, an important waterway for oil and gas transportation that was closed at the start of the war, reopens.

“If that’s the case – and we go back to a relatively unconstrained environment for global energy supply – then I think bonds should work quite decently as a diversifier again,” he said.

However, that does not mean the case for owning bonds has gone out of the window right now – investors should buy bonds for the income. “We call it fixed income for a reason,” said Coucke.

The yield paid on the date of purchase – whether it be an individual bond or a fund like his own – is the return investors should expect over the lifetime of the investment.

“I think that's what matters the most. In theory, you should realise the yield that you're buying into over the life of your investment with relatively high certainty,” he said.

“So I think that’s the appeal – the pretty attractive yield that you're getting into and the relatively high chances of realising this yield over several years.”

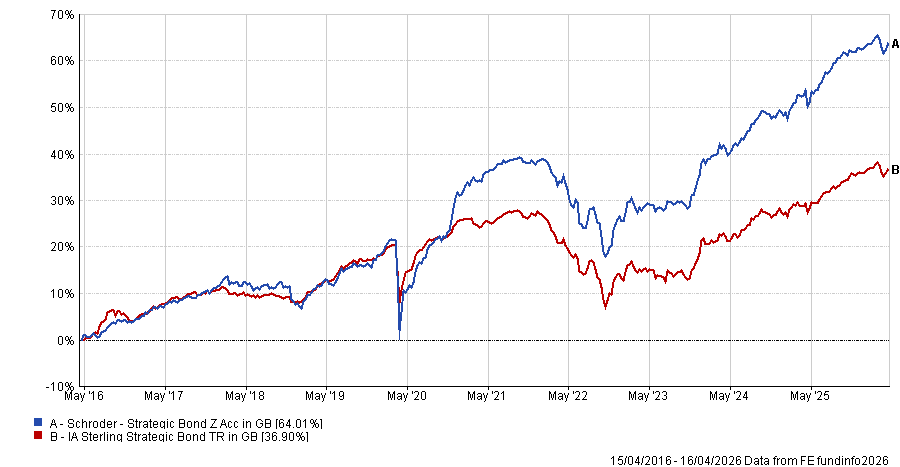

The Schroder Strategic Bond fund has been the third-best performer in the IA Sterling Strategic Bond sector over the past decade and has made top-quartile returns over one, three and five years. It currently offers investors a 5.68% yield.

Performance of fund vs sector over 10yrs

Source: FE Analytics

“That's always been the appeal for fixed income – the certainty regarding the income that you are getting, which you can't say about equities,” said Coucke.

“So forget the day‑to‑day correlation. I think over the next one or two years, the carry will mostly dominate the return over capital appreciation, which is more driven by the daily moves of interest rates. And that's the appeal to me.”

Last week, the manager told Trustnet why the fund has little exposure to investment-grade bonds, focusing more on a barbell approach between high-quality, short-dated debt such as government bonds, and more risky high yield and private credit markets.