The biggest challenge facing funds-of-funds is not identifying good stock pickers but portfolio construction, according to Lisa Wang, senior vice president and head of EMEA investment strategy at Franklin Templeton Investment Solutions.

Wang, whose team builds multi-asset portfolios using both internal and third-party funds, said the fund-of-funds model creates structural problems that are difficult to resolve.

“When you're putting different active managers together, one of two things can happen, both equally frustrating,” she said.

“You can either double down on certain exposures, because many of them are actually in the same names and before you know it your portfolio is so much based on that idea; or, if you try to allocate to managers with really diversified views, you end up with a benchmark portfolio but now you've paid active fees for what is really very similar to a benchmark.”

The problem stems from the fact that active managers come as they come; investors can't choose just the elements they like. To Wang, that's “one of the biggest challenges”.

Even when an active manager has genuine stock-picking skill, other portfolio decisions can overwhelm it. For example, an overweight position in a good company may not come through in the overall performance because of certain portfolio construction decisions or poor market timing.

Wang is particularly disappointed by managers who claim to be bottom-up stock pickers but then overlay top-down macro calls, usually when they think they should be underweight beta or over- or underweight a sector.

“If they made the wrong call, that one wrong call completely overcomes the idiosyncratic stock-picking performance," she said.

Portfolio construction within active funds can also create unintended exposures, Wang continued, if manager is too enamoured with their bottom-up perspective that they lose perspective on the broader picture.

This can cause unconscious tilts towards certain sectors, countries or style factors and end up with unintended exposures in the portfolio, making it difficult to control risk at the fund-of-funds level.

The alternative – using passive funds as the core of a portfolio – brings its own problems.

"Historically when you think about the core-satellite approach, you're going to put a bunch into passives as your core, but your passives are not going to earn anything for you – they're going to be a perpetual fee drag even though they're cheap," Wang said.

This leaves portfolio constructors wanting exposure to fundamental stock-picking skill but without the baggage of unintended tilts or poor timing decisions.

Wang believes the active versus passive debate has become unhelpful, with investors taking entrenched positions when the answer likely lies somewhere in between. The real issue is how best to deploy a limited budget, both in terms of fees and active risk.

"You have a limited risk budget versus the benchmark, a limited active risk budget and limited fees or expenses that you can incorporate into the portfolio," Wang said. "What is the best balance to drive returns?"

While studies show most active managers underperform over the long term, those in the upper quartile do deliver outperformance consistently, Wang noted. The challenge is identifying those managers while managing cost and risk exposure.

"It's about selecting the right manager, but at what price?" she said. "You want to make sure that in your core you're not using up any of that price or risk that you could use for the really, really good manager that you may want to pay the additional risk and price for."

Franklin Templeton has been expanding its Core Enhanced Equity suite, originally launched in October 2025 and designed to address these structural problems.

The approach isolates fundamental stock-picking skill from portfolio construction decisions by using a systematic multi-factor framework that scores stocks across quality, value, sentiment and alternative factors, then overlays a ‘conviction factor’ derived from analysing the holdings of active managers with proven stock-picking skill.

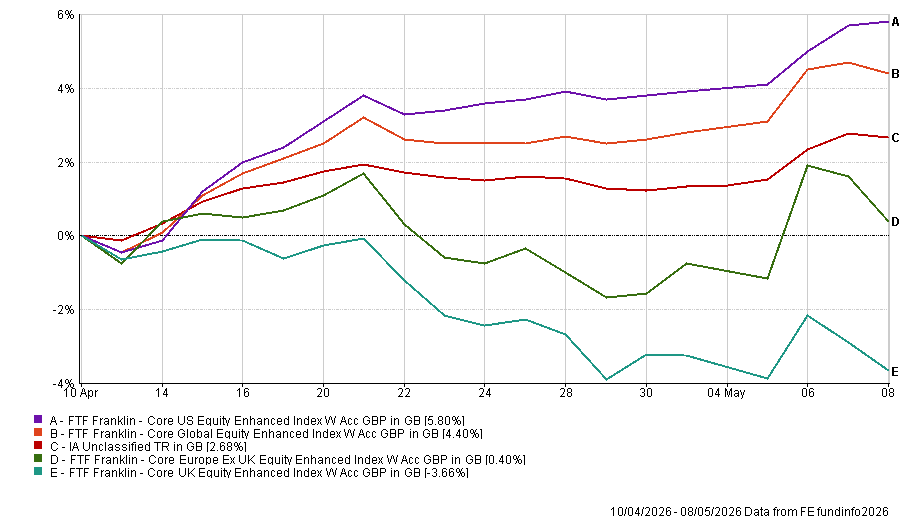

Performance of funds against sector since beginning of data

Source: FE Analytics

The strategies aim to extract only the stock selection component while neutralising unintended sector, country or factor tilts, delivering what Wang describes as sitting "right in between passive and active" – the core working harder than a passive tracker without the full cost and volatility of concentrated active bets.