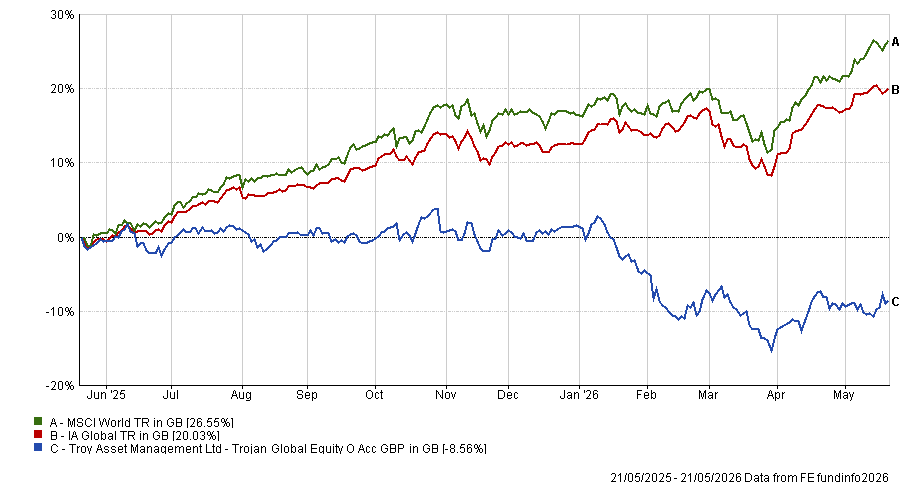

Troy Trojan Global Equity has had one of the worst years in its history. The fund lost 9.4% over the 12 months to the end of April, against a sector average return of 19.5% – a gap of nearly 29 percentage points that ranks it 559th out of 571 funds in the IA Global sector.

George Viney, who manages the fund alongside Gabrielle Boyle, says the underperformance is real, painful and, in his view, temporary.

"We have gone down when the market has gone up. That's very unusual in the history of the fund, very unusual in the course of Gabrielle’s 35-plus years of managing money in this way," he said.

"We're quite bruised by what we've experienced in the past 12 months – it’s not what we had anticipated – but if you think about the future opportunity again on a five-to-seven-year view, you can own these compounding, high-quality companies at less than a market multiple, and that looks appealing.”

Performance of fund against index and sector over 1yr

Source: FE Analytics

The explanation, according to Viney, is that the market has decided several of the companies they back are at existential risk from artificial intelligence, and has priced them accordingly.

Many of the fund's holdings are digital businesses whose share prices have fallen sharply on fears that AI will erode their competitive advantage. For Viney, those fears are wrong – or at least overstated.

An example he made was Experian, a credit data business the fund has held since 2006. Experian's database is fed by more than 1,000 US banks, updated with 1.1 billion new data points a month, and underpins credit, fraud and identity decisions across the country.

That data, Viney said, does not exist on the open web, is highly regulated and cannot be replicated by a new entrant armed with AI. If anything, a proprietary data set of that scale becomes more valuable as AI spreads, because large language models are only as useful as what feeds them.

"The models are only as good as the feedstock that informs their outputs," he said. "The complements to any large language model or AI environment become more valuable as the cost of serving or delivering those goes down."

A similar argument has been made last week on Trustnet by Nick Train, who also owns Experian.

The Troy fund also spans consumer staples, healthcare, business services and technology – companies that are deploying AI internally and building it into new products, Viney noted.

The market, in his view, is crediting the disruptors and ignoring the incumbents. He therefore hopes his holdings will go through what Google parent Alphabet has achieved: widely treated as an AI casualty and valued below a market multiple 12 months ago, it has demonstrated since then it can monetise its infrastructure and application layer in ways investors had underestimated.

However, the fund has not been static through the sell-off. Viney trimmed Alphabet after it grew to breach the fund's internal 8% single-stock limit and reduced Swiss healthcare multinational Roche on valuation grounds.

Fintech PayPal was sold after disappointing the team's expectations and the proceeds were redeployed into holdings that had de-rated: Experian, Relx, and a new position in Amazon, initiated in the fourth quarter of last year.

Amazon's appeal, Viney explained, is its AWS cloud business, which he described as "a natural opportunity for them to upsell and cross-sell a multitude of different services to that customer base”.

Its warehouse robotics operation, which is “the biggest fleet of robots in the Western world”, also gives the company an internal AI opportunity that he said the market had consistently underpriced.

What the fund has not bought is semiconductors or AI hardware, as the picks-and-shovels trade is not a long-term one, with the economics of a capital expenditure cycle tending to attract competition and eventually reverse.

“Over the longer-term time horizon we tend to take, it's very hard to have confidence about the durability of the economics of those companies.”

Instead the fund holds the hyperscalers – Google, Microsoft, Meta and now Amazon – on the premise that their infrastructure and application businesses will generate recurring, compounding demand.

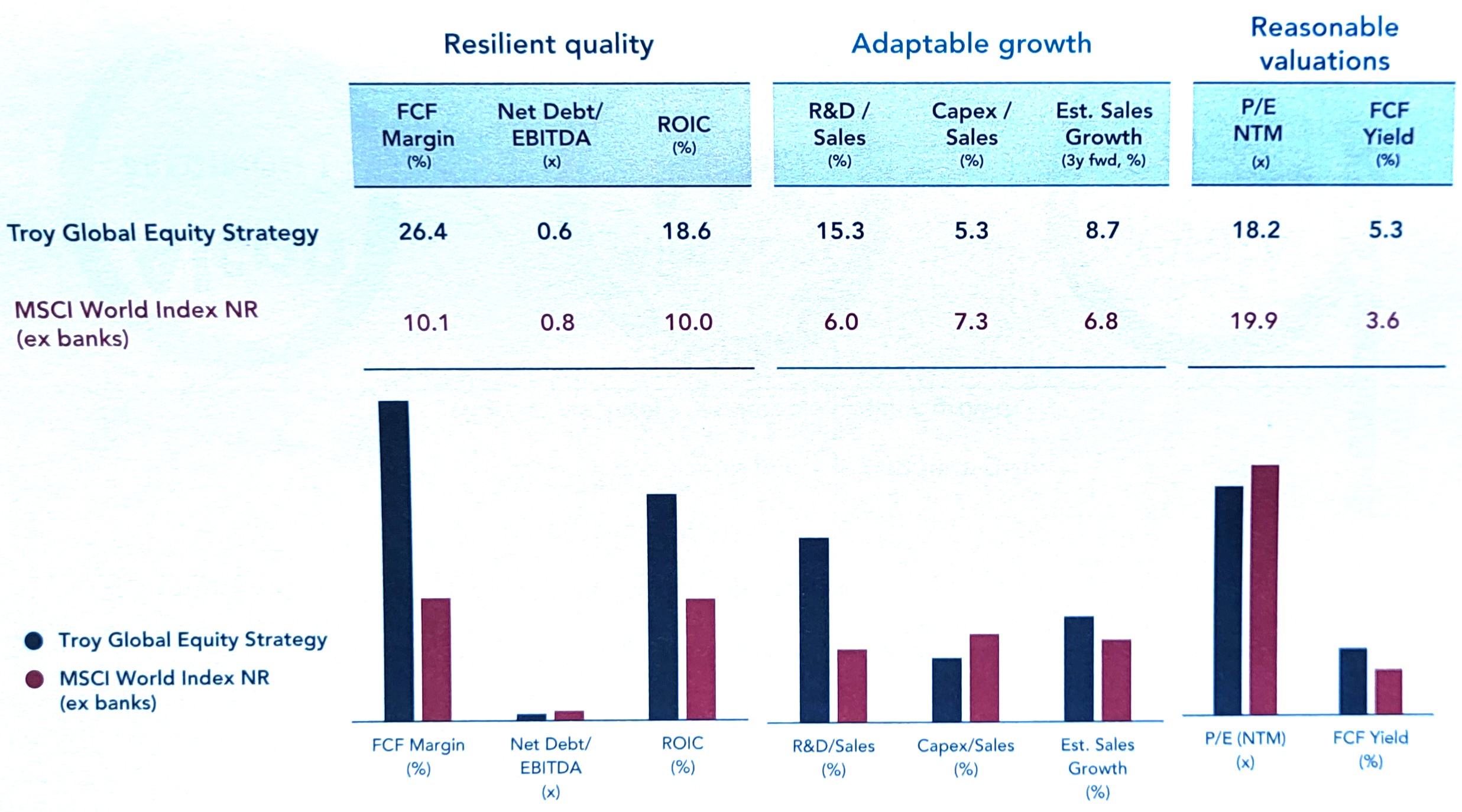

The fund's portfolio trades at around 18x earnings against roughly 20x for the MSCI World, and Viney said the free cashflow yield gap between the fund and the broader market is as wide as it has been in a decade.

Troy Global equity index comparison

Source: Troy Asset Management

The operating metrics of the underlying businesses, he argued, have continued to improve: cash margins are high, leverage is low and return on invested capital is well above the index average. The discount, in his view, is a function of sentiment, not fundamentals.

Whether investors share that confidence is another matter. The fund has £390.1m in assets and an ongoing charge of 0.86%. It has returned 25.8% over five years against 50% for the IA Global sector, while over 10 years the gap is wider at 41 percentage points (154% of the fund versus 195% of the average peer).

In calendar years, 2018 and 2023 stood out as particularly positive (with first-quartile returns of 1.1% and 23.9%), while underperformance is concentrated in 2016 (19.3% versus 23.3%) and from 2025 to today.

The managers have responded by buying the fund themselves. "We've been personally buying more of it and at a faster rate and greater amounts than we have in a long time," Viney concluded.