UK income funds have beaten their more generalist peers consistently over the past half a decade but investors should not default to an income portfolio necessarily, according to fund pickers.

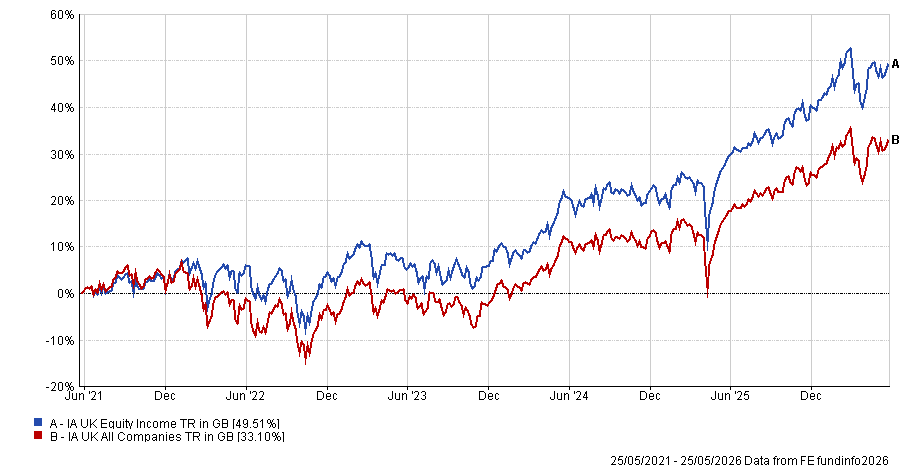

In the past five years the average fund in the IA UK Equity Income sector is up 49.6%, while the average peer in the IA UK All Companies sector is up 33%.

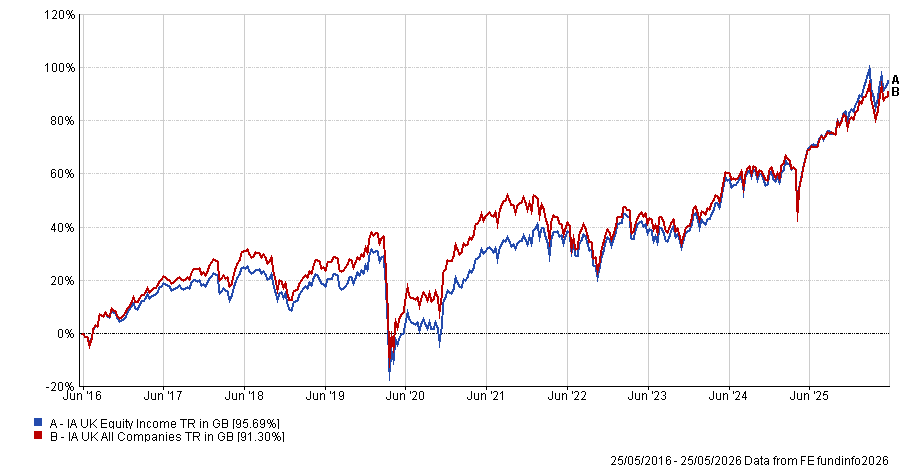

This strong run means income funds are now also ahead over a full 10 years (95.3% versus 90.8%).

Performance of sectors over 5yrs

Source: FE Analytics

Ross McKnight, senior investment analyst at City Asset Management, said much of this outperformance is because value has been the best-performing factor in the UK over the past five years.

“Income funds have been more geared into this [trend] versus the IA All Companies sector,” he said, as they often have a higher average weighting to financials.

“In some cases, banks have gone up fivefold, which has been a key driver of performance. Additionally, lower exposure to quality and sectors such as healthcare has also been accretive,” said McKnight.

Indeed, over the past half a decade, the value style has made almost three times the returns of growth strategies and four times more than quality counterparts, as the below chart shows.

Performance of indices over 10yrs

Source: FE Analytics

Simon Evan-Cook, manager of the Downing Fox multi-asset range, agreed that the value bias has helped specialist income portfolios as these “tend to sit more closely with the value style of investing”.

“In part this is because of ‘yield discipline’ – the dividend yields on stocks that have risen in price fall as they do, which encourages income investors to move on to a higher-yielding stock, whereas non-income investors don’t face that pressure,” he said.

Additionally, some of the biggest dividend payers in the market are oil companies BP and Shell, so a lot of income funds naturally have higher exposure. A recent Trustnet study found that more than half of funds in the IA UK Equity Income sector counted Shell among their 10 largest positions, while 43.1% held BP in their top 10.

Should investors buy income funds?

Although income funds have been the best way to invest on average over the past five years, this does not mean investors are necessarily better off investing purely for dividends.

Sheridan Admans, founder of Infundly, said: “I would not say income is automatically the best way to invest in the UK. The broader UK market still looks under-owned and attractively valued versus global peers, so the opportunity may now extend beyond dividend-paying companies.”

This was echoed by Evan-Cook, who noted that “in theory” a dedicated non-income investor with a “proper valuation discipline” has more options to pick from than an income-constrained manager, meaning some of the best managers “should still sit in the IA UK All Companies sector”.

Over the past five years, Artemis SmartGARP UK Equity – in the All Companies sector – has been the best-performing UK fund. Three of the top five funds from among both sectors come from the broader peer group, although the top 10 is dominated by income specialists.

An income fund is a good “each-way bet”, said Evan-Cook. Although it may get left behind in “racy markets”, a yield discipline can help to avoid the worst market falls.

How do the experts invest?

McKnight said he doesn’t currently own a UK equity income fund, preferring to have a balance between a FTSE 100 tracker and an active multi-cap portfolio. In particular, he said the tracker is “set up well given the current macro backdrop”.

Admans also suggested pairing a tracker with an active fund but used the Vanguard FTSE UK Equity Income Index for his passive allocation. The £2.2bn portfolio has been the best performer in the IA UK Equity Income sector over the past five years, with large allocations to financial, consumer staples and energy stocks (BP is its largest holding with Shell also in the top five).

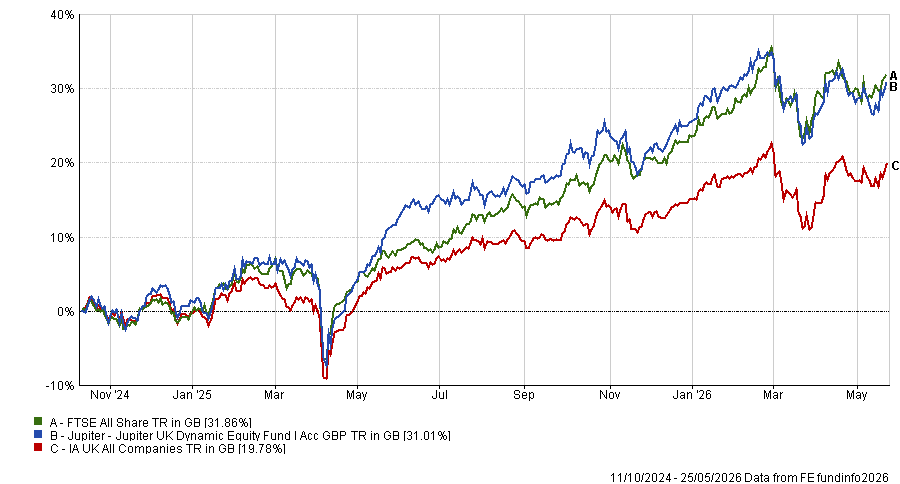

To complement this, he went for Jupiter UK Dynamic Equity, managed by FE fundinfo Alpha Manager Alex Savvides. He moved from JO Hambro Capital Management (JOHCM), taking over the Jupiter Special Situations fund, which was formerly run by Ben Whitmore, changing the name of the fund and the investment style.

In charge since 2024, Savvides “adds active stock selection and targets undervalued companies where restructuring, management change, balance-sheet improvement or better capital allocation can unlock value,” said Admans.

Under his tenure, the fund is up 31%, a second-quartile effort in the IA UK All Companies sector, although almost 12 percentage points ahead of the average peer.

Performance of fund vs sector and benchmark since manager start

Source: FE Analytics

Evan-Cook, meanwhile, highlighted Premier Miton UK Value Opportunities, which has been run by Matthew Tillett since 2022.

“It’s a go-anywhere fund and, having held a decent weight in many of those income-producing large-caps a few years back, the manager has since moved onto where he thinks the best opportunities lie, which means he has more exposure to small-caps than you’d find in most UK equity income funds currently,” Evan-Cook said.

“This has put a lid on his returns in recent years, as the market only has eyes for its largest companies, but this has only added to its potential to outperform from these levels.”