Equity markets are making a serious misjudgement about Iran, according to Troy’s Charlotte Yonge, who alongside co-manager Sebastian Lyon, have positioned their £5bn Trojan fund accordingly.

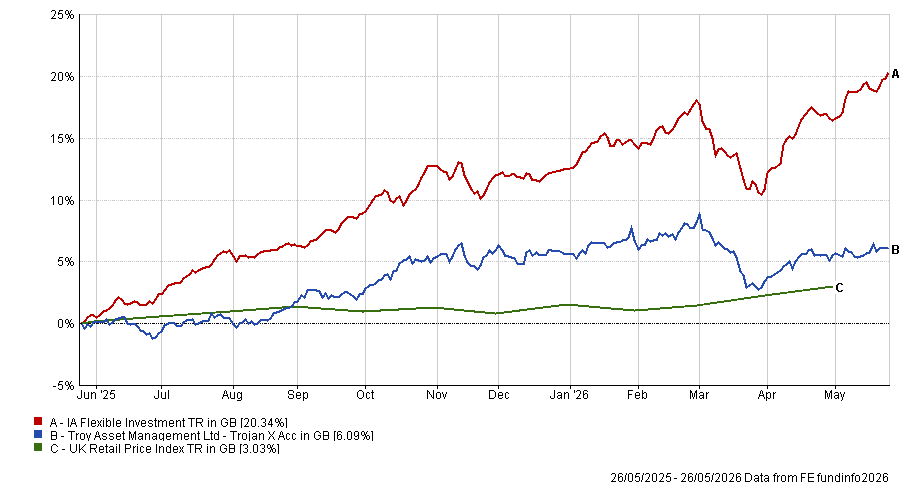

With equities at 36% of the portfolio, below the 20-year average of 42%, the fund has trailed the market in recent times – it returned 6.2% over the year to end-April, ranking 170th out of 176 in the IA Flexible Investment sector, and 24.5% over five years against the 34.7% sector average.

But despite the missed rally, the managers aren’t leaving caution behind.

Below, Yonge argues that the Strait of Hormuz standoff is being priced as a non-event, draws a direct parallel with the 1973 oil embargo and explains why she is still buying companies framed as losers, such as Adobe and Experian.

Performance of fund against index and sector over 1yr

Source: FE Analytics

What is your investment philosophy and process?

The mandate was set up originally to look after one family’s wealth. The aim is to protect capital but also to grow it.

There will be periods where we fall but the aim is to fall much less than the market. In the financial crisis, our largest ever drawdown was less than 14% when the market fell by more than half. In Covid, the market dropped by a third and we fell less than 10%.

We invest across four asset classes: equities, bonds, gold and cash. We lean into risk when valuations are cheap and lean back when we think the risks of a 2008 or Covid-style period are on the horizon. We try to go into difficult periods with greater resilience than everyone else, so that when people are panic selling, we can buy.

Why are you below your average equity allocation right now – and what are the risks you're watching?

We’re currently at 36% in stocks relative to an average of 42% over the past 20 years, a high of 72% and a low of 22%. We’re below average because we think equity markets are vulnerable and there are very clear risks that we don’t think are discounted.

Iran is the most immediate. The market is essentially saying it’s a non-event, making new highs, assuming Donald Trump is in control and that the Iranians will capitulate. Experts we speak to say Iran can survive anywhere from 100 to 300 more days without the Strait being open. The market is pricing in an outcome that assumes a great deal.

How worried are you about the conflict?

We don’t make precise probabilistic forecasts. We look at what’s priced in versus the risk. The probability of recession in stock markets is virtually zero. We think it’s a non-zero probability and increasing by the day.

The Yom Kippur War and the 1973 oil embargo took over six months to be fully reflected in equity markets. The S&P [500] fell 20% while the embargo was in force, then fell a further third after it was lifted.

The knock-on from reduced oil supply takes time to hit demand and the real economy. We don’t know if there will be a recession but the longer this lasts, the more likely one becomes. If we get to August or September without a resumption of oil supply, there’s a very real chance of a recession.

What is the AI risk you see in markets?

The top 10% of stocks by market cap now comprise the highest share of total market cap ever recorded, and it’s almost all AI-related. If the hyperscalers spend $600bn rather than $700bn this year, the semiconductor stocks really suffer.

Over half of US growth has been driven by AI capex. That creates a dual vulnerability – in markets and in the economy.

What were your best calls over the past 12 months?

We made an aggressive addition to equities in April and May of last year. We started 2025 with under 30% in equities and on the Monday after Liberation Day we added five percentage points in a single day. We continued buying through the summer to reach the low 40s.

Alphabet, which we already owned, was $145 that day. It’s now just under $400. We also added Hubble, a manufacturer of electric grid equipment in the US, in May last year. That’s done very well.

And the worst?

The mistakes have been Experian and Adobe. Both have been re-rated by the market on the assumption that AI will impair their businesses. Adobe’s earnings multiple has gone from 20x to just over 10x, Experian’s has gone from the mid-20s to around 16x.

Adobe is less than 1% of the fund; Experian is just under 1.5%. Cumulatively they’ve detracted less than a per cent.

Both continue to operate well. Experian is a credit bureau with highly regulated, proprietary data sets you can’t replicate with an LLM [large language model]. Adobe has an 80% share of the digital creative marketing business, is deeply embedded in professional workflows, and is incorporating AI within its own ecosystem.

The market has already decided these businesses are impaired. We think there’s a good chance that’s wrong. We’ve held and we’ve added.

What do you do outside of fund management?

I have two young children, so they take up a lot of fun time at home. I’m quite sporty, I love running, cycling and swimming. It helps me think.