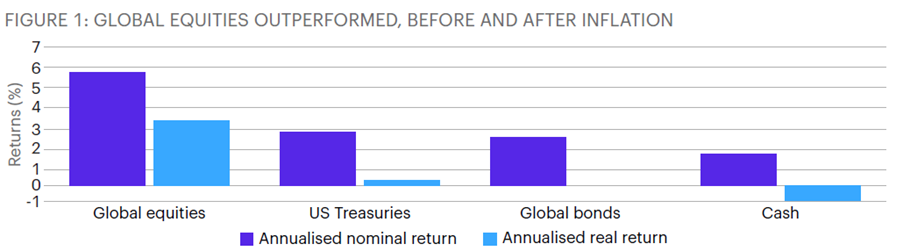

Global equities have provided access to long-term economic growth, technological innovation and productivity gains whilst offering a natural hedge against inflation over time.

Over the past 20 years, global equities have returned 6.1% per annum on a nominal basis, significantly outperforming global bonds, US treasuries and cash. When adjusted for inflation, the relative advantage of equities becomes even more pronounced.

We believe the question for investors is not whether to allocate to global equities but how best to construct the exposure to meet individual objectives and risk tolerance.

Source: Allspring

Active versus passive: The perennial debate

Whilst there are strong views on both sides of this well-worn debate, the sensible conclusion for investors is an ‘and’ rather than an ‘or’. An efficient and effective global equity portfolio can be constructed by blending low-cost market exposure (beta) with skilled active management (alpha).

For example, blending an actively managed global equity strategy with a passive exchange-traded fund allows investors to seek added return without abandoning the benefits of low-cost market exposure.

Depending on their risk appetite, return objectives and fee budget, allocations can be scaled to help to meet the desired outcomes.

Over the past decade, passive investments have garnered hundreds of billions of dollars from investors seeking low-cost, broad market exposure. Considering the prolonged period of disappointing returns from active managers, driven by exceptionally loose monetary policy, abundant liquidity and periods when fundamentals appeared disconnected from market prices, it is unsurprising that passive investing has grown to its current scale.

However, these substantial flows into passive strategies have also resulted in historically high levels of concentration in the largest stocks within major indices. The risk is that, should flows reverse, selling pressure may also become concentrated, potentially exacerbating market drawdowns.

We see investors increasingly exploring alternative ways to build their core portfolio exposures. Whilst concentration remains a risk, markets have started to show signs of improving breadth and a renewed focus on company fundamentals.

This may indicate a more normal market environment in which active management can once again show its true value – delivering alpha.

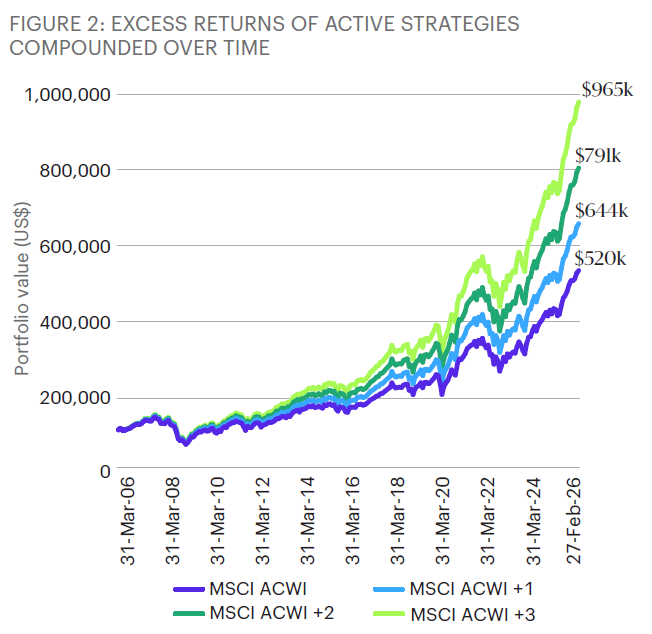

Excess return, or alpha, is powerful over the long term and is especially valuable when overall market returns are expected to be lower. The following graph compares a portfolio of $100,000 invested in the MSCI All Country World Index (ACWI) over the past 20 years with three hypothetical investment strategies that generated 1%, 2% or 3% of excess returns annually.

This straightforward example provides a clear reminder of the powerful impact that even modest levels of alpha can have on long-term capital growth.

Source: Allspring

Systematically capturing alpha

Investors seeking to generate alpha choose among fundamentally driven and systematic investment approaches. Systematic investing harnesses large datasets – with advanced technology and investment innovation combined with experienced human oversight – aiming to build disciplined and repeatable portfolios.

A key advantage of systematic investing is the ability to assess every company within an investment universe against a variety of metrics on a daily basis, from traditional measures such as profitability, valuation and return on equity to other factors such as sentiment, revisions and momentum.

Companies can also be efficiently assessed through multiple lenses, by traditional categories such as geography and sector as well as the stage of their life cycle and overall business maturity.

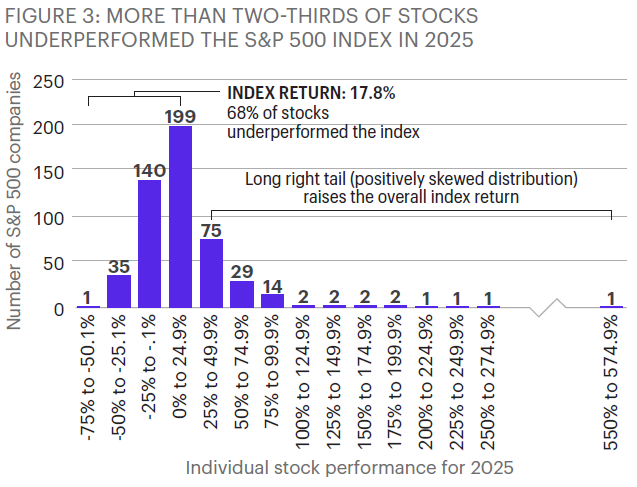

Why is this important? Research shows long-term equity wealth creation has been driven by a relatively small number of stocks – many listed companies failed to outperform the market.

The chart below shows 68% of stocks in the S&P 500 Index underperformed the index return in 2025. Index performance can mask significant dispersion at the stock level, whereas systematic strategies can assess the entire market, aiming to identify long-term winners whilst avoiding persistent underperformers.

Whilst systematic investing is grounded in fundamental principles, incorporating a final stage of human validation helps address the challenge that no model can pick up every material data point all of the time.

For example, a purely systematic process may guide you towards a company whose CEO just resigned or to a company that’s experienced a stock-specific event that could materially impact future performance.

We believe this combination of scale, advanced technology and experienced judgement allows systematic investing to stand out as a robust approach to capturing sustainable alpha.

Source: Allspring

Sophie Scott is a systematic core equity specialist on the Allspring Global Equity Enhanced Income fund. The views expressed above should not be taken as investment advice.