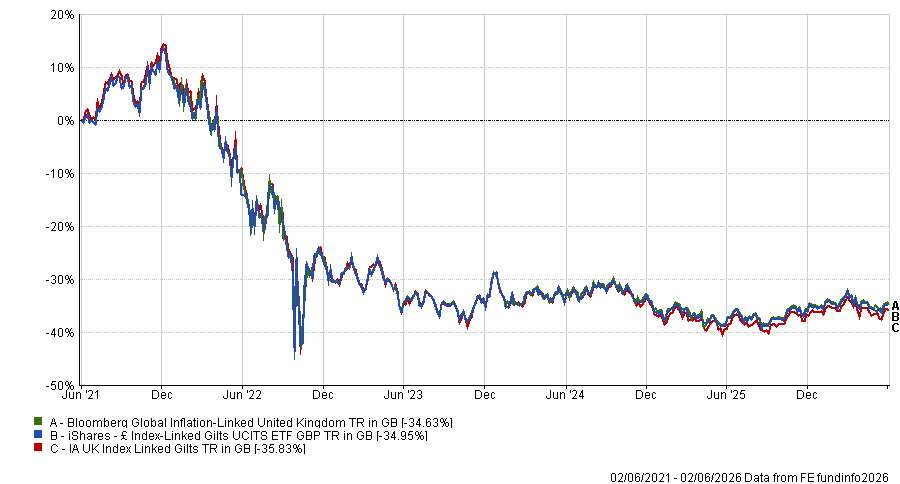

Investors who bought an index-linked gilt fund five years ago hoping they would serve as an inflation hedge have been left disappointed. Over this time the average fund in the IA UK Index-Linked Gilt sector is down 36%, with the best performer losing 30.9%.

It could have been worse if investors bought at exactly the wrong time. If they did so at the end of 2021, by the end of 2025 they would have almost halved their money.

Yet some fixed-income specialists still back them as a viable instrument – provided that investors understand duration and buy the right part of the market.

Index-linked gilts (“linkers”) are UK government bonds where the income rises in line with inflation. Unlike conventional gilts, which pay a fixed coupon, linkers adjust both the coupon and the face value in line with the Retail Prices Index (RPI) (replaced by the Consumer Prices Index (CPI) from 2030, due to recent reforms).

That inflation-protection is a huge attraction in eras when prices rise, but the asset class is much more complicated than assuming these bonds will do well when inflation increases.

Take the iShares GBP Index Linked Gilts ETF – a widely held exchange-traded fund among retail investors – which has a duration of around 14 years. This means it is highly sensitive to changes in long-term real interest rates.

When real rates rose sharply in 2022 and 2023, the ETF fell by roughly half. Today, it has partially recovered but remains down about 35% in total-return terms, as the below chart shows.

Performance of fund against index and sector over 5yrs

Source: FE Analytics

Investors who therefore assumed they were buying protection against rising prices ended up, inadvertently, with a large bet on real rates falling.

As Trustnet reported earlier this year, gilts have been losing investors money for a number of years now, particularly these index-linked bonds. But has a reset in valuations now made them worth revisiting?

The case for

Real yields on index-linked gilts – the return investors receive above inflation – turned positive in 2022 for the first time in years.

Emma Moriarty, portfolio manager at CG Asset Management, says she remains firmly committed to linkers as a core portfolio holding. The Capital Gearing trust, which she works on, has its entire fixed-income allocation in index-linked bonds, with around 45% of the total portfolio in linkers, split roughly 20% in UK index-linked gilts and 25% in US treasury inflation-protected securities (TIPS), which are the American equivalent.

“If you look at our core index-linked markets – the US and UK – index-linked bonds have outperformed nominal government bonds since the turn of the century. The reason for this is that markets systematically underestimate realised inflation,” she said.

The 10-year index-linked gilt currently yields 1.62% in real terms, which Moriarty says looks attractive against the economy's long-run trend rate of growth.

Juliet Schooling Latter, research director at Chelsea Financial Services, agreed that the entry point is better now than it has been in years and so did Richard Carter, head of fixed interest research at Quilter Cheviot, who stressed that linkers offer “some protection against spikes in inflation”.

The case against

The rehabilitation of linkers as an asset class comes with important caveats, the biggest of which is duration.

Carter pointed out that the all-maturity index has a duration roughly double that of investment-grade corporate bonds.

“If bond markets keep selling off, be that due to UK domestic political problems or otherwise, then linkers could suffer further,” he said.

Moriarty agreed. While the 10-year gilt yields 1.62% in real terms, CG Asset Management has positioned its own portfolios shorter than the index due to concerns about the long end of the UK gilt curve.

Two factors are weighing on longer-dated gilts: continued supply pressure from debt-funded government spending and reduced demand from defined benefit (DB) pension schemes.

The latter were the largest structural buyers of long-duration linkers but have significantly wound down their activity following the liability-driven investment crisis of 2022, when the Truss government's mini-Budget triggered a gilt sell-off so severe that leveraged pension fund strategies faced margin calls overnight, prompting a Bank of England intervention and a subsequent industry-wide reduction in long-duration gilt exposure.

There is also the RPI-to-CPI switch to contend with. From 2030, the inflation index underpinning linkers will shift from RPI to CPI. Since RPI has historically run 0.5% to 0.8% above CPI, the inflation compensation going forward will be lower than in the past.

Carter noted the change is "well understood by market participants" and Moriarty said her modelling suggests the curve around 2030 reflects rational pricing. But for new buyers it reduces the expected compensation from holding longer-dated instruments.

Schooling Latter flagged a further complication in the middle of the curve.

“The 20-year area is arguably the most attractively valued part of the curve,” she said, “but this is a consideration for investors prepared to take on significant duration risk, rather than those simply seeking an inflation hedge.”

What investors should actually do

If retail investors want genuine inflation protection from linkers, shorter-dated instruments would be a more appropriate route.

Carter recommended one-to-10-year index-linked gilts for investors primarily seeking protection against inflation spikes rather than a long-duration rates view.

Moriarty made the same distinction, noting that the problem with broad ETFs like the iShares fund above is that investors buying them were making a long-duration bet they may not have understood, which is precisely why CG Asset Management launched the CG UK Index-Linked Bond fund with a duration of around five years.

Schooling Latter also pointed to the iShares Up to 10 Year Index-Linked Gilt fund as a more conservative option for retail investors, while noting that the iShares vehicle remains appropriate for those willing to take on duration risk at what is now a more favourable starting point.

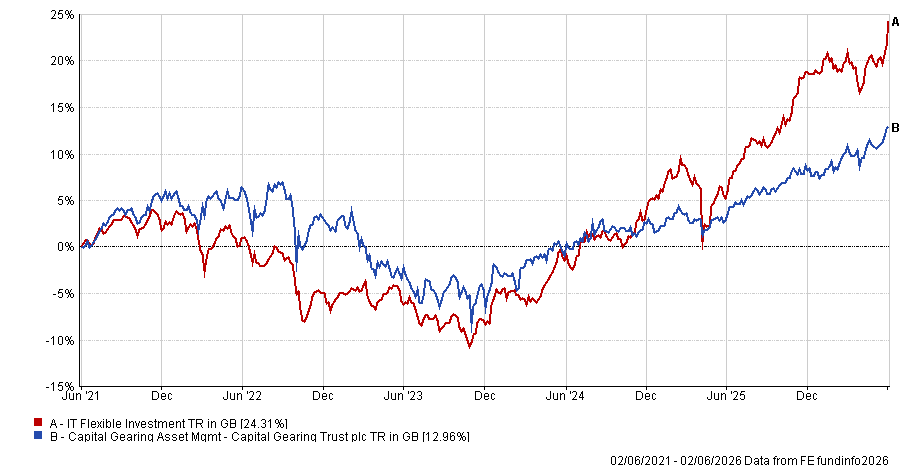

For those wanting managed active exposure rather than a simple ETF, Schooling Latter highlighted the Capital Gearing trust.

Performance of fund against sector over 5yrs

Source: FE Analytics