Markets are pricing in further Bank of England rate hikes due to the war in Iran and political instability at home but Mark McDonnell, macro analyst at Invesco, thinks this is the wrong call and that the data already supports a different conclusion.

“The market has some element of muscle memory from what happened in 2022,” he said, but investors are failing to understand that there are differences this time around.

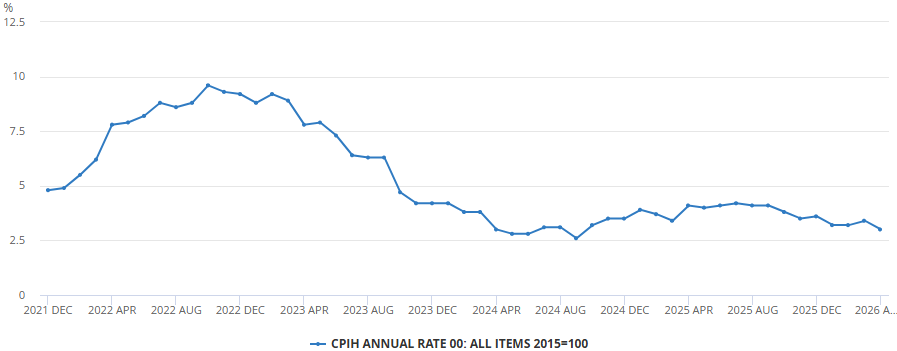

In 2022, UK inflation hit 11.1%, a 41-year high. Energy bills surged after Russia's invasion of Ukraine, food prices followed and workers, in a historically tight labour market, won pay rises large enough to keep up.

Those pay rises fed back into prices, which translated into pay demands and the Bank of England spent the next two years hiking rates aggressively to break the cycle.

Today, inflation is at a lower level but there are fears it could be on the rise again. The Consumer Price Index (CPI) came in at 3.3% in March before dipping to 2.8% in April and forecasters expect it to climb again to around 3.5% by year end as the energy price cap rises. On the surface, it rhymes with 2022, even if the overall figure is much lower.

But McDonnell's argument is that the mechanism is entirely different and that is what markets are getting wrong.

Performance of Consumer Price Index since December 2021

Source: Office for National Statistics

Compared to 2022, underlying demand is now weak and fiscal support has fallen from around 3% of GDP in 2022 to just 0.1% today. But the most important difference is the labour market.

“Back in 2022 we had a big inflation shock and an extremely tight labour market. Households had this inflation shock, they managed to get a big pay rise to compensate, and it led to a self-fulfilling cycle where inflation was more persistent,” he said.

“Now the labour market is significantly looser, unemployment is higher and I just don't see that workers have that same bargaining power to compensate for the inflation shock.”

Without that wage-price loop, the persistence that made inflation in 2022 so damaging isn't there.

Private sector wages are growing at 3%, wage settlements are running at between 3% and 3.5% and the Bank of England has indicated that wage growth of 3.25% is consistent with its 2% inflation target.

“I feel somewhat comforted,” McDonnell said. “I think it's underappreciated how much of the UK's recent experience with high inflation is not a function of underlying drivers within the economy but mostly big rises in taxation that have been inflationary, and because we've seen some significant changes in regulated prices around things like water bills. When you strip that out, the UK doesn't look too bad on the inflation front.”

This changes how central banks should react, as tax-driven and regulated-price inflation are largely a one-off. That said, McDonnell is still expecting inflation to rise before it falls again.

The investment angle is that if UK inflation is being misread, UK assets are mispriced and some of the cheapness in longer-dated gilts, which have traded near 30-year highs in yield, starts to look like opportunity rather than warning.

McDonnell said he is not yet ready to advocate for long bonds, citing UK political uncertainty as a second reason gilts yields are high. But he is more optimistic than current pricing implies.

What could unlock the situation is households saving. Britons are saving around 10% of their disposable income, roughly amounting to £180bn a year – well above the historic norm of around 5% and potential deferred spending.

“Those animal spirits have been caged over the past couple of years, and I think it's a function of the political environment and of high interest rates,” McDonnell said.

Ease these pressures – perhaps through a credible autumn statement and inflation falling, as he expects it will next year – and the picture changes.

“I think it's a positive story for the UK," he said. "But you need those two things to come together."