Every fund manager makes mistakes – the crucial part is how they go about identifying and then fixing them.

When Julian McManus told Trustnet last year that selling out of Alphabet had been a big mistake, he said he was looking at ways to correct it.

Sixteen months on, the co-manager of the £717m Janus Henderson Global Select fund has rebuilt the position to 4.6% of the portfolio, making it a top 10 holding.

“For the strategy, the opportunity cost of not holding Alphabet during some of that time when the stock was strong is real,” he said.

“But it is part of the process of being an active investor – you will make mistakes from time to time, so it is important to recognise them and learn from them.”

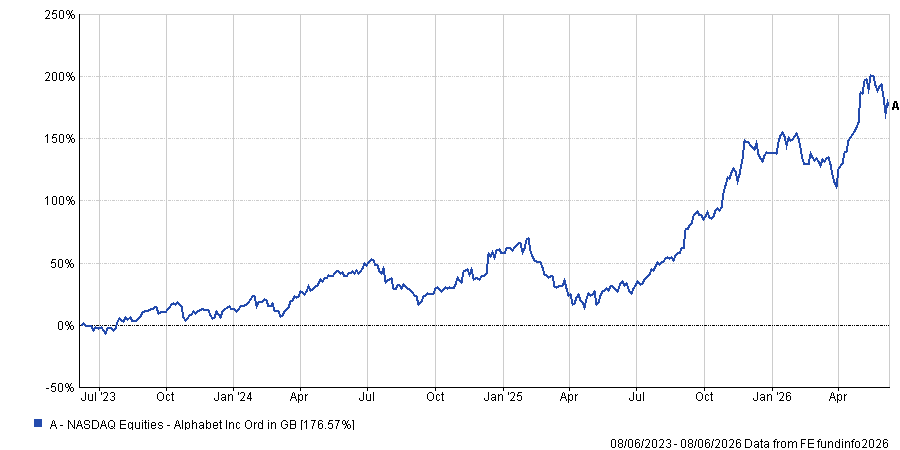

Stock price change over 3yrs (in sterling)

Source: FE Analytics

The first quarter of this year brought McManus confirmation that he had remedied the error, as Alphabet’s cloud business grew by 60% and margins expanded by 500 basis points (bps) quarter-on-quarter.

“Those are huge numbers and show that what the business is doing is very powerful,” he said.

Below, McManus explains what other opportunities he is currently backing and where he thinks the market is getting it wrong.

What is your fund’s philosophy?

We look for free cashflow that is undervalued by the market. At the end of the day, free cashflow is what investors get to eat, whether it is reinvested in the business or returned to shareholders – that is the source of value for us.

We try to go about this in a disciplined manner. We are benchmark-aware and we want to make sure that most of our risk budget – we use a range of 400-700bps as our target tracking error – goes on stock selection, not on factor bets like style, country, currency or industry.

Alphabet now sits alongside other big AI players in Janus Henderson Global Select’s top 10, such as Nvidia and Amazon. Is this a deliberate thematic concentration or individual stock conviction that happens to cluster around AI?

These positions are somewhat new for us, and they are based on valuation – the free cashflow is there and we think it is set to accelerate.

We did not own Nvidia until 2024 at all, as the valuation was not in range. However, this has become much more attractive at 20x this year’s earnings and 15x in 2027.

It is the same story with Amazon: while the stock has been going sideways and consolidating, it has been compressing valuation multiples, getting much more attractive and we think the business is in better shape than before.

What was the best call of the past 12 months?

TSMC is one of our top active weights – it was an average active position size of over 5% until recently – and has been our strongest performer over the past year.

The stock is up 120% over 12 months, contributing 550bps of return over that time.

It trades at an attractive valuation because of a lack of recognition of the strength of TSMC’s business but also because of Taiwan-associated risk.

But it is a position we have been trimming back recently, as we allowed TSMC to run a long way to the point it became over 500bps active overweight.

Are you worried about the risks to TSMC due to uneasy China-Taiwan relations?

In my mind, the ‘Taiwan risk’ to TSMC is going up quite rapidly for a couple of reasons. Firstly, what the US has been doing in the Middle East has left the Pacific theatre much more thinly defended, as munitions have been drawn out to help in the Middle East.

Secondly, during the summit we recently saw between president Donald Trump and president Xi Jinping, it was notable how president Xi has shifted the narrative around Taiwan. The fact he felt emboldened to ask straight out whether the US would defend Taiwan in the event of a conflict with China – to which Trump was very ambiguous in response – shows how successfully China has shifted the narrative around Taiwan over the past year.

We are still dealing in conditional probabilities here, but I think the risk has gone up a lot.

How do you address these kinds of risks in your portfolio?

We look to balance out the risk through our portfolio construction. In the case of TSMC, we have paired it with a large weighting in defence – specifically BAE Systems.

You can think of it as somewhat of a hedge in the sense that, if there is some form of conflict around Taiwan, most things will do poorly except for defence companies.

BAE Systems these days is very highly exposed to the US, with more than half of revenues coming from there, and particularly highly exposed to the Pacific theatre in terms of the products it supplies.

So that is one example of how we try to be thoughtful about how the portfolio will behave given the risks we are facing and the opportunity set in the world today.

Where else are you finding the most interesting opportunities?

European banks look interesting again. They were up 30% in 2024 and 80% in 2025 – and it is understandable that people took their profits at the end of that run. I understand why European banks have since been traded in a risk-off manner, but I think that is a dislocation.

Given the pressure they have been under since the outbreak of conflict in the Middle East, I think the market has got this one wrong, as I think we are looking at higher inflation for longer because of spiking energy prices. This is good for rate-sensitives like European banks because it means higher net interest income for longer.

In addition, St. James’s Place is our top contributor to tracking error. It has attracted a lot of negative press attention for overcharging clients and giving them too little advice. New management fixed that problem and gave clients a fee holiday to draw a line under it.

That fee holiday is due to come to an end over the next year or two, and yet that is not factored into forecasts – so this is going to catch up with our modelling rapidly over the next 12-24 months. I find that an exciting asymmetric proposition right now.

What was your worst call of the past 12 months?

Our worst call has been US-listed insurance brokerage company AJ Gallagher – it was a 2.5% average position and is down 40% over the past 12 months. It has detracted 150bps in absolute terms and 245bps in relative performance – a painful position.

But we think the stock’s underperformance has come entirely out of valuation multiple compression, not out of earnings – earnings forecasts are pretty much flat over the past 12 months.

The market has taken a very dim view of insurance brokers, both because the insurance pricing cycle has rolled over and softened, turning people negative on the whole space, and because there is the question of AI disruption risk.

We feel it will not be as negatively impacted by AI as the market believes, as there are aspects of an insurance broker's business that cannot be easily replicated, such as access to proprietary data and building and maintaining relationships with clients.

What do you do outside of fund management?

In the summer I like to cycle a lot and then in the winter that flips to skiing.