A potentially historic El Niño event is forming in the Pacific, which investment strategists warn could push global food prices to levels that would add over a percentage point to developed economies’ headline inflation within 18 months.

El Niño is a periodic warming of sea surface temperatures in the central and eastern Pacific Ocean that reshapes rainfall and temperature patterns in key growing regions, bringing excessive rainfall to parts of South America while triggering drought across south-east Asia, India, parts of Africa and Australia.

The World Meteorological Organization assigns an 80% probability for El Niño condition in June-August 2026. The organisation’s secretary-general, Celeste Saulo, said: “We need to prepare for a potentially strong El Niño event which will exacerbate drought and heavy rainfall and increase the risk of heatwaves."

WisdomTree head of commodities and macroeconomic research Nitesh Shah and director of research Aneeka Gupta noted that 2024 was the hottest year on record, with global average surface temperatures 1.55 degrees above the pre-industrial average, and said agricultural systems are already operating under stress from that elevated baseline.

The Hormuz fertiliser disruption, which has roughly doubled urea prices since the conflict began, adds to the problem.

"[El Niño’s] significance in the current context is that it has the potential to reduce agricultural crop yields in the same producing regions that would otherwise have helped offset the input cost pressures arising from the Hormuz disruption," Shah and Gupta said. "Both forces are pulling in the same direction at the same time."

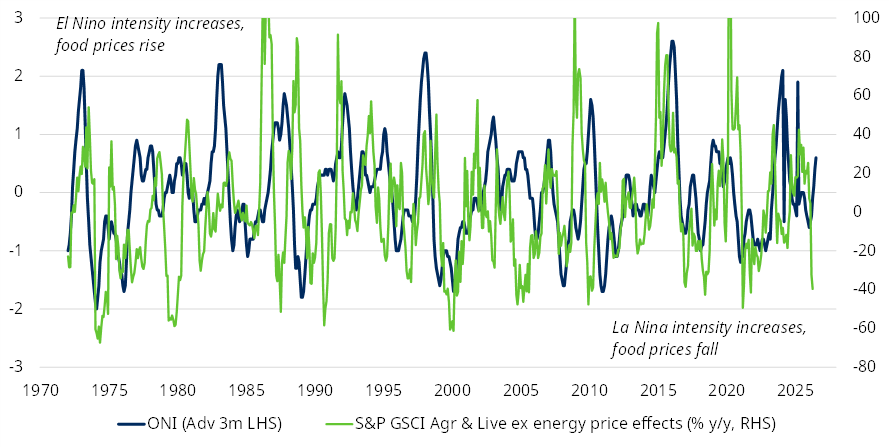

The historical relationship between El Niño's intensity and food prices points toward a sharp rise ahead. David Rees, head of global economics at Schroders, said, if past correlations hold, a very strong El Niño would imply a doubling of global food prices from current levels over the next year or so.

A rising Oceanic Niño Index usually results in higher global food prices

Source: Schroders, LSEG Datastream

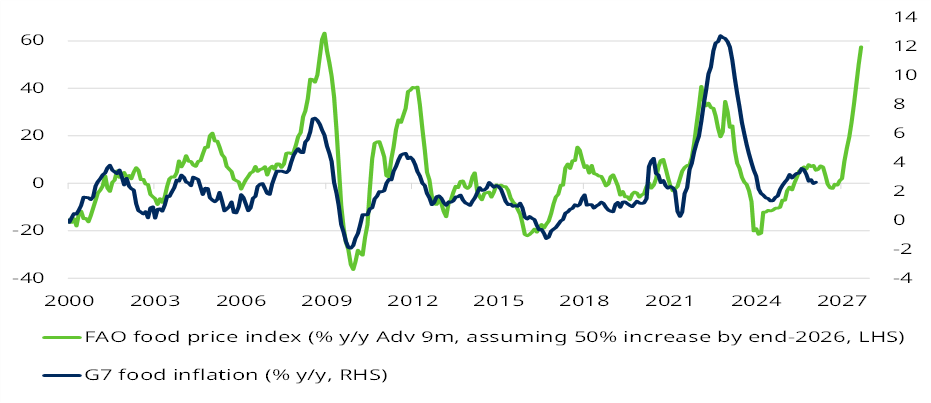

"If this confluence of factors caused the UN [Food and Agriculture Organization] food price index to rise 50% by year-end, the usual lags mean G7 food inflation would probably hit double-digits in 2027, enough to add over a percentage point to headline inflation," Rees said.

Shah and Gupta identified a typical six to 12-month gap between the peak of an El Niño event and the peak of its production impact, meaning “stress that is already appearing in agricultural systems today is likely to intensify before it eases”. Markets have historically repriced ahead of confirmed production impacts, reacting in anticipation of tightening supply rather than waiting for harvest data.

The crops most exposed reflect El Niño's particular geography. Cocoa stands out: West Africa, the world's largest producing region, suffered significant output declines in both the 1997-98 and 2015-16 El Niño episodes.

Hakan Kaya, commodities portfolio manager at Neuberger, said: "El Niño can intensify the winds which descend from the Sahara across west Africa. Hot, dry conditions stress cocoa trees, suppress pod development and reduce bean quality."

WisdomTree's research found that every strong El Niño in the past 55 years has reduced global cocoa production.

Sugar looks equally exposed, as previous El Niño events cut production in India and Thailand by 20% to 30%, pushing major producers towards net imports.

Rees said: "The impact could be more pronounced this time because a greater share of sugar stockpiles is being diverted into ethanol production. Biofuel demand is being reinforced by the Middle East oil shock, increasing usage of sugar, corn and soybean oils."

Robusta coffee is another pressure point. Vietnam accounts for more than 40% of global robusta supply and is among the regions most exposed to El Niño-driven drought. The 2015-16 event cut Vietnamese output meaningfully and fuelled a sharp rally in robusta futures. Arabica, by contrast, tends to benefit from El Niño conditions in Brazil's main growing regions.

Wheat faces headwinds from Australia, which has seen production declines due to El Niño-related drought in nearly every such event over the past six decades, with Schroders estimating potential losses of around nine million tonnes in 2026/27.

WisdomTree’s Shah and Gupta highlighted a critical distinction between crop types: "For annually planted row crops such as wheat and corn, sub-optimal fertiliser application in the 2026 planting cycle will compress yields in the 2026/27 harvest, a one-season impact that can recover if input supply normalises.

"For perennial crops such as coffee and cocoa, the damage is more persistent: nutrient and weather stress during flowering and fruit-set reduces yields across multiple subsequent harvests from the same plants and new planting takes three to five years to reach productive maturity."

Rees argued that the macroeconomic concern is what rolling waves of food inflation mean beyond a single shock. Second-round effects on wages raise the risk of price pressures becoming entrenched and the political consequences could be significant, with prolonged cost-of-living pressure potentially fuelling a further populist shift in Europe ahead of key elections.

A wave of food inflation could hit the global economy just as the energy price shock subsides

Source: Schroders, LSEG Datastream

Food represents 10 to 15% of developed market consumer price baskets and 25% or more in emerging markets, meaning the distributional impact is sharpest where it is least affordable.

For investors, Kaya added: "This is supply-driven inflation, the kind that monetary policy can struggle to address. This risk is not adequately reflected in current market pricing.

“When combined with supply concerns across the broad commodity universe, from copper to oil, we see a strong case for investors to consider tilting asset allocation toward commodities, not only for diversification and inflation hedging purposes but also for the potential for attractive returns."