Investment trust managers are beginning to rebuild exposure to UK mid-caps, arguing that the FTSE 250 now offers some of the most compelling valuations in global equities.

Over the past few years, the index’s more domestically tilted profile was damaged by post-Brexit sterling weakness and the persistent outflows from UK equity funds. Poor sentiment has subsequently weakened valuations across the board among UK mid-sized companies.

That backdrop has created what some managers describe as a rare opportunity.

Simon Gergel, lead manager of Merchants Trust, said valuations have moved to levels that are difficult to reconcile with fundamentals.

“Companies in the FTSE 250 are trading well below its last 10-year average rating – and miles below the rest of the UK and international markets. That is highly unusual,” he said.

“Yet mid-cap companies in the UK are expected to trade at a premium to larger companies because they have historically delivered better growth. At the moment, they are at big discounts due to poor sentiment.”

Jean Roche, manager of Schroder UK Mid Cap Investment Trust, pointed out that many UK mid-caps are still delivering strong earnings growth despite being priced cheaply at an average of 12x earnings.

“A mid-cap company may be growing its top line by 5% and the bottom line by 10% but be trading on 10x earnings – it just doesn’t make sense,” she said, noting that Schroder UK Mid Cap portfolio holdings have an average earnings growth of 13%.

Another clear signal is that the FTSE 250 is yielding more than the FTSE 100. According to FTSE Russell data, the FTSE 250 yields 3.53% and the FTSE 100 yields 3.06%, as of 29 May 2026.

Gergel said: “It is very unusual for the FTSE 250 companies to be on a higher yield – and that is where we are going to be focusing our buying in that area as we reduce the FTSE 100 exposure over the coming period.”

He noted that Merchants Trust has around half of its portfolio in FTSE 250 stocks, particularly among the most domestic names in real estate, retail and construction.

James Henderson, manager of Lowland Investment Company, made the same point, also noting he plans to focus on buying in the mid-sized market as he reduces the trust’s FTSE 100 exposure.

Henderson said the yield anomaly reflects years of underperformance among domestic earners.

“UK medium and smaller companies have been underperforming the large, and that's because UK medium and smaller have much more exposure to the UK domestic economy,” he said, putting this down in large part to the ramifications of Brexit.

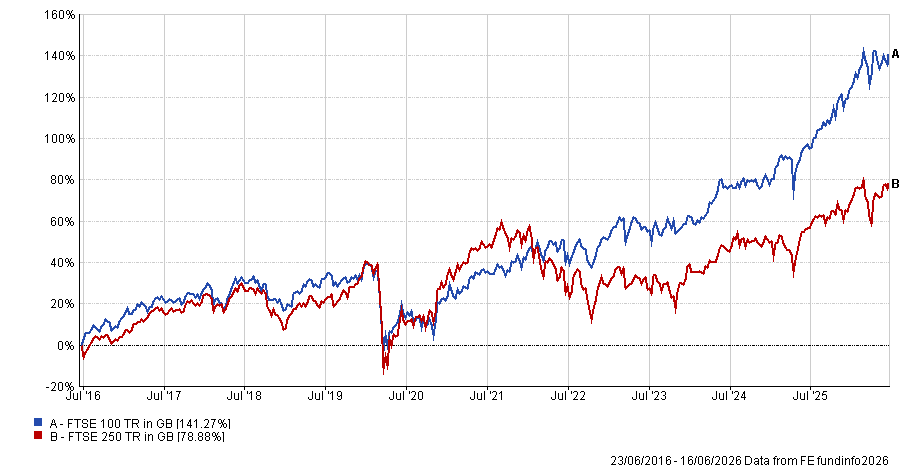

Performance of FTSE 250 vs FTSE 100 since Brexit

Source: FE Analytics

“Hopefully, it has now played itself out, leaving these companies looking cheap,” Henderson said.

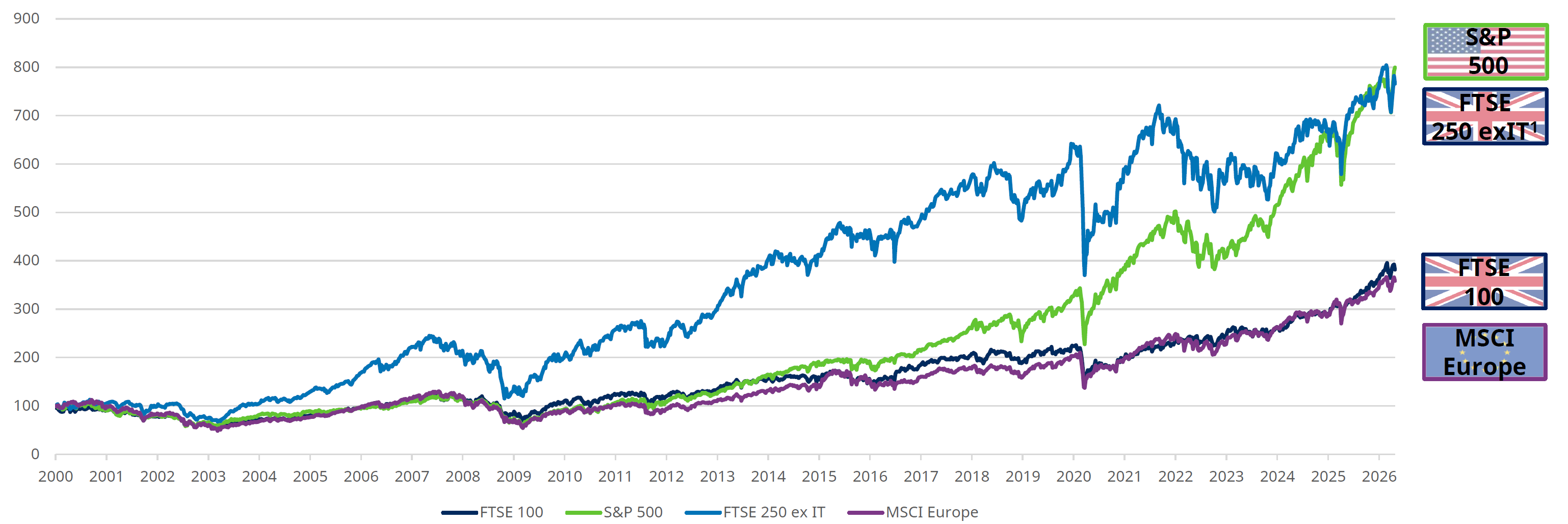

But zoom out to before Brexit and the picture changes. Roche pointed out that the longer-term performance of UK mid-sized companies tells a much more positive story, as the FTSE 250 excluding Investment Trusts has outperformed most developed market indices and kept pace with the S&P 500.

FTSE 250 ex Investment Trusts vs large developed markets (total return %)

Source: Schroders, Refinitiv Datastream. Rebased to 100 at 1 January 2000, data to 1 May 2026. Currencies are base currencies for individual indices.

Roche said this is because mid-caps sit in a sweet spot between small-cap alpha potential and large-cap stability.

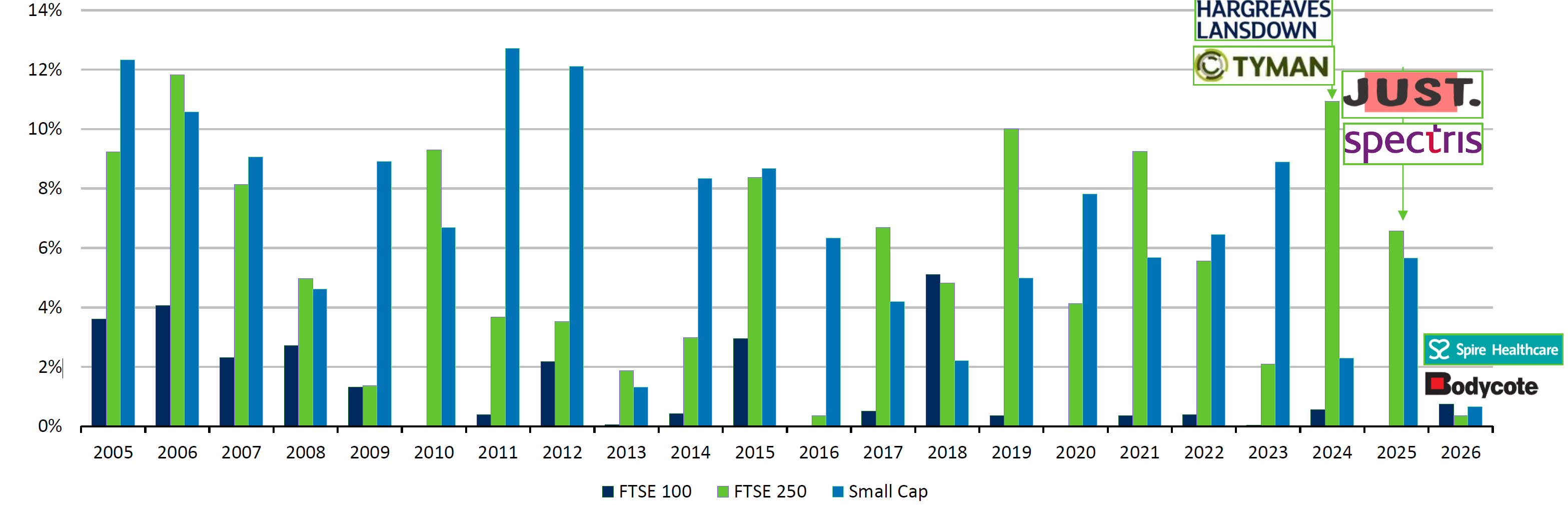

“These are mature, cash-generative companies that are still small enough to be acquired,” she noted.

“Within Schroder UK Mid Cap, we had two companies – Just Group and Spectris – taken out last year at 75% and 100% premia and they represented 8% of the trust. The more typical premium in the UK market is 30-35% but in mid-cap land we have been seeing premia of closer to 50% for two years running.”

Value of completed acquisitions as % of index starting market cap

Source: Schroders, Panmure Liberum, 18 May 2026.

As such, Roche said there is “an embarrassment of riches” in terms of what investors can buy cheaply in the mid-sized market.

“We just look to buy the best communicators, the ones that provide the best insight into how they are managed,” she said.

However, given the high exposure to the domestic landscape that many of these companies have, Roche currently avoids companies in sectors where political risk dominates but still sees resilience in niche consumer areas, such as the defence sector as a technology play or companies providing access to high-protein products.

“House builders are the key example, as they are at GFC [great financial crisis of 2008] era valuations without the GFC-era balance sheets, so there is a case for holding some – but I don’t tend to be overly brave in sectors that are highly political.”

More broadly, when asked whether the rotation of multi-cap and large-cap managers into the FTSE 250 validates the opportunities in the mid-cap market or risks eroding the valuation discount, Roche was direct: “I’d say to them: come on in, the water’s warm.”