UK stocks are getting picked off consistently by both overseas and domestic corporations, or private equity firms. The numbers show a remarkable story: we're not even halfway through the year and the total value of UK takeovers for 2026, should they all complete as planned, is £39.3bn – 33% more than the £29bn value of deals in the whole of 2025 and, at 28 deals so far, they're coming at a rate of more than one per week, according to analysis from the investment platform AJ Bell.

The companies at the centre of this bidding frenzy come from all walks of life, from Nuveen's £10bn takeover of Schroders and Zurich's £8bn offer for Beazley, all the way down the market-cap spectrum, through Ingredion's £2.5bn approach for Tate & Lyle to Animalcare's take-private by Charterhouse Capital Partners for £235m.

Many have sounded the alarm at the shrinking of UK public markets, with performance suggesting a dearth of good companies in which to invest. One could certainly read the data that way; why else would UK investors, according to the Investment Association, have pulled a net £74bn out of UK equity funds since the start of 2016?

All of the above goes to show that there is now a structural undervaluation of UK plc by public market investors of all stripes. But who exactly is this benefiting? It's benefiting those private equity funds and trade buyers that are picking UK businesses off at alarmingly cheap valuations.

Indeed, of the 22 deals agreed so far this year where the terms have been made public, the average premium offered relative to the undisturbed share price was 45%.

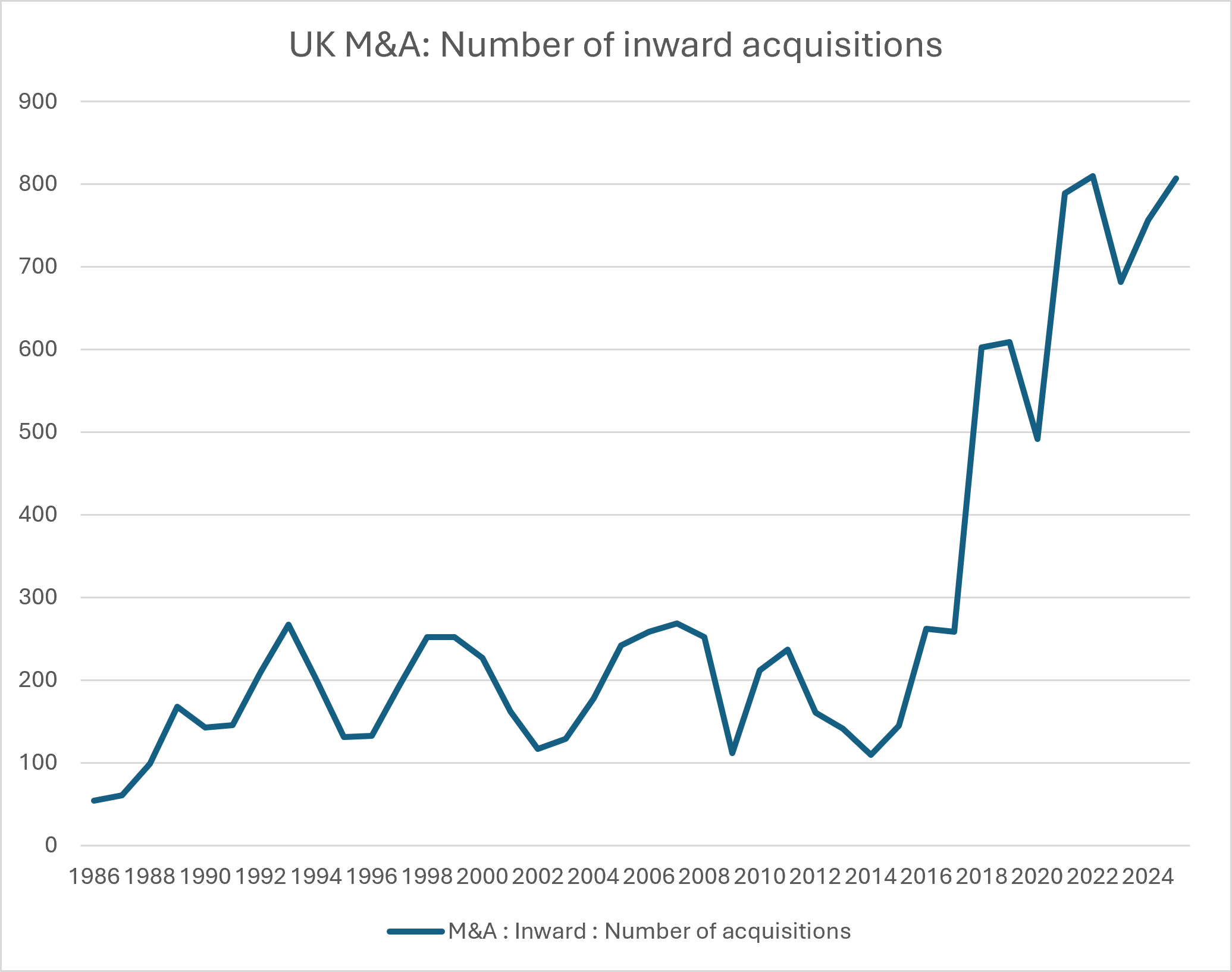

This is a theme we've seen for a few years now. Broadening the data out to all UK companies, the number of inward acquisitions (that is, foreign companies acquiring UK companies), you see a real step-change.

Between 1986 and 2017, the average number of inward acquisitions was 180 per year; since 2018, that number has risen to 693, according to the Office for National Statistics (ONS).

Source: ONS

So, where does this all leave us? We suspect the constant selling of UK plc by retail investors is so they can stock up on the winners of the past (i.e. US big tech, through passive, index-tracking funds). In our view, investors should be looking ahead, not to what has already happened.

Valuation and concentration risk in broad global markets is high, but this doesn't mean investors need to dial down equity exposure. Rotating into cheaper markets should improve diversification and, hence, potential future returns.

It's very possible that we're seeing a potentially generational investment opportunity within UK SMID caps. To us, the sheer number of UK companies being taken out just shows that the UK market is packed with excellent businesses that are attracting suitors from around the world.

Of course, it's impossible to tell exactly what and when the catalyst will be to bring public market investors back to UK SMIDs, but, after more than a decade of consistent outflows, we are surely closer to the end of this trend than the start. We certainly don't think that one should be jumping off the train at this point in time.

Schroder UK Mid Cap recently agreed to propose a tender offer to try to draw a line under a campaign by Saba Capital, which has a 19.5% stake, against the trust.

Saba has said that it will support the proposal and tender its shares, which makes sense for the activist hedge fund, but for ordinary investors tempted to participate, it would be akin to throwing the baby out with the bathwater, in our view.

In fact, SCP is one of the best-placed trusts around to capture any re-rating of UK mid-caps (as the trust's name suggests). Managers Jean Roche and Andy Brough have constructed a portfolio of 50 names focused purely on the FTSE 250, which they believe offers a mixture of leaders from niche or growing industries.

Jean and Andy also like the FTSE 250 as it is regularly refreshed thanks to promotions and demotions from other parts of the market as well as IPOs, providing a steady stream of world-class opportunities.

Another mid-cap focused trust where the rating may not reflect the potential is Mercantile, where managers Guy Anderson and Anthony Lynch invest predominantly in mid-caps, with historically around three quarters of the portfolio in FTSE 250 companies.

Guy and Anthony's bottom-up process focuses on company fundamentals to identify high-quality businesses that are generating positive momentum and are available at attractive valuations.

One option that scours the whole of the market is Fidelity Special Values. Managers Alex Wright and Jonathan Winton take an unashamedly contrarian and value-focused approach, with performance driven by bottom-up selection.

We think that this provides resilience when positive developments are being overlooked (such as now) and enables FSV to outperform across different market cycles and environments.

Moving down the market-cap scale, Rockwood Strategic is a highly differentiated trust that has outperformed even its lofty 15% annualised goal over the long term thanks to manager Richard Staveley's bottom-up process, which has led to a highly concentrated portfolio of between 20 and 25 undervalued, micro-cap companies.

This concentration enables Richard to take sizeable stakes in his holdings, supporting his approach of collaborating with management teams to help instigate a turnaround.

The fund has already this year benefited from two takeover bids at Treatt Plc and Van Elle Plc, both at significant premiums.

We see plenty of reasons why public market investors might return to reassess the attractions and cheapness of UK stocks, hence putting a stop to the picking off of UK plc by acquirers and hopefully breathing life back into an important part of the economic ecosystem.

David Brenchley is an investment specialist at Kepler Trust Intelligence. The views expressed above should not be taken as investment advice.