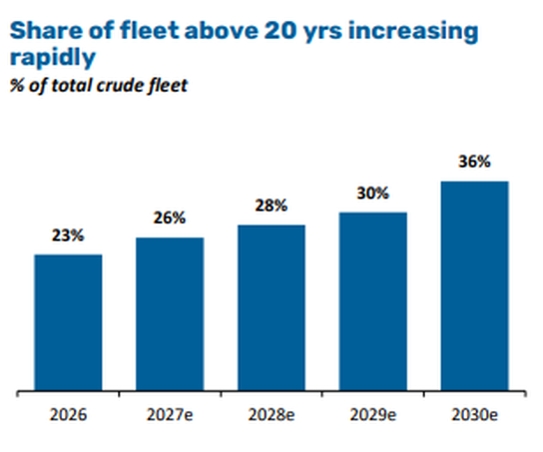

The crude tanker market was not in balance going into the war in Iran. Over 20% of the global fleet of VLCCs (the massive super tankers that carry two million barrels of oil per voyage) was already 20 years old. This is an important threshold where maintenance costs rise, efficiency falls and regulatory pressure intensifies.

Environmental rules and the increased risk of spillages means that many oil companies refuse to charter them, forcing this cohort towards the margins and creating a significant shortfall of the vessels needed to carry oil around the world.

Source: Capital Tankers presentation.

The supply picture becomes even more complicated as many of these older vessels have drifted out of the mainstream market altogether. It is believed that over 20% of VLCCs now operate in the sanctioned or ‘shadow’ market – quietly moving Russian and Iranian crude to buyers.

These ships operate outside Western insurance frameworks and are effectively unavailable to conventional charterers. Even before the first shots were fired in the Middle East earlier this year, the headline supply already overstated the reality.

What happens when a tight market meets a shock?

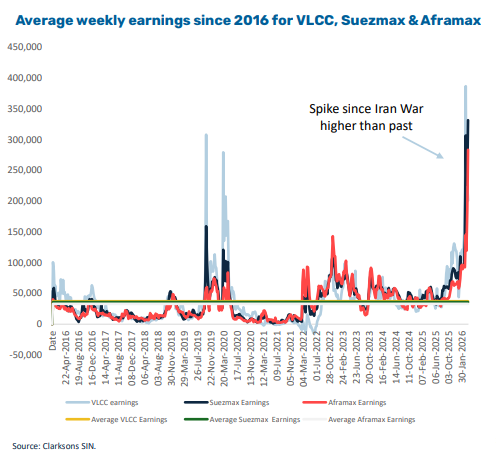

The war in Iran and the closure of the Straits of Hormuz turned that underlying tightness into something much more extreme and serious. With roughly 20% of global oil flows normally passing through the strait, disruption had immediate consequences.

Cargoes stalled, vessels queued and insurers stepped back. Shipping rates surged as they typically do in such moments.

While these spikes rarely persist, they serve a useful reminder that the system that moves crucial energy supplies around the world is quite fragile.

The message is clear: spare capacity is limited and the system does not absorb shocks easily. Shipping markets tend to overshoot in both directions. Periods of calm breed complacency but periods of disruption expose what was already broken. The reopening of Hormuz is not the end of the story – it is the beginning of the next chapter.

Why the reopening is the real opportunity

It is tempting to view this as a short-lived event where rates spike initially, tensions ease and then markets normalise. We think that misses the point. The reopening of Hormuz is unlikely to reset the market to where it was before. Instead, it sets the stage for the next phase of the cycle, where several supportive dynamics begin to align.

First, there will be an immediate demand surge. Key importers, particularly across Asia, will have drawn down inventories and delayed cargoes, meaning strategic reserves released during the disruption will need to be rebuilt. When flows resume, this demand backlog does not usually return gradually – it tends to arrive all at once.

Next will come a permanent route rewiring. Relying on a single chokepoint for a significant portion of global energy supply has proven incredibly costly and the rational response must be to improve diversification through alternative sourcing, increased stockpiling and more complex routing. All of these require more shipping capacity per barrel moved.

Lastly, we will likely see structurally higher rates. Shipping is not just about how much oil moves, but how far. Longer routes, indirect flows and redundancy all increase effective demand for vessels, even if underlying volumes remain unchanged.

Insurance costs, chartering behaviour, and routing decisions rarely revert fully to pre-crisis norms – a degree of caution may linger and that caution has a price.

Is this just another cycle?

Shipping is often framed as a purely cyclical industry. That is broadly true but there are periods where structural factors take over. This increasingly looks like one of them.

On the supply side, the fleet is ageing and bifurcated. Older vessels face regulatory headwinds, while a sizeable chunk of capacity is tied up in non-compliant trades. Meanwhile, on the demand side, the system is becoming more complex. Energy security considerations are rising and supply chains are adjusting accordingly.

This points to a market where effective capacity remains constrained and utilisation stays higher for longer.

In this environment, the gap between ‘good’ and ‘bad’ assets widens. Modern, fuel-efficient vessels – particularly those aligned with tightening emissions standards – should see consistently stronger utilisation and pricing. They are the ships charterers prefer when optionality narrows.

By contrast, older tonnage faces a more uncertain future, while vessels operating in sanctioned markets remain largely excluded from mainstream demand.

This is not a rising tide lifting all boats; it is a more selective market where quality matters. The Norway-listed shipping company Capital Tankers offers a clear way to access this theme. Backed by Capital Maritime, the company is building a young, modern fleet with a focus on efficiency and compliance.

While the current fleet is relatively small, the delivery pipeline over the next few years materially scales the platform.

Crucially, much of this expansion has been secured ahead of the recent disruption. In effect, the company has locked in fleet growth at pre-tightening prices.

As those vessels deliver into what we see as a more supportive rate environment, the earnings potential changes significantly. What today looks like a modest base could evolve into a very different profile as utilisation and rates normalise at higher levels.

Mike Clements and Pras Jeyanandhan are managers of the VT Tyndall European Unconstrained fund.