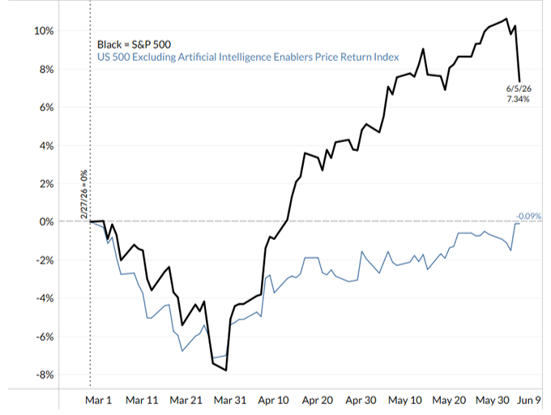

The contrasting fortunes of the market are the most extreme that I’ve seen in my investing lifetime. The US index is up sharply, but if you exclude the AI enablers, it’s barely moved since the Iran war broke out.

Strip out the AI enablers, strip out US stocks’ performance

Source: Bianco Research, Goldman Sachs, Bloomberg; S&P 500 excl. AI enablers price return vs S&P 500, 27 Feb 2026 to 5 Jun 2026

Hopefully, this will prove to be a high-water mark. A place where the market can start to broaden out, as this domination is unlikely to continue sustainably.

To put this bifurcation into context, the US large-cap technology sector has outperformed the S&P 500 by six standard deviations over the past 50 days; a six-sigma event is the equivalent of a ‘black swan’ – in (admittedly too simplistic) mathematical terms, that’s a one-in-506-million event.

Although, given the enormity of trend-following machine trading and passive flows, perhaps we shouldn’t be shocked.

According to some analysts, 75% of active fund managers are now overweight the semiconductor sector. We are part of the quarter that is not. While we hold several companies in this space, we’re managing our semis exposure carefully.

We prefer to focus on the most protected investment cases rather than the commodity-driven memory and DRAM (Dynamic Random-Access Memory) players.

We own Nvidia – which we’ve owned for over seven years – which remains the best-performing investment in our fund’s history. Despite its expected continued domination of GPU AI workloads, the shift to AI inference and the emergence of agents will benefit CPU players in the industry.

Our new holding in Arm (up 250% year to date), which we started last year, should be a significant beneficiary of this trend. This is because the CPU concentration is much higher in inference workloads, which plays into Arm's hands.

Historically, Arm has been exclusively an IP licensing and royalty business, with almost all mobile chip designs optimised on Arm architecture. To capture greater value and reduce time-to-market, it’s started vertically integrating into physical chips. This will become a third leg of revenue, offering full end-to-end CPU solutions for data centres without cannibalising its traditional IP business.

And Arm’s off to a good start – its newest data centre chip is apparently 50% more energy efficient and has twice the computing performance compared with its main competitor, so it should be able to capture significant market share.

Analysts at Jefferies believe Arm could sell 1 million chips in two years’ time – assuming a 45% gross margin and $1,500 average selling price, this implies $1.5bn in additional revenue and $675m in gross profit.

As an IP-only business the current average selling price, based on royalties alone, is just $15 per data centre chip. After the shift in its business model that would be $1,500 – a huge value creation opportunity.

Outside of semiconductors, software has had a harder time. Markets are pricing extinction for enterprise and consumer software. We think this is histrionics.

We have sold our position in book-keeping program developer Intuit because more questions have emerged around its recent results. These concerns pointed to competitive market-share losses in its TurboTax product for DIY tax filers who make less than $50k.

This isn’t due to AI alternatives, but simple price undercutting. The fear is that pricing and market share are eroded in higher-value SKUs as greater functionality and the technology lead narrows.

But we enjoyed a rare bright spot in software as our holding in cybersecurity provider CrowdStrike made a sharp move higher off the lows since we bought it in February.

This company was caught in the software SaaS-pocalypse as it sits in the software ETF basket. Yet cybersecurity risks are only increasing and this company should see a significant uptick in deployments as companies want to guard against AI risks.

Staying broad when the market's gone narrow

When a handful of semiconductor stocks account for the lion's share of index returns, and passive flows keep funnelling money into the same crowded trade, it can feel like you're running a race where only one lane counts.

But we've been here before and history shows that extreme concentration is a feature of late-cycle exuberance, not a permanent state of affairs.

We own world-class companies with resilient, reliable and repeatable growth. Our ‘weatherproof’ bucket, spanning healthcare, staple services, pest control, uniform rental and waste management, won't make headlines.

But these businesses compound quietly and should prove their worth when the tide turns. And tides always turn.

The AI investment theme is real. We’re positioned to benefit through Nvidia, Arm, cabling and connector supplier Amphenol and hyperscalers Alphabet, Amazon and Microsoft. But we refuse to bet the farm on a single narrative, no matter how compelling.

Some 75% of active managers are now overweight semiconductors. When three-quarters of the crowd is leaning the same way, the contrarian in me gets uncomfortable.

We'd rather own the highest-quality, most structurally protected names in the space, and pair them with businesses that can thrive regardless of which way the AI wind blows.

The recent sharp correction in semiconductor stocks – triggered by Broadcom's earnings miss in early June – is a reminder that even record-breaking growth can disappoint when expectations have gone parabolic.

The PHLX Semiconductor Index shed over 10% in a single session, wiping more than a trillion dollars in market value. That's not a panic signal, but it shows that the market's tolerance for anything less than perfection in AI names has evaporated. Our balanced positioning should help us navigate these air pockets.

US corporate earnings growth is running at its strongest pace since late 2021 and the breadth beneath the surface is quietly improving. When rate expectations shift, or the geopolitical backdrop calms, the market's narrow obsession with AI enablers could give way to a much broader rally.

That's exactly the environment where our diversified portfolio of best ideas – our ‘shots on goal’ – should start to score.

James Thomson is manager of the Rathbone Global Opportunities fund. The views expressed above should not be taken as investment advice.