Terry Smith's decision to put less emphasis on the 'do nothing' leg of his investment mantra has drawn a mixed response from fund analysts, ranging from sympathy for his read of the market to scepticism about why the change has come only now.

Smith has long run his £12bn Fundsmith Equity fund with three rules: buy good companies, do not overpay and do nothing. But in his recent semi-annual letter to investors, the manager said while the first two legs stand, the third needs revising.

The fund opened 12 new positions in the first half of 2026, including GE Vernova, Mastercard, TSMC and Netflix, while exiting Unilever, Novo Nordisk, Nike and Zoetis, taking portfolio turnover to a high.

Smith's justification for the change rests on a market he sees as dominated by passive flows and AI-driven momentum rather than fundamentals. He singled out one technique he is stepping back from: buying quality companies after a setback, the approach that worked for Warren Buffett's investment in American Express during the salad oil scandal.

In today's market, he wrote, "all we are getting is cut fingers as their downward share price spiral is exacerbated by the index momentum enhancement effect".

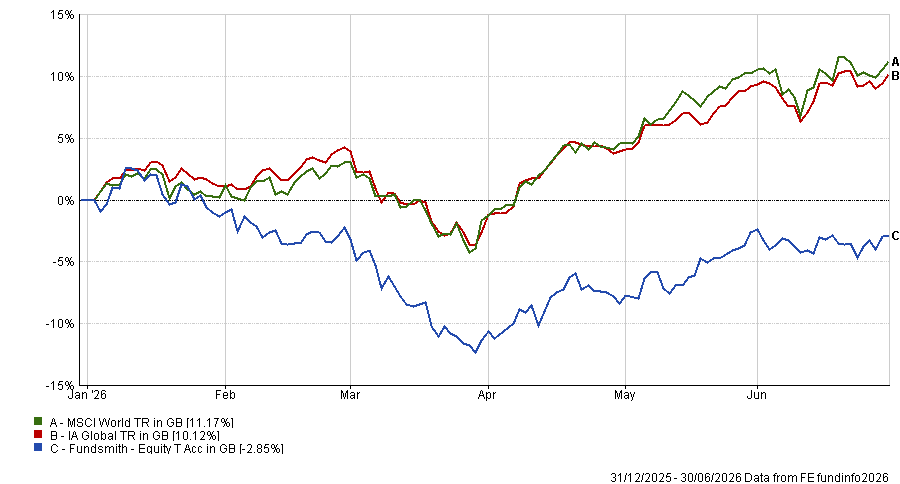

Performance of Fundsmith Equity vs sector and index in H1 2026

Source: FE Analytics. Total return in sterling between 1 Jan and 30 Jun 2026

Fundsmith Equity fell 2.9% in the first half of 2026, against an 11.2% gain for the MSCI World index in sterling terms. Portfolio turnover reached 51.8%, a high for the fund.

Smith said: "We run open-ended funds, and you can and increasingly have been taking money out, we suspect mostly to join the exodus from active to passive, or possibly to invest in managers who profess that they understand quality better than we do.

"They may be right, or they may just be closet momentum investors, which will be fine until it isn't. However, there will be little point being proved right about the dangers of passive or momentum investment after our fund has closed."

Ben Yearsley, director at Fairview Investing, pushed back on that framing, saying "it feels a bit disingenuous" for Smith to suggest managers who have done well are just momentum chasers.

But Yearsley's larger question is one of timing. "Is he admitting after 16 years that he has been wrong? And if so, why has it taken until now to change course?" he said, noting that the quality style favoured by Smith and managers such as Nick Train has been out of favour for several years already.

Simon Evan-Cook, manager of the MGTS Downing Fox funds, was cited approvingly in Smith's letter for his own writing on the shortcomings of passive investing. He took a more sympathetic view of the Fundsmith Equity manager's move.

"There was an industry belief that low turnover = good, high turnover = bad, and that cast a long shadow," Evan-Cook wrote on LinkedIn. "But that was oversimplified, and now markets have changed too."

He agreed with the view that markets are genuinely different after quantitative easing and the Covid pandemic, with volatility returning "with a bang".

"Active investors aren't driving any more, so it makes sense to adapt to the craziness that now happens. Being on the wrong side of that hurts investors," he added.

Rob Morgan, chief analyst at Charles Stanley Direct, cautioned against attributing all of Fundsmith Equity's underperformance to the dynamics Smith described.

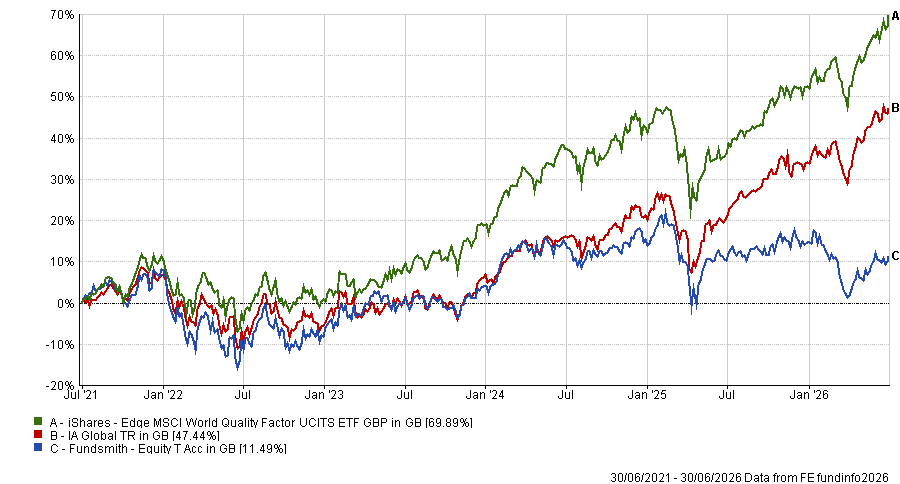

He pointed out that the fund sits in the fourth quartile of the IA Global sector over one, three and five years while the iShares Edge MSCI World Quality Factor UCITS ETF, charging a quarter of Fundsmith's fee, has beaten it comfortably over the same periods.

Performance of Fundsmith Equity vs sector and quality ETF over 5ys

Source: FE Analytics. Total return in sterling between 1 Jul 2021 and 30 Jun 2026

Even allowing for the ETF's heavier technology weighting, Morgan argued that this suggests Fundsmith's underperformance is not just about momentum and passive dominance alone.

On the change itself, he had some sympathy: "It makes sense to acknowledge the market characteristics and aim to take advantage of outsized moves rather than simply being a cork on the ocean of volatility. In that sense, modifying the 'do nothing' part of the approach is logical."

But he suggested the actual changes go well beyond that description. Pointing to Smith's retreat from buying quality companies after a setback and the new weight placed on price and fundamental momentum, Morgan asked: "Does the first part of the fund's mantra now become 'buy good companies that are not falling in value' and it's a case of if you can't beat the momentum investors join them?"

Yearsley raised a related concern about execution. "I don't have an issue with tweaking the style, however the question to be asked now is whether Terry and team can deliver in a faster-paced environment with more change at a portfolio level. Will they end up chasing performance?" he asked.

In his letter, Smith questioned the market's enthusiasm for the AI-driven narrative while adding names such as TSMC that sit inside that same ecosystem. Morgan noted that these businesses would be unlikely to escape unscathed if AI infrastructure spending disappointed.

Yearsley said it seems "a bit weird" to be adding holdings like TSMC after such a strong run. Morgan added that this raises the question of whether these are "a short-term trade rather than a long-term hold".

On where all this leaves investors, Morgan said: "The crucial question that must be asked: whether the manager has made a correct, pragmatic decision to adapt to a new world or whether he is mistakenly abandoning an important tenet of his process. Ultimately, this probably depends on where you stand on the market dynamics right now."

Yearsley said he has not been an investor in Fundsmith Equity and "probably wouldn't start now".

Evan-Cook concluded that Smith's portfolio changes are, at the moment, "Schrödinger's Trade: simultaneously both a good idea and a bad one".

"We will only know if it's a stroke of genius or a miscalculation once the markets have judged," he said.

"I hope it pays off. Fundsmith has made investors a lot of money over the years, and it's been a great advert for active fund management (and at a time when other star managers were screwing up). We need more success stories like this."