Investing in the UK is like running up a down-facing escalator, according to JOHCM UK Equity Income manager Clive Beagles, who said the structural headwinds of the past two decades have made it extremely difficult for domestic funds.

It is no secret that the UK market is a dwindling power on the global stage. Once a powerhouse, it has less total market capitalisation ($2.8trn) than both Nvidia ($3.6trn) and Apple ($2.9trn), with other US tech giants not far from overtaking the entire market either.

And it will take real and meaningful change to arrest this. “Just tinkering around with little fiddly things isn't going to make any difference,” said Beagles.

The UK was once far more important, he noted. When the JOHCM UK Equity Income fund manager started his career in 1989, it was 15% of the world index and the second-largest equity market in the world.

“Every international investor had to have an allocation to the UK because it was too important. It was a badge of honour to be listed in the UK,” he said.

But the decline has been steady and unrelenting. Its allocation dropped to around 10% by the turn of the century and today stands at around 3.5%, placing it in third place after the US and Japan.

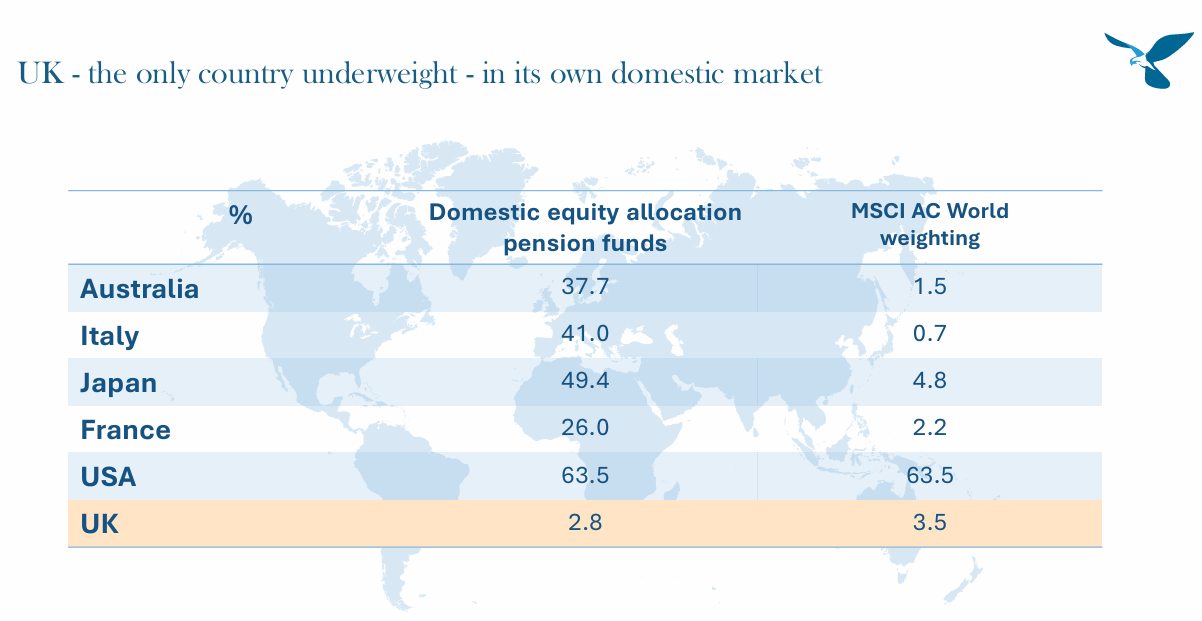

Beagles put this down to there being more sellers than buyers. This has been turbocharged by domestic pension funds, which in 2000 held around 50% of their assets in UK stocks. Today this figure stands at a paltry 2.8%.

Source: JO Hambro Capital Management

“Pension fund allocations in the UK have broadly gone from 50% to almost nothing. Obviously, that's been a very large supply of equity that has been hard to offset and it has left us in this pretty amazing situation where the UK is the only major developed market that is underweight its own domestic equity market,” he said.

As the table above shows, US pension funds’ allocation to their home market is broadly in line with global benchmarks, although Beagles noted that it is hard for them to be overweight given its 65% allocation in the global indices.

The more direct comparison is to other countries of similar stature, such as Australia, where pension funds have nearly 40% in domestic equities versus a 1.5% weighting in the index.

“You can see how significantly different other countries are. They care about their domestic equity market and all the natural benefits that flow from that,” said Beagles.

“In the UK we've just let this happen almost by accident and no politicians or regulators have been prepared to stand in the way.”

His solution is ‘mandation’ – forcing pension funds to invest in UK equities by taking away tax relief if they are not appropriately allocated. This, he said, would be a “sensible route” for the next iteration of the current government to go down, once a new prime minister and chancellor are in place.

“We’re not saying you can't have freedom in where you want to invest, but if you want to get your full tax relief, maybe you should be prepared to have a minimum allocation of some sort to the UK,” said Beagles.

“We're not asking for it to be 40 or 50%, but 10% would make the world of difference to valuations and then companies could get back to a more sensible valuation.”

This is far from the only thing that needs to change, however. A lifting of uncertainty, which has dominated the past decade since Brexit, would also lead to more confidence in the domestic market, said Beagles.

It should encourage retail investors – the other major part of the financial equation – to invest, rather than hoard their savings. The chart below shows the aggregate between savings held in cash deposits and loans. British people have £350bn in net cash, the most we have ever had.

Most of this has gone into cash ISAs, he argued, with between £40bn and £60bn being placed into the tax wrapper over the past three years.

“We're not short of cash or capital, it's just all in unproductive places. That money should be put to work more productively in the economy, rather than stuck in cash ISAs,” he said.

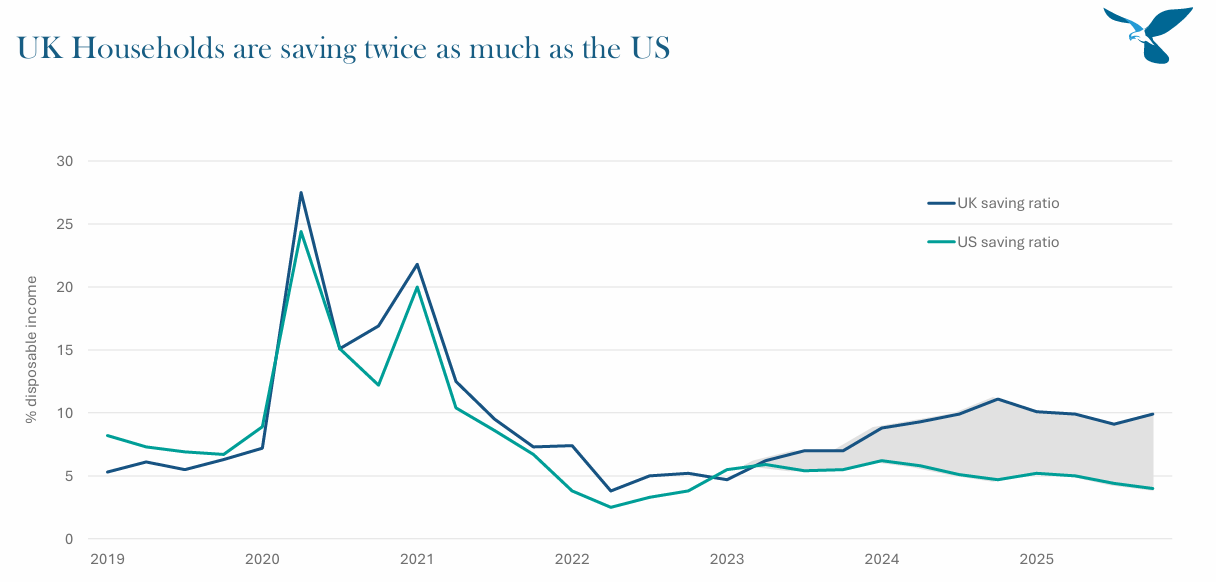

This is the mindset Americans have. The chart below shows UK residents save double the amount of cash as US citizens, who are more likely to invest. This has not always been the case, however.

Source: JO Hambro Capital Management

During Covid, savings went up as people could not spend their cash. Upon the world reopening, this plummeted as people splurged on things they were previously unable to, such as holidays, and the rate dropped below the long-run average.

In the past three years, the US has trended down to near all-time lows while in the UK the savings rate has drifted higher, back towards 10%.

Whether they invest or spend the cash, using this money will be beneficial for UK companies and markets.

“Two-thirds of UK GDP is made up of consumer spending. That's the thing that's going to change the dial – it's not going to be about becoming the next AI superpower or leading the next wave of decarbonisation, but about getting the consumer feeling a bit more confident and prepared to spend some of these excess savings,” said Beagles.

One way to encourage people to invest (or spend) is perhaps to reframe how we view the UK economy. Here, he said the media does not help here, as it “perpetuates a doom loop” that is not always accurate.

The JOHCM UK Equity Income manager acknowledged that economic growth had not been strong, but highlighted that it has grown by almost 15% over the past decade. While this is “not a great number”, it is faster than four of the other G7 countries and only behind the US and Canada.

“The ONS's [Office for National Statistics] initial estimates of GDP tend to start off with a very low number and subsequently get revised higher,” Beagles noted. Over 20 years this has averaged as a 0.39 percentage point increase each year.

“So if the initial estimate put GDP growth at 1%, the actual outcome is 1.4% — that's quite significant. The problem is people don't even read past the headline. They hear GDP this year was 1%, it was rubbish and they don't look at the subsequent revision.”