The European bank trade has bolstered investors’ returns over the past 12 to 18 months – the question is whether this is set to continue.

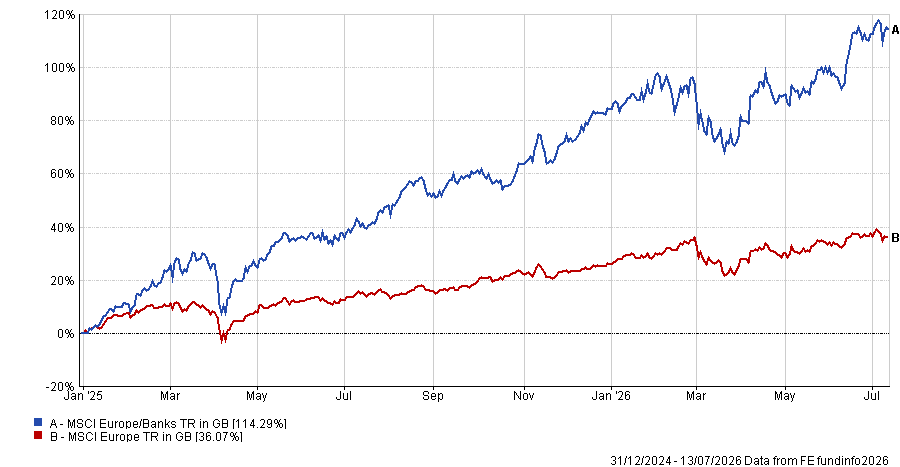

As shown in the graph below, European banks have far outstripped the overall MSCI Europe benchmark since the start of 2025, gaining 114.3% against just 36.1%.

In 2025, European banks’ 84.4% return was far ahead of the 26.1% from the wider index, while they’ve made another 16.5% in 2026 so far, versus 7.9% from the MSCI Europe,

Performance of MSCI Europe/Banks vs MSCI Europe since 1 Jan 2025

Source: FE Analytics

Robert Schramm-Fuchs, portfolio manager on the European equities team at Janus Henderson, describes himself as “very bullish” on European banks.

To explain why, he first pointed out that Europe is in a supportive yield curve environment. “Even though the Iran war has reduced some of the steepness in the yield curve, it is still positively shaped,” Schramm-Fuchs said.

Next, is the absolute level of interest rates.

“We just had an ECB [European Central Bank] hike – even though the hawks want more hikes, the base case is one and done,” he said.

“This leaves us at an absolute interest rate level which is in the Goldilocks window for banks: too low, the business model doesn’t work; too high, you have to worry about economic stress.”

Schramm-Fuchs said the ‘Goldilocks’ window sits around 2-4% for short-term interest rates. The current interest rate set by the ECB is 2.4%.

European banks are also seeing supportive revenue trends, he noted, with loan volumes growing modestly and fee income rising as more savers shift money out of deposits and into investment products – a trend that policies like Germany’s pension reform are accelerating.

Meanwhile, the cost of bad loans remains very low because European borrowers have materially paid down debt since the 2008 financial crisis, leaving banks with a higher quality loan book, he said.

Benjie Creelan Sandford, associate manager of Algebris Financial Income and Algebris Financial Equity, is also bullish on European banks, noting they have been “a huge relative and absolute overweight position over the past few years”.

He noted that the sector presented an “extremely attractive value opportunity” coming out the other side of Covid, as Europe moved into a higher inflation environment.

“We had a view as to what that would mean for interest rates, coinciding with fundamental factors that were turning around for European banks – a 180-degree pivot versus the period from post-GFC [great financial crisis] through to 2020.”

Valuation-wise, Creelan Sandford thinks European banks still have space to run.

“We still don't think the sector is expensive. We still think medium term, given the fundamentals, you can compound that value over time. It is still a very attractive investment proposition,” he said.

“But clearly European banks now trading at 10x P/E versus two or three years ago when they were trading at 6x P/E means the valuation is not quite as attractive as it was, which is why we have pared back the extremity of our positioning and taken up positioning elsewhere in the financial allocation.”

At its peak, European banks made up over 40% of Algebris Financial Income, he said, noting that these stocks continue to be the single largest position in the fund but they have now been cut to around 25%.

That is not to say that Creelan Sandford expects European banks to move from 10x to 15x going forward.

“The reality is you don’t need to believe that to think banks continue to create value,” Creelan Sandford said, noting that he focuses positioning on a bank’s steady compounding of value.

“When I look at the dividends I am getting paid, total distribution yields for the sector are still around 7-8%, so still incredible yield, while cash dividends are around 5-6% and then there is 2-3% on buybacks on top,” he said.

“If I look at the dividends I am getting paid plus the good value growth that banks are generating – given the strong profitability underpinnings – that is around 15% per annum total shareholder return. That’s not a bad place to be as a starting point.”

Schramm-Fuchs also expects European banks to continue to be a core driver of returns in his portfolios.

“We are still at a valuation discount in price-to-earnings (P/E) terms and still at a valuation discount to the history of European banks,” he said.

“That history has been very chequered: it was a history of extreme leverage pre-financial crisis and then a history of rising share count after the financial crisis because balance sheet health needed to be restored and leverage needed to be dramatically reduced.”

Regulatory ceiling

However, while conditions are good for European banks, Schramm-Fuchs noted that over-regulation threatens continued growth.

He said that the bloc has “the most rigid and intense banking regulation in the world” while simultaneously having one of the highest degrees of reliance on bank lending.

“This reliance on bank lending, combined with forced deleveraging, has meant that, macroeconomically, Europe is not doing as well as it could – but, at the micro level, for banks, it has meant we have been through all the exposures with a fine-tooth comb. There is no bad debt in the system – there cannot be.”

This is, however, hindering the sector’s growth potential, Schramm-Fuchs said. For example, he highlighted how many European banks are eager to integrate new software and AI-powered capabilities to become more efficient but are limited.

In particular, he is concerned that this “ongoing regulatory creep” is keeping European banks from achieving a level playing field with banks in other regions, such as the US, which promote deregulation and therefore have more ability to innovate and grow earnings.

“Despite their quality, you have to go down to the most challenged banks among the US regionals to find any trading at the same low earnings multiples as European banks. It doesn’t make any sense,” said Schramm-Fuchs.

Indeed, Schramm-Fuchs said an apples-to-apples comparisons suggests that, if assessing the core tier one ratios of European banks versus US banks and adjusting them to the same regulatory standards, “European banks would hold 100 to 150 basis points more capital than their US counterparts”.

He therefore concluded that there is “very clearly a ceiling to European banks due to regulation”.

“If your growth is limited, there is a ceiling to how much re-rating you can get,” he said.