Rathbone Global Opportunities manager James Thomson expects stock market gains to spread beyond artificial intelligence and memory chip stocks in the second half of 2026, so has adjusted the £3.2bn portfolio's holdings ahead of that shift.

Key AI holdings such as Arm Holdings, CrowdStrike, Amphenol and Alphabet were among the fund's strongest performers in the second quarter of 2026. FE fundinfo Alpha Manager Thomson attributed their continued momentum to persistent macroeconomic pressures, but he thinks those pressures may now be turning.

"We're anticipating market performance broadening beyond the AI and memory chips basket, potentially triggered by a fall in oil prices and easing in the hawkish tilt by central banks – especially if inflation moves lower," he said.

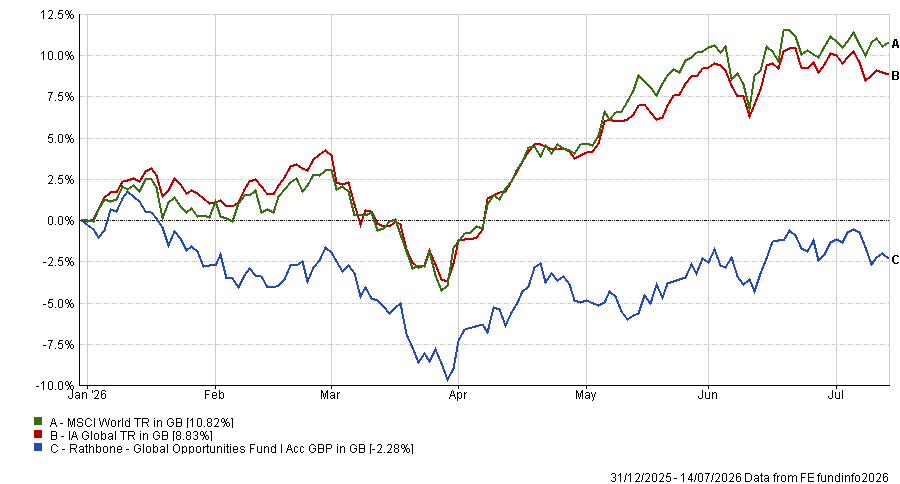

Performance of Rathbone Global Opportunities vs sector and index in 2026 YTD

Source: FE Analytics. Total return in sterling between 1 Jan and 14 Jul 2026

He added that the Iran conflict continues to be priced in and out of investor assumptions, creating volatility around this broader trend.

Thomson pointed to several macroeconomic indicators that rose in the second quarter and could reverse course: oil prices, inflation, inflation expectations, bond yields and central banks' rate projections. He thinks his portfolio might benefit if these indicators start to fall.

"Our zero exposure to oil and gas, due to its unpredictable growth qualities and price-taking characteristics, was a headwind during the war of H1 but it could become a tailwind in this scenario," he said.

As the chart above shows, Rathbone Global Opportunities has underperformed both its average IA Global peer and the MSCI World index since the start of 2026. Its 2.3% loss over this period puts it in 543rd place out of 576 funds in the peer group.

Thomson pointed out that the fund is not retreating from the AI theme, distinguishing between stocks exposed to capacity shortages, which he considers less durable, and companies he sees as structural beneficiaries of AI infrastructure build-out.

"We are not AI naysayers – in fact, we have many AI beneficiaries from GPUs to CPUs, hyperscalers, networking, data centre real estate, grid modernisation and power infrastructure construction and equipment," he said.

Nvidia, Arm and CrowdStrike, a recent addition, now sit among the fund's 10 largest holdings and provide exposure across different parts of the AI supply chain.

But in looking outside of this theme, Rathbone Global Opportunities has “bought more new stocks so far this year than at any similar point in the past”. Alongside these purchases, Thomson has sold consumer-facing software holdings including Intuit, along with information services and private equity positions, on concerns that AI-driven competition could erode their growth rates.

Much of the new buying has gone towards stocks in the 'HALO' theme (hard assets, low obsolescence). He introduced it in response to what he sees as elevated obsolescence risk – or the risk that a process, product or technology will become obsolete – across industries.

New additions include electrical infrastructure contractor Quanta, aerospace contractor Howmet, mining equipment supplier Sandvik and construction equipment maker Caterpillar, joining motion control technologies firm Parker Hannifin and fibre-optic products maker Amphenol, both existing holdings. Thomson made two further unnamed HALO additions.

The manager links this theme to a broader expectation that resource independence and protectionism will shape markets over the coming years, as major economies compete for the critical minerals needed for technology and electrification infrastructure. Despite that view, Thomson avoids direct exposure to commodity producers.

"We remain wary of investing in pure commodity stocks as they are often at the mercy of a single commodity price and have high project risk. We have taken a less risky picks n' shovels approach," he said.

Thomson has also used recent volatility in software stocks to add to positions he considers mispriced. CrowdStrike fell during a broader sell-off in software shares, which he attributes to fears about AI-driven disruption, but he expects the business to benefit from rising demand for cybersecurity as AI adoption spreads.

Separately, energy drinks maker Monster Beverage and cosmetics business L'Oréal have been added to the fund to bolster its defensive holdings, aiming for growth less tied to technology sector swings.

Thomson said this repositioning is a trade-off between short-term and long-term returns. He expects that giving up exposure to the fastest-growing but potentially unsustainable stocks will support performance once market gains broaden out.

"Forgoing returns in stocks with supernormal (but fleeting) profit growth may be painful in the short term, but it will protect us in the longer term," he said. "Our balanced and diversified approach to portfolio construction will drive outperformance as the market broadens beyond this single theme. Meanwhile, we are using the bifurcation as a rare opportunity to buy watchlist stocks."