In the world of investing, capital appreciation – the increase in the market value of an asset - tends to capture the headlines, for example Nvidia becoming the world’s largest company or Apple announcing a record fiscal quarter after the launch of the iPhone 17.

The drama of soaring share prices or the rapid growth of a technology giant makes for compelling reading but it often obscures the engine that drives the minority of long-term wealth creation: dividend reinvestment.

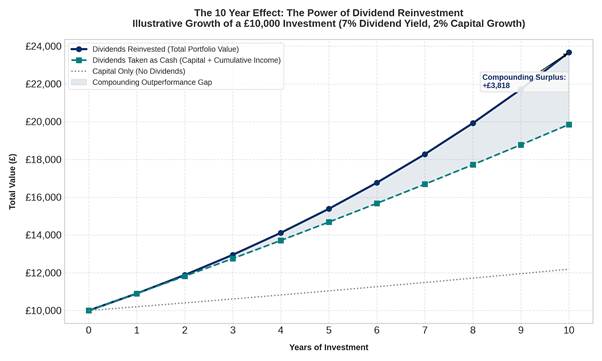

When looking across a standard investment horizon, there is a mathematical tipping point where the composition of total return shifts. We call this the 10-year effect. And at this point, investors often have a choice to make.

The choice to take cash or reinvest the dividend

During the first few years of an investment lifecycle, the impact of choosing to reinvest dividends rather than taking them as cash can feel almost negligible. It is a linear progression, a modest accumulation of fractional shares that sits in the shadow of broader market movements.

However, as an investor approaches the decade mark, the geometry of compounding begins to assert itself. The income generated by the accumulated shares begins to create a snowball effect that structurally transforms the risk and return profile of a portfolio. Over a ten-year period, this process can effectively double the share count of a high-yielding vehicle, significantly lowering the average cost basis and insulating the investor against capital volatility.

This compounding engine becomes particularly potent in the current macroeconomic climate. With traditional fixed-income markets grappling with duration risk and equity markets exposed to shifting growth forecasts, the value of a reliable, high-yielding income stream is amplified.

The philosophy of a vehicle like CVC Income & Growth, which focuses on senior secured floating-rate corporate credit, is aligned with this long-term compounding dynamic. Because floating-rate assets adjust their coupons upward alongside base rates, they generate a consistently high level of distributable income without the capital erosion that plagues fixed-rate bonds when yields rise.

This means that during periods of market stress, the fund is effectively throwing off more fuel for the compounding engine, precisely when underlying asset prices may be suppressed, allowing automatic reinvestment to capture mispriced value at a discount.

Beyond the maths, this reinvestment principle also introduces a critical behavioural discipline. Reinvesting distributions removes the temptation to time the market, replacing emotional decision-making with the process of pound-cost averaging.

In a market with rapid swings in inflation expectations and central bank policy, consistency becomes an alpha generator. By automatically recycling distributions back into the market, investors transform volatility from an operational risk into a structural tailwind, using short-term price pullbacks to accelerate their long-term share accumulation.

Small steps for long-term gains

The journey toward a transformed ten-year horizon is built on immediate, incremental actions. The decisions made during these regular quarterly windows may seem small in isolation, but they represent the foundational building blocks of long-term wealth, proving that the most reliable path to financial resilience is not predicting the future but methodically reinvesting in the present.

The illustration below models the geometric reality of reinvesting dividends over a 10-year period, based on a standard £10,000 initial investment, a high-yielding 7% dividend distribution and a conservative 2% baseline capital growth rate.

Source: CVC Credit Partners

Pieter Staelens is lead fund manager of CVC Income & Growth. The views expressed above should not be taken as investment advice.