The Magnificent Seven as a group have lost more than 20% since Christmas eve, meaning they have technically entered bear market territory, judging by UBS’s market-cap weighted Mag7 index.

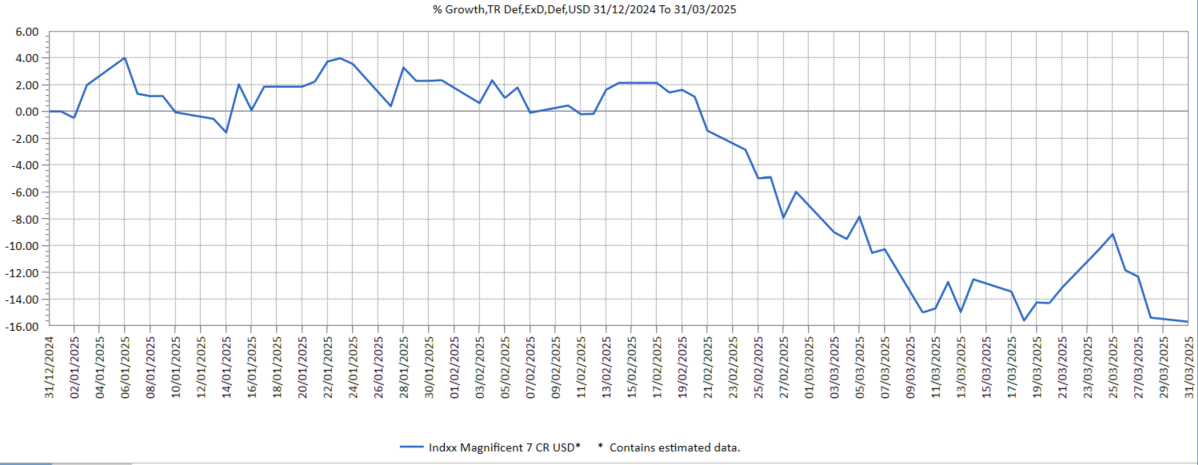

Other measures paint a similar, although slightly less dire, picture. The equally-weighted Indxx Magnificent Seven index is down 15.7% since Christmas eve in dollar terms, as the chart below shows, although in sterling terms it has lost 18.2%.

As Jason Hollands, managing director of Bestinvest, pointed out: “While that is painful for anyone who invested at the start of the year, to put this in context, the index is back at where it was last September.”

Performance of Indxx Magnificent Seven, year to date

Sources: Bestinvest, Lipper

The Bloomberg Magnificent 7 Total Return index, another equal-weighted benchmark, is down 16% year to date in dollars. “It is not far off bear market territory but not quite there yet,” Hollands said.

The underperformance of the Magnificent Seven this year is notable against wider equity markets but also versus the technology sector, said Matt Ward, portfolio manager, technology at AXA Investment Managers.

This marks “a real reversal of what we’d seen throughout 2023 and 2024; on an equal-dollar weighted basis, the Magnificent Seven are still up 40% versus the MSCI ACWI Tech Index over the past 24 months”, he observed. “Behind these headline numbers though we see real nuance within the group with a wide dispersion of stock performances, valuations and the fundamental drivers that vary significantly between them.”

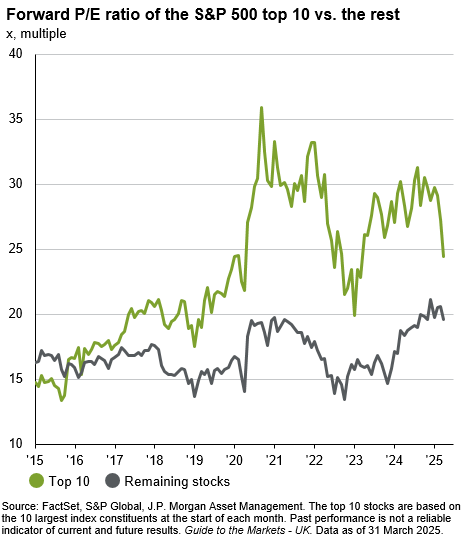

Looking at a slightly longer list of US mega-caps, the 10 largest stocks in the S&P 500 have been playing ‘catch down’ with the rest of the market, closing the valuation gap significantly in recent months.

Below, Trustnet asked experts how investors should react to the sharp sell-off in mega-cap tech stocks this year. Should they move out of specialist tech funds in case the rout worsens or is now the time to pile back in?

This could be a buying opportunity, especially if prices ease further

Darius McDermott, managing director of Chelsea Financial Services, sees the sell-off as a potential buying opportunity. “Artificial intelligence is not a passing trend and the Magnificent Seven have invested billions into research and development in this area. They remain well placed to lead the next wave of innovation,” he explained.

“While valuations were stretched, the long-term growth story remains intact. These are high-quality businesses with strong margins and robust cashflows. If prices ease further, that could present an attractive entry point for funds specialising in the technology trends.”

That said, what investors should do from here depends on what they already have in their portfolios. “It’s crucial to understand how much exposure you already have to the Magnificent Seven, especially through global or US equity funds. These stocks recently made up around 37% of the S&P 500, so many investors may already be overweight without realising it. While the US remains a hub of innovation, recent market volatility has underscored the importance of diversification,” McDermott cautioned.

For investors who want exposure to tech stocks overseen by a specialist, McDermott suggested Sanlam Global Artificial Intelligence and Allianz Technology Trust.

“Sanlam Global Artificial Intelligence takes a differentiated approach, ‘eating its own cooking’ by using a proprietary AI system to help identify companies poised to benefit from the AI theme. Importantly, the manager does not just look at firms creating AI, but also those using it to enhance their business models – offering investors a more diversified route into this rapidly evolving trend,” McDermott noted.

“Allianz Technology Trust is managed by the experienced Mike Seidenberg, supported by a specialist team based in Silicon Valley. This gives them unrivalled access to companies at the heart of global tech innovation.”

Hold your horses and stay the course

Rob Morgan, chief investment analyst at Charles Stanley, said investors should cleave to well-established investment principles such as diversifying appropriately and committing for the longer term.

“The extent of uncertainty and complexity around tariffs and the consequences for individual companies means, in the short term, we can expect a high level of market volatility. However, the era of US exceptionalism may persist once we get past the short-term difficulties,” he said.

Despite near-term risks, the tech sector is still home to structural winners. “In the main, the big tech giants are fantastic businesses – it can be argued some of the most successful in history – so there is always going to be a place for such businesses in portfolios if they are priced appropriately,” Morgan observed.

“This year's sell-off has blown the froth off valuations and, in time, could lay the foundations for decent returns. As a result, this is an opportunity to rebalance back towards this area if your portfolio has been lacking in it or sticking the course as long as you are not over-exposed.”

Alison Porter, co-manager of Janus Henderson Investors’ Global Technology Leaders and Sustainable Future Technologies strategies, also expects short-term volatility but said the long-term investment case remains intact.

“We believe we are still in the early stages of an artificial intelligence (AI) compute wave that requires investment across the technology stack, as physical infrastructure needs to be upgraded before we see truly transformational applications emerge,” she said.

“While the coming months will be volatile, long-term we remain positive on the companies with hyperscale (public cloud) platforms which can help to propel and facilitate the development of new applications disrupting new sectors, such as healthcare and transportation.”

Time to diversify away from mega-cap tech

The market correction, although severe, has not brought mega-cap tech valuations down to attractive levels yet, Hollands said. “Lower share prices have taken some of the froth out of what were very extreme valuations but it would still be stretching to claim they are now a screaming bargain.”

Many investors already own the Magnificent Seven through passive funds tracking US and global equity indices, which have become heavily exposed to the tech giants. Therefore, “the bigger issue for many people will be to diversify beyond them”.

That said, Hollands does not advocate knee-jerk selling on short-term market movements. Besides, it remains to be seen whether the Magnificent Seven will remain in a trading range, recover or experience another leg downward, he said.

“Tech is going to remain an important sector and so if you invested in it on a long-term view, then you should probably not get distracted by short-term volatility.”

That said, investors who want to diversify could switch some US equity exposure to equally weighted index funds such as Xtrackers S&P 500 Equal Weight UCITS ETF.

“Other options include factor funds, such as the Invesco FTSE RAFI US 1000 UCITS ETF, which owns the 1,000 largest companies but weights them based on average sales, cashflow and dividends over the past five years, as well as book value, which provides the portfolio with an implicit value tilt and mutes Magnificent Seven exposure without eliminating it entirely,” he explained.