Global investors are misreading where risk and opportunity now sit, according to Guinness Asset Management, as the economic and geopolitical regime that dominated markets for two decades has broken down.

“Diversification today is less a choice – it is becoming a real necessity,” said Valerie Huang, Asia and emerging markets portfolio manager at Guinness. “The world that worked for portfolios for 20 years simply doesn’t exist anymore.”

For much of the past two decades, markets operated under a stable macroeconomic regime of low inflation, cheap capital and broadly credible policy frameworks. Equity returns were driven less by profits and more by falling discount rates and valuation expansion. Huang argued that this world has ended.

Governments are now more activist on spending, taxation and industrial policy; resource security has re-emerged as a priority; and supply chains and alliances are shifting, resulting in more policy noise, greater inflation risk and rising market concentration.

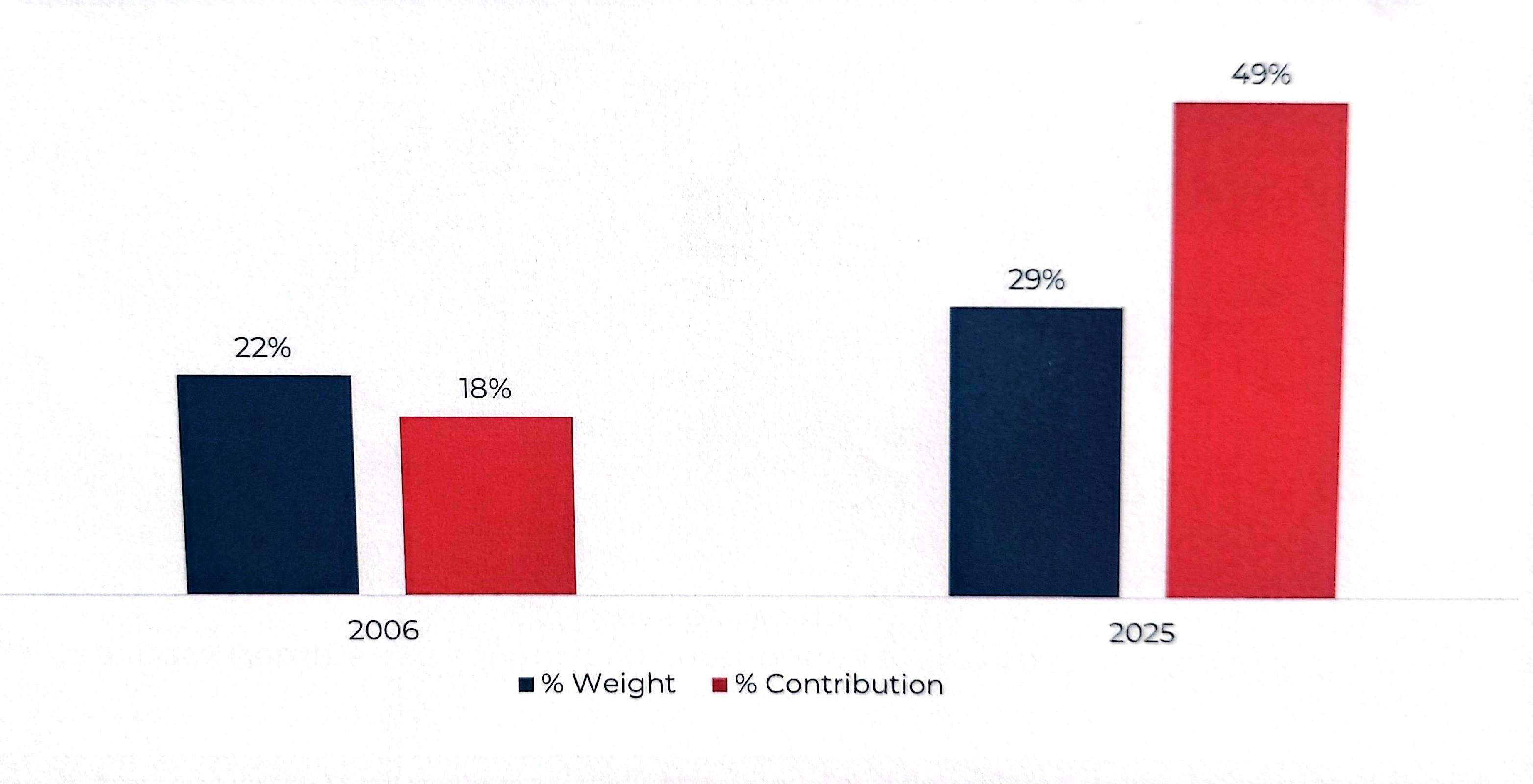

Top 10 MSCI AC Asia Pacific ex Japan names by weight and contribution to the total return of the index

Source: MSCI, Bloomberg, Guinness Global Investors.

Concentration, which investors may be used to seeing in the US, is visible in Asia too. The chart below shows how the top 10 names in the MSCI AC Asia Pacific ex Japan index accounted for just under 30% of the benchmark last year but contributed close to half of its returns. This means index risk is no longer evenly spread and simple regional exposure is less diversified than it appears.

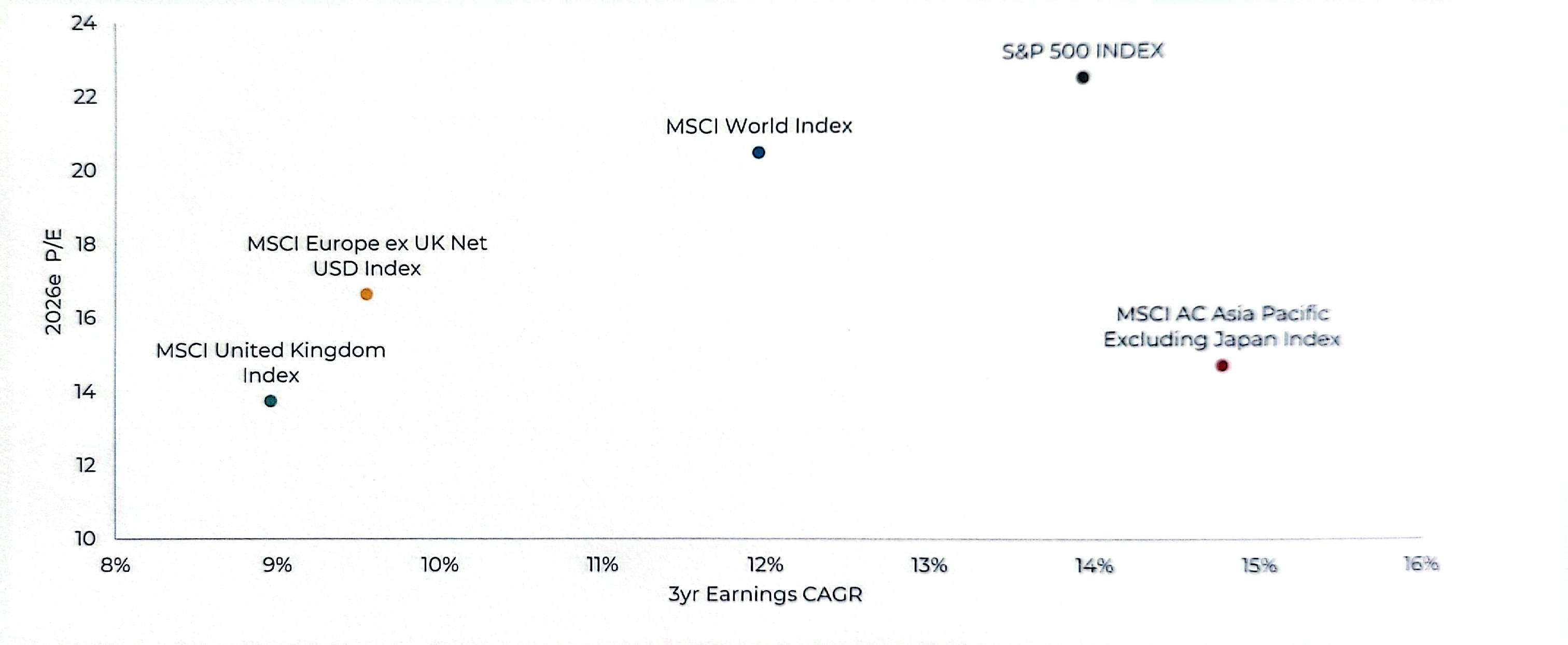

However, prices are more favourable in Asia, as the chart below shows.

Against that backdrop, Guinness argued most global investors misplace risk by treating the US as the “safe” pole and China as the dangerous one.

Three-year earnings compound annual growth rate

Source: MSCI, S&P 500, Guinness Global Investors

Edmund Harriss, head of Asian and emerging market investments at Guinness, said: “The US is looking backwards”, prioritising things that “would ‘make America great’ in the sixties” such as fossil fuels and legacy industries. China, by contrast, is positioning for the 2040s and beyond through electrification, renewables and advanced manufacturing.

Because of this, Harriss argued that China can “sit this one out” in today’s geopolitical noise, trying “not to interrupt the enemy while they’re making a mistake” while at the same time building supply chains, controlling large parts of the renewable energy value chain and exporting electric vehicles that are increasingly visible on Western roads.

Portfolio manager Sharukh Malik said Beijing intentionally deflated its property sector after years of excess, accepting slower growth to reduce financial risk. That drag is now fading.

Growth is being rebuilt around electric vehicles, semiconductors, automation and advanced manufacturing, a shift Malik expects to become clearer towards the end of this year or early 2027.

“People look at what went wrong in China over the past five years and assume that is all China is,” Malik said. “They miss what is being built underneath”, such as drone delivery networks in Shenzhen, the rapid adoption of electric heavy trucks and advances in industrial robotics that are being deployed across factories. The picture is of an economy that is becoming more innovative and more export-competitive, he argued.

This is also where the contrast with the UK enters the debate. Harriss noted that while China’s industrial base is expanding into higher-value sectors, the British economy is no longer the engine it once was – a reminder that “developed” status does not guarantee structural strength.

At stock level, Guinness’ Asia and emerging markets portfolio manager Mark Hammonds described how his team targets quality businesses with competitive advantages, high returns on capital, reliable cashflows and disciplined position sizing.

Elite Material, a Taiwanese producer of advanced printed circuit board laminates, illustrates the approach. The company was not bought for exposure to the artificial intelligence (AI) theme, but benefited from successive demand cycles in consumer electronics, cloud computing and high-performance AI hardware because of its dominant position in environmentally friendly materials.

Haier Smart Home shows how Chinese manufacturing standards have moved up the value chain, now competing across price points in developed markets while also serving the rising appliance demand that accompanies income growth in emerging markets.

Bajaj Auto in India highlights a different trend: emerging market-to-emerging market trade with a new plant in Brazil.

“This is an interesting example of a company based in an emerging market, India, but serving a different emerging market customer in Brazil,” Hammonds said. “So you’ve got EM-to-EM trade happening, and for the first time bypassing developed markets altogether.”

There is one risk that concerns Guinness more than geopolitics or China’s property market: the global AI capex cycle. Hammonds warned that capital expenditure on AI infrastructure is rising in a smooth, almost linear fashion, while revenues historically arrive in steps.

That gap creates periods when investors question whether returns will materialise quickly enough to justify current spending levels. When valuations are stretched, tolerance for disappointment is low.

“The spending keeps going up in a straight line, but the money comes back in lumps,” he said. “That is where markets get uncomfortable.”

Recent volatility around Microsoft reflected this tension. In Asia the profile looks steadier because much of the manufacturing and component supply sits there, but the underlying risk remains global.

In the near term, large-cap Asia has performed strongly. If conditions stay benign, Hammonds expects attention to move further down the market-cap spectrum, where many mid-sized companies have yet to rerate despite solid fundamentals.

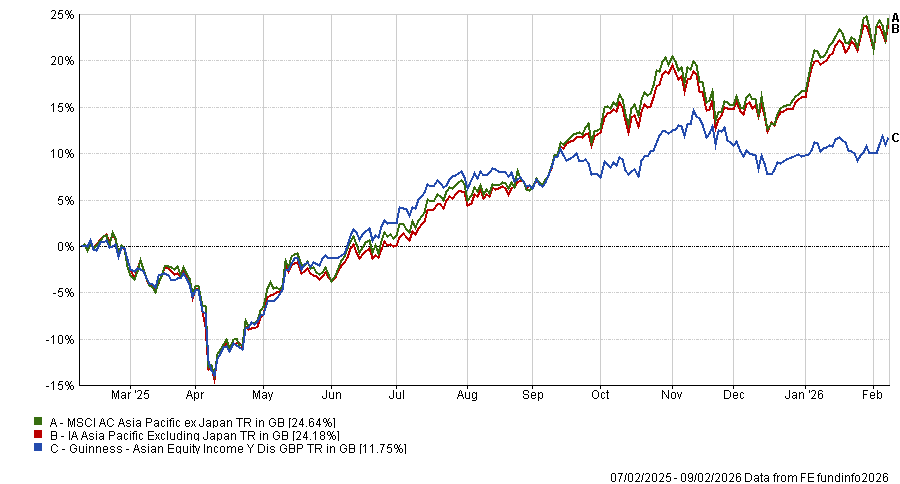

The managers run the Guinness Asian Equity Income fund, a first-quartile performer in the IA Asia Pacific Excluding Japan peer group in 2021, 2023 and 2024. Last year, it underperformed the rest of the market, as the chart below shows.

Performance of fund against index and sector over 1yr

Source: FE Analytics