After years of lagging developed markets, emerging market equities staged a powerful recovery in 2025 as they benefited from a perfect storm of dollar weakness (which eased financial conditions) and improving terms of trade as commodity prices recovered due to growing demand from the artificial intelligence (AI) surge.

In addition, many emerging market central banks raised interest rates early in the post‑pandemic inflation shock, which has given them the space in 2025 and 2026 to cut while developed markets such as the US and Europe remain more constrained.

Rebekah McMillan, associate portfolio manager at Neuberger Berman, said: “As a result, last year proved that emerging markets cannot be ignored as part of a multi-asset portfolio.”

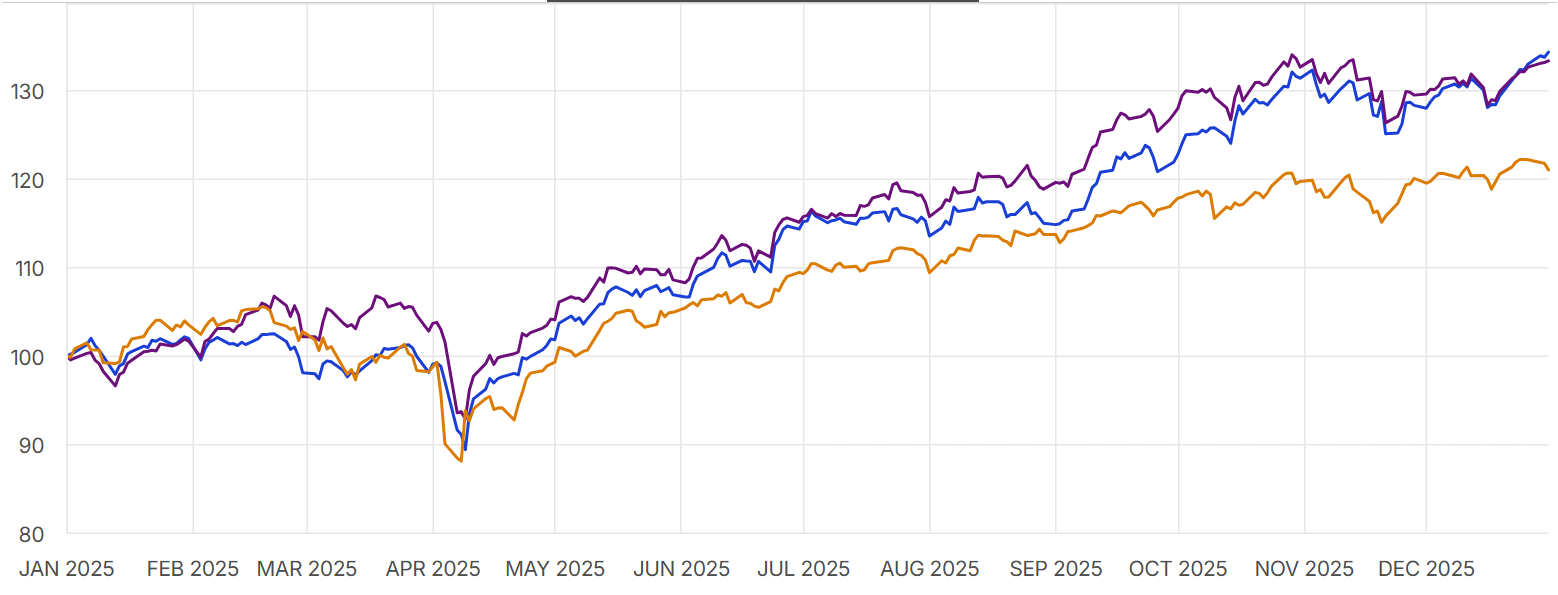

This is further supported by the numbers, with the MSCI Emerging Markets index outperforming the developed market MSCI World, up 33.6% in 2025 and 21.2% respectively, according to data from MSCI.

Performance of MSCI Emerging Markets (purple), MSCI Emerging Markets ex China (blue) and MSCI World (orange) in 2025 (USD)

Source: MSCI

In the past, China has been the main driver of emerging market performance as its economic cycles heavily influenced commodity demand and regional growth, Wolf von Rotberg, equity strategic at J. Safra Sarasin Sustainable Asset Management said. As a reflection of the country’s influence, China made up 40% of the MSCI Emerging Markets index in 2020.

In more recent years, China has struggled with regulatory crackdowns, property sector weakness, debt issues and slowing growth. As a result, China’s weighting in MSCI Emerging Markets dropping to around 25%.

As shown in the graph above, last year the MSCI Emerging Markets ex China index outperformed MSCI Emerging Markets, gaining 34.6% in 2025.

Von Rotberg said: “The interesting observation is that emerging markets can work and outperform without China. MSCI Emerging Markets is no longer as dependent on what China is doing.”

Against this backdrop, fund managers highlight a group of countries beyond China – notably Korea, Taiwan and Brazil.

South Korea

AI-related emerging market stocks, particularly in Asia, are outperforming, yet their valuations remain much lower than those of developed market peers, with emerging market companies focused on hardware benefiting from stronger pricing power, better demand visibility and steadily improving earnings momentum.

One of the Asian markets that has caught fund managers’ interest in the AI race is South Korea. Tom Kynge, multi-asset portfolio manager at Sarasin & Partners, said: “We like that it offers exposure to semiconductors and memory storage [for use in AI].”

Von Rotberg said that 2026 will be “just as strong” for South Korea as 2025 was, with the US hyperscalers set to once again hike their AI-focused capex – therefore keeping up demand for chips and memory storage.

But Karnail Sangha, co-manager of Robeco Emerging Stars Equities, also likes South Korea for other themes. “For example, it is housing one of the best defence equipment and manufacturing companies [Hanwha Aerospace] at a time when geopolitical risks are rising and such companies are seeing an increase in their order books,” he said.

“The South Korean government is also pushing companies to do better capital allocation and improve corporate governance in order to get rid of the discounts in Korea that we are seeing now.”

Taiwan

The AI build out has also notably benefited Taiwan, with TSMC thriving thanks to its dominance in advanced chip manufacturing and its central role producing the high‑performance processors used by the likes of Nvidia and Apple.

McMillan said: “We have also been positive on Taiwan and performance has been exceptional. When looking at the forward-looking indicators, the patent filings and capital spending is still strong – so the momentum is there – which means we expect further growth for the region.”

In contrast, although he still sees the benefits of investing in the region, Sangha said he is choosing to exercise more caution with his value-tilted fund.

“Valuations have become less attractive to us, so we are a bit more cautious there,” he said. “We are nonetheless still positioned in TSMC which continues to outperform.”

Brazil

The fund managers said that Brazil offers an appealing mix of easing inflation and the possibility of rate cuts ahead.

“Brazil is a market we like and we expect falling inflation to allow interest rates to fall too,” said Sangha. “But, in the background, there is still excessive fiscal spending that needs to change.”

The October 2026 presidential election also introduces potential change, he noted, with the more market‑friendly Flavio Bolsonaro posing a challenge to incumbent Luiz Inácio Lula da Silva.

McMillan added: “We like Brazil for both equities and debt, given that it has high real rates but the commodity exposure could be a boost to corporates and earnings there.”

Don’t rule out China

Despite the shift in focus to other emerging markets, the fund managers stressed that China still offers selective opportunities, particularly in areas supported by policy or linked to structural growth themes.

Kynge said: “China is the elephant in the room and remains a tricky one to navigate. On the one hand, there are incredible companies and there is some incredible technological innovation happening there. On the other hand, there is an overt suggestion from the government that it is not on the side of investors. It is not a capital first environment.”

However, he said that there continues to be a huge amount of innovation from select companies in China, meaning there is real opportunity for those willing to look.

Sangha agreed, noting that there “is still a lot of room for stimulus, with structural growth sitting somewhere between 4% and 5%”.

“You still have to be very selective about where you want to be – the old economy sectors are ones to avoid,” he said. “We like renewables and AI, as well as consumer facing companies.”