The US market’s 2025 performance cannot be summed up in a single storyline, with two very different narratives unfolding in parallel.

On the one hand, it enjoyed the swell of investment from those looking to dive into the artificial intelligence (AI) build out. On the other, the market was buffeted by increased volatility from the White House – from the introduction (and withdrawal) of tariffs, to squabbling between the president and Federal Reserve chair on interest rates, sticky inflation and geopolitical tensions.

As such, just as AI enticed more investors to back a select number of US stocks, macro concerns drove others to hunt for more defensive and value assets.

Against this backdrop, the IA North America sector delivered a modest 7% return over the year, with funds that have enjoyed years of strong performance in a growth-tilted US market finding 2025 much more difficult.

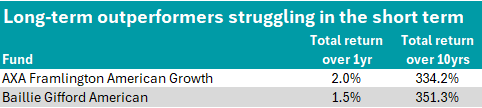

And it was this changing market regime that caught out long-term leaders Baillie Gifford American and AXA Framlington American Growth, which made just 1.5% and 2% respectively in 2025.

Source: FE Analytics

As shown in the table above, the £2.1bn Baillie Gifford American fund has a much stronger long-term performance, gaining 351.3% over 10 years – placing it in the first quartile in the sector over that time period.

Run by FE fundinfo Alpha Manager Tom Slater, alongside Gary Robinson, Kirsty Gibson and Dave Bujnowski, the strategy is a high-conviction, bottom-up portfolio of 30 to 50 growth stocks held with a long-time horizon.

Such concentrated exposure to fast-growing and disruptive companies means performance is driven heavily by a smaller number of high-impact stocks – for good or for bad.

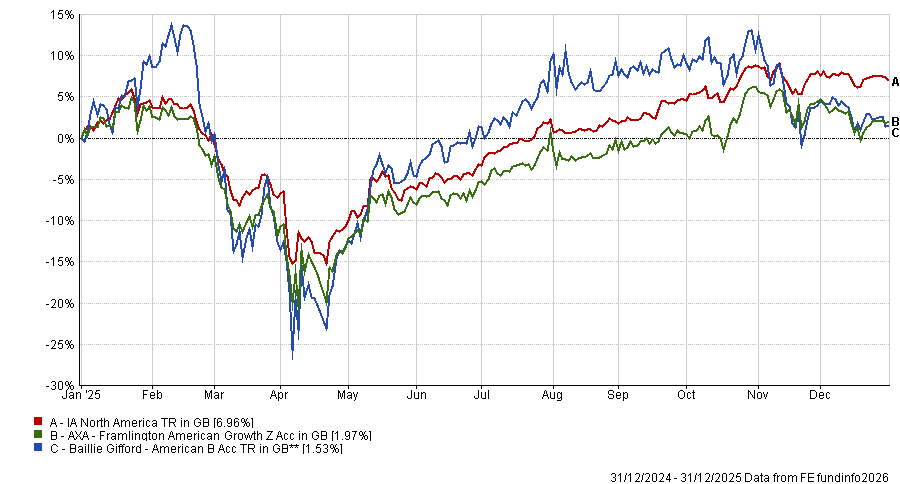

In 2025, this proved to be a headwind, as some of the fund’s largest holdings lagged, with the management team highlighting notable detractors in its end of year report: video game developer Roblox, language learning platform Duolingo and media streaming platform Netflix.

Management said Roblox underperformed due to a sharp increase in AI-related investment, which pressured near-term profitability despite strong underlying growth.

Meanwhile, Duolingo suffered from a de-rating after fourth quarter bookings guidance came in below consensus. Finally, Netflix detracted as a one-off Brazilian tax change overshadowed its otherwise solid revenue and cashflow growth, alongside ongoing uncertainty surrounding the proposed Warner Bros acquisition.

Similarly, AXA Framlington American Growth has made huge gains over 10 years, posting a 334.2% return over the decade. In the shorter term, its growth tilt and structurally lower exposure to outperforming large-cap US names detracted from its 2025 performance.

Managers David Shaw and Gordon Happell monitor top-down themes and macroeconomic conditions but their investment decisions are primarily driven by bottom-up company analysis.

As such, the fund invests in high-quality growth companies they believe have strong competitive advantages, while avoiding those that rely on cost-cutting, financial restructuring or excessive borrowing to boost earnings.

Like the Baillie Gifford fund, the AXA portfolio is more concentrated, with a range of 65 to 95 holdings.

Performance of funds vs sector in 2025

Source: FE Analytics

While these long‑term growth leaders struggled, a very different picture emerged among several of the sector’s long‑term laggards, which were buoyed by the 2025 market environment.

Source: FE Analytics

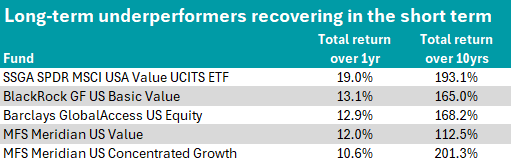

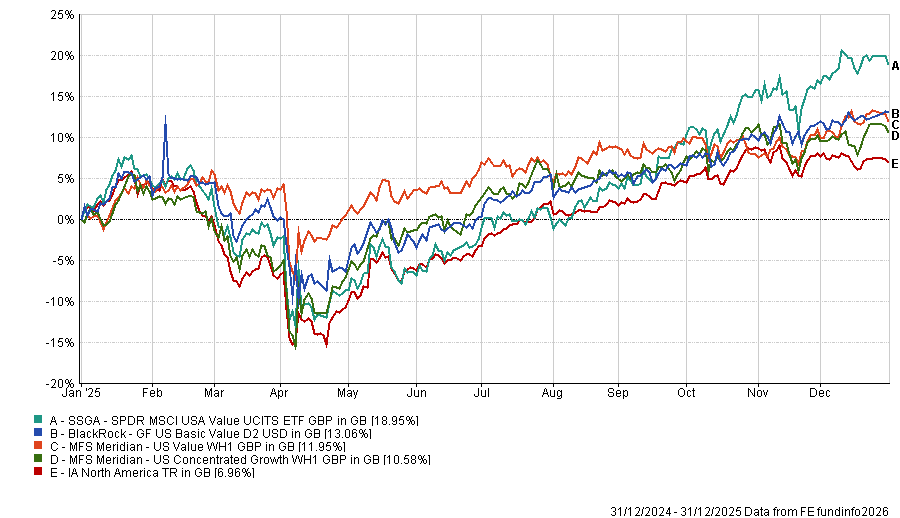

Top of the table is SPDR MSCI USA Value UCITS ETF, which delivered a first quartile return of 19% in 2025, despite its weaker long-term record.

The $190m fund tracks the MSCI USA Value Exposure Select index, giving it a systematic tilt toward lower‑valued US companies. Its largest positions include Micron Technology, Applied Materials and Cisco, with the portfolio leaning most heavily toward information technology, financials and consumer discretionary stocks.

Meanwhile, the $893m BlackRock GF US Basic Value fund returned 13.1% over one year and 165% over 10 years. The fund uses the Russell 1000 Value index as a reference point, targeting undervalued companies, with top holdings including Wells Fargo, Citigroup and SS&C Technologies.

MFS Meridian Funds had two funds in the IA North America sector which posted fourth quartile returns over 10 years and first quartile returns over one year.

The $2bn MFS Meridian US Value fund is managed by Nevin Chitkara and Katherine Cannan and follows a traditional value approach, seeking high-quality and attractively valued large-caps offering downside protection. It made a 12% gain in 2025.

The fund is overweight financials, industrials and healthcare and is underweight information technology stocks relative to the Russell 1000 Value index.

MFS Meridian US Concentrated Growth returned 10.6% in 2025 and 201.3% over 10 years. Through its focus on high-quality and durable large-cap growth companies co-managers Jeffrey Constantino and Joseph Skorski expect to compound returns over long periods.

Although the portfolio is underweight the information technology sector relative to the Russell 1000 Growth benchmark, with a greater allocation to financials, its top holdings include notable mega-cap tech names, such as Nvidia and Microsoft.

Performance of the funds vs sector in 2025

Source: FE Analytics