Global equity income funds blend reliable dividend payments and worldwide diversification, qualities proved especially appealing in 2025, when sharp style rotations and renewed demand for stability left investors seeking shelter from volatility.

In the face of such uncertainty, the IA Global Equity Income sector remained relatively steady, with funds in the sector managing an average return of 12.7% in 2025.

Beneath the sector’s relatively calm exterior, the year delivered some unexpected standouts, as funds that lagged for much of the past decade suddenly benefited from the changed market regime.

Source: FE Analytics

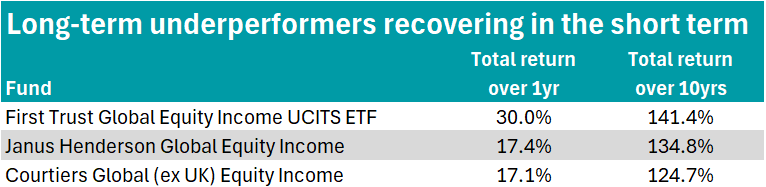

First Trust Global Equity Income UCITS ETF surged to the first quartile of the sector over one year, gaining 30% in 2025. This wasn’t enough to impact its long-term returns, however, as it achieved a fourth quartile 10-year performance of 141.4%.

The exchange-traded fund (ETF) tracks the Nasdaq Global High Equity Income index, which has notably higher weightings to financials (47%) and energy (15%), with just 1.3% in technology stocks.

Companies are selected based on factors such as liquidity and dividend yield, and must exhibit the ability to increase dividends over time.

It also uses a ‘plough-back’ approach, weighting companies based on their net income minus dividends paid. Stocks are capped at 3% for developed market companies and 1% for emerging market businesses.

First Trust Global Equity Income UCITS ETF was included as one of the funds with the lowest correlation to the S&P 500 in a Trustnet study last year and protected investors during the ‘Trump slump’ in 2022 and 2025.

Another long-term laggard turning things around in 2025 was the $9.4bn Janus Henderson Global Equity Income fund. While its 10-year figures underwhelm (it has made a fourth quartile 134.8% return over a decade), it delivered 17.4% last year.

Managed by Andrew Jones, Ben Lofthouse and Faizan Baig, the strategy targets an income in excess of 80% of the MSCI ACWI High Dividend Yield index over rolling three‑year periods while also achieving capital growth over the long term.

The managers prioritise strong dividends, low valuations and cashflow durability, with portfolio positioning including overweights to the index in financials (19.7% vs 17.5%), information technology (17.5% vs 9%) and industrials (14.1% vs 12.3%). The fund is most notably underweight consumer staples at 11% compared to the index weighting of 14.7% and healthcare (8.4% vs 14%).

Holdings such as Microsoft, Samsung and TSMC reflect an emphasis on financially robust companies with reliable cashflow profiles, rather than purely high‑yield names.

It is recommended by fund selectors at Barclays Smart Investor, who included it on the firm’s best-buy list.

“Janus Henderson has a very strong and established team managing global income since 2006. The fund managers, Andrew Jones and Ben Lofthouse, are supported by one of the largest teams of analysts in the global equity income sector and they can utilise the research and insight from the other fund managers and analysts across the firm,” they said.

Third on the list is Courtiers Global (ex UK) Equity Income, which is managed by Gary Reynolds. The £49.5m fund returned 17.1% over one year.

It applies a fundamental, value‑tilted, equally-weighted approach, which has tended to increase exposure to smaller‑cap and value names versus large-cap‑weighted peers.

Several holdings made notable positive contributions last year, with the managers highlighting Citigroup, Banca Monte dei Paschi di Siena and Deluxe Corp, which added 0.4, 0.4 and 0.3 percentage points to portfolio performance respectively. In contrast, HP, Civitas Resources and Wereldhave NV detracted 0.3, 0.2 and 0.1 percentage points.

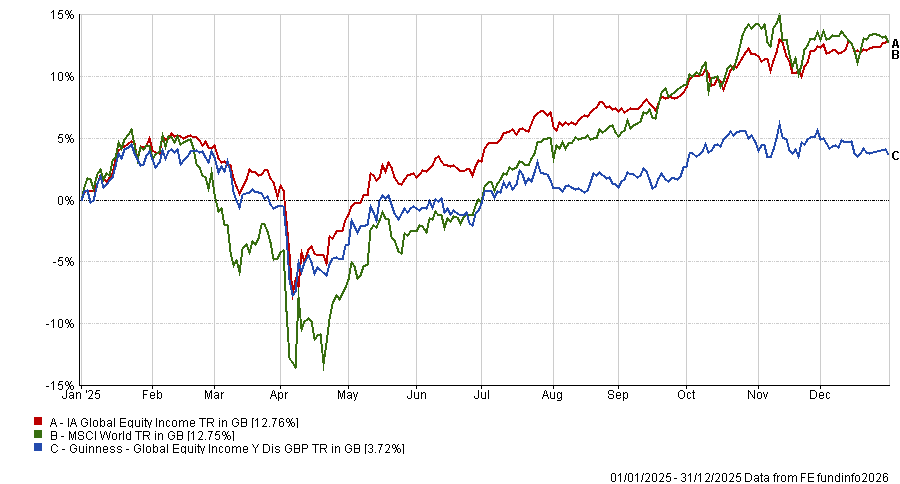

Performance of the funds vs sector in 2025

Source: FE Analytics

But while several long‑term laggards moved up the rankings, one of the sector’s more consistent names fell behind in the shifting market environment.

The $7.3bn Guinness Global Equity Income gained just 3.7% in 2025, lagging the sector – in strong contrast to its top-quartile 200.1% total return over 10 years.

Managed by Ian Mortimer and Matthew Page, it follows a high‑conviction, quality process that aims to deliver an above‑market yield while maintaining a preference for dividend growth rather than outright high yield.

To do this the managers apply a screening process to a global universe of around 14,000 companies, selecting only those that have delivered a cashflow return on investment (CFROI) of at least 10% annually for each of the past 10 years and maintain a debt‑to‑equity ratio below one.

This typically steers the portfolio towards more mature companies and away from highly cyclical areas. The fund is equally weighted and high conviction with 35 holdings.

In the fund’s mid-2025 investment commentary, the managers attributed underperformance to the fund’s underweight to the information technology and communication services sectors – more specifically, the fund’s underweight to the Magnificent Seven stock.

Given the dominance of mega‑cap tech stocks in 2025’s equity rally, this underweight created a meaningful drag on relative performance

In addition, they said the fund’s overweight allocations to consumer staples and healthcare acted as a headwind as both sectors underperformed.

Performance of the fund vs sector and benchmark in 2025

Source: FE Analytics